Global| Oct 29 2009

Global| Oct 29 2009Q3 GDP Posts First Gain After More-Than Year Long Recession

by:Tom Moeller

|in:Economy in Brief

Summary

The U.S. economy grew last quarter at hardly a barn-burning rate, but at least it was positive for the first time in over a year. Real GDP during 3Q'09 grew at an expected 3.5% annual rate after a 3.7% decline since late-2007. The [...]

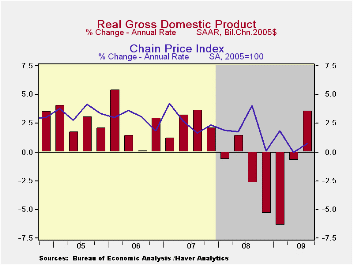

The U.S. economy grew last quarter at hardly a barn-burning rate, but at least it was positive for the first time in over a year. Real GDP during 3Q'09 grew at an expected 3.5% annual rate after a 3.7% decline since late-2007. The rise was fueled by upturns in domestic demand and inventories but lessened by deterioration in the foreign trade deficit. Consensus expectations are that economic growth will continue in coming quarters at roughly a 3.0% rate which, by postwar standards, would be subpar.

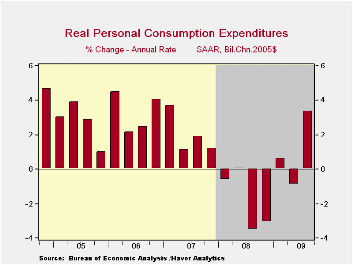

Domestic final demand growth was positive for just the second

quarter since 1Q'08. The upturn owed to a 3.1% gain in consumer

spending (-0.3% y/y) that was led by a 22.8% rise in durables

consumption. The Cash for Clunkers sales incentive program by

auto-makers caused motor vehicle consumption to jump at a 56.4% annual

rate, though it still was up just 1.4% from one-year earlier.

Elsewhere, personal consumption of furniture grew at a 6.4% (-5.9% y/y)

rate following a like downturn during 2Q. Spending on clothing

& shoes fell at a 1.5% (-5.1% y/y) rate while services spending

gained a modest 1.8% (0.4% y/y).

Domestic final demand growth was positive for just the second

quarter since 1Q'08. The upturn owed to a 3.1% gain in consumer

spending (-0.3% y/y) that was led by a 22.8% rise in durables

consumption. The Cash for Clunkers sales incentive program by

auto-makers caused motor vehicle consumption to jump at a 56.4% annual

rate, though it still was up just 1.4% from one-year earlier.

Elsewhere, personal consumption of furniture grew at a 6.4% (-5.9% y/y)

rate following a like downturn during 2Q. Spending on clothing

& shoes fell at a 1.5% (-5.1% y/y) rate while services spending

gained a modest 1.8% (0.4% y/y).

In the fixed-investment side of the GDP accounts, residential

spending also grew for the first time since 1Q'06. The 23.3% rise

(-18.1% y/y) followed a 2Q decline of similar magnitude. During the

downturn, which spanned three years, residential investment fell by

more than one-half. Continuing to the downside at a 2.5% (-18.9% y/y)

rate was business investment. The decline was led by a 9.0% (-20.8%

y/y) drop in spending on structures though equipment spending rose a

modest 1.1% (-17.9% y/y). That increase was led by a gain in

transportation equipment spending (-47.2% y/y) and an upturn in

information processing equipment & software (-6.4% y/y).

Government investment rose at a 2.3% rate (1.8% y/y) led by a gain in

defense spending (5.0% y/y).

In the fixed-investment side of the GDP accounts, residential

spending also grew for the first time since 1Q'06. The 23.3% rise

(-18.1% y/y) followed a 2Q decline of similar magnitude. During the

downturn, which spanned three years, residential investment fell by

more than one-half. Continuing to the downside at a 2.5% (-18.9% y/y)

rate was business investment. The decline was led by a 9.0% (-20.8%

y/y) drop in spending on structures though equipment spending rose a

modest 1.1% (-17.9% y/y). That increase was led by a gain in

transportation equipment spending (-47.2% y/y) and an upturn in

information processing equipment & software (-6.4% y/y).

Government investment rose at a 2.3% rate (1.8% y/y) led by a gain in

defense spending (5.0% y/y).

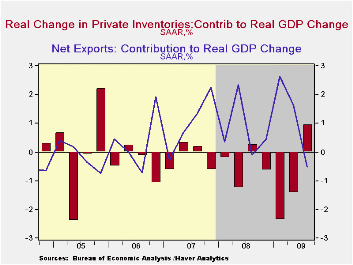

Inventory accumulation made a positive contribution to GDP

growth for just the second time in two years. The modest 0.9% addition

followed subtractions of 1.4 and 2.4 percentage points during the prior

two quarters.

Inventory accumulation made a positive contribution to GDP

growth for just the second time in two years. The modest 0.9% addition

followed subtractions of 1.4 and 2.4 percentage points during the prior

two quarters.

For the first time in a year, deterioration in the foreign trade deficit lowered GDP growth. The 0.5 percentage point subtraction was due to a 16.3% (-14.9% y/y) rise in real imports which outpaced the 14.7% (-11.2% y/y) gain in exports.

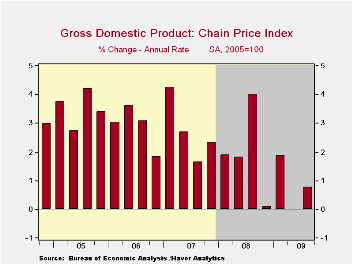

The GDP price deflator rose a slim 0.8%. Though the PCE price index gained 2.8% (-0.6% y/y), the rise in the overall domestic final sales price index was held to just 1.6% (-1.0% y/y) as the fixed investment price index fell sharply (-2.5% y/y).

| Chained 2005$, % AR | 3Q '09 | 2Q '09 | 1Q '09 | 2Q Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| GDP | 3.5 | -0.7 | -6.4 | -2.3 | 0.4 | 2.1 | 2.7 |

| Inventory Effect | 0.9 | -1.4 | -2.4 | -1.2 | -0.4 | -0.4 | 0.1 |

| Final Sales | 2.6 | 0.7 | -4.1 | -1.5 | 0.8 | 2.5 | 2.6 |

| Foreign Trade Effect | -0.5 | 1.7 | 2.6 | 0.9 | -1.2 | 0.8 | 0.1 |

| Domestic Final Demand | 3.0 | -0.9 | -6.4 | -2.4 | -0.4 | 1.7 | 2.5 |

| Chained GDP Price Index | 0.8 | -0.0 | 1.9 | 0.7 | 2.1 | 2.9 | 3.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief