Global| Nov 24 2009

Global| Nov 24 2009Q3 GDP Growth Revised Down Due To Domestic Demand & Foreign Trade

by:Tom Moeller

|in:Economy in Brief

Summary

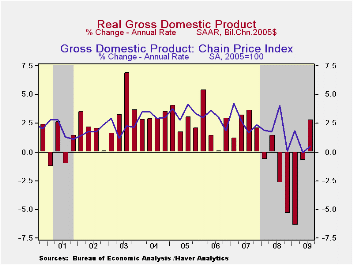

The second estimate of 3Q U.S. economic growth was lowered from the advance report due to slower growth in domestic demand and greater deterioration in the foreign trade deficit. The revision to 2.4% from 3.5% was greater than [...]

The second

estimate of 3Q U.S. economic growth was lowered from the advance report

due to slower growth in domestic demand and greater deterioration in

the foreign trade deficit. The revision to 2.4% from 3.5% was greater

than expectations for a lessening to 2.9%. Nevertheless, growth last

quarter was the first positive figure since 4Q 2007.

The second

estimate of 3Q U.S. economic growth was lowered from the advance report

due to slower growth in domestic demand and greater deterioration in

the foreign trade deficit. The revision to 2.4% from 3.5% was greater

than expectations for a lessening to 2.9%. Nevertheless, growth last

quarter was the first positive figure since 4Q 2007.

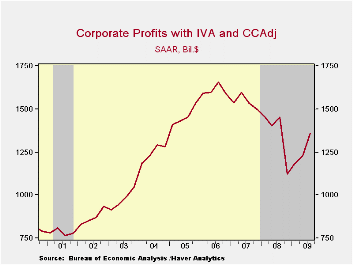

Accompanying

the GDP figure was the first estimate of 3Q corporate profits. The

10.6% rise versus 2Q was the third consecutive quarterly increase and

diminished the y/y decline to 6.7% from -25.1% at its worst in 4Q' 08.

Lower market interest rates lifted earnings in the financial sector by

more than one-third (25.4% y/y) and they tripled from year-end '08.

Earnings from the rest of the world increased 6.7% (-19.1% y/y) while

the end of the recession raised domestic nonfinancial profits by 2.0%

(-12.5% y/y) for the second quarterly increase.

Accompanying

the GDP figure was the first estimate of 3Q corporate profits. The

10.6% rise versus 2Q was the third consecutive quarterly increase and

diminished the y/y decline to 6.7% from -25.1% at its worst in 4Q' 08.

Lower market interest rates lifted earnings in the financial sector by

more than one-third (25.4% y/y) and they tripled from year-end '08.

Earnings from the rest of the world increased 6.7% (-19.1% y/y) while

the end of the recession raised domestic nonfinancial profits by 2.0%

(-12.5% y/y) for the second quarterly increase.

Deterioration in the foreign trade deficit subtracted a greater 0.8 percentage points from 3Q GDP growth after an initially estimated 0.5% subtraction. Import growth was increased to 20.8% (-14.1% y/y) yet the gain in exports also was revised up to 17.0% (-10.8% y/y).

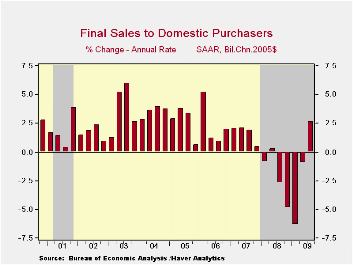

Domestic final demand growth also was revised down to 2.7% from 3.0%. Real PCE growth was revised down to 2.9% (-0.1% y/y) from 3.1% as the Cash for Clunkers sales program gave slightly less lift to vehicle sales as estimated earlier. Elsewhere, personal consumption of furniture grew at an unrevised 6.3% (-5.9% y/y) rate but the decline in spending on clothing & shoes was halved to 0.7% (-5.0% y/y). Services spending gained a slightly reduced 1.0% (0.4% y/y).

On the fixed-investment side of the GDP accounts, the quarterly rise in residential spending was slightly reduced to 19.5% (-18.8% y/y). Business investment also fell at a slightly increased 4.1% (-19.3% y/y) rate. Government investment rose at an increased 3.1% rate (2.0% y/y) led by an 8.9% gain in defense spending (5.2% y/y).

The addition to 3Q

growth in GDP from inventories was unchanged at 0.9 percentage points.

The addition followed subtractions of 1.4 and 2.4 percentage points

during the prior two quarters, and was just the second positive

contribution to GDP growth in two years.

The addition to 3Q

growth in GDP from inventories was unchanged at 0.9 percentage points.

The addition followed subtractions of 1.4 and 2.4 percentage points

during the prior two quarters, and was just the second positive

contribution to GDP growth in two years.

The gain in the GDP price deflator was lowered slightly to 0.5%. The PCE price index was ticked lower to 2.7% (-0.7% y/y) and the rise in the overall domestic final sales price index was brought down to 1.5% (-1.0% y/y).· The U.S. National Income & Product Account data are available in Haver's USECON and the USNA databases.

Can the Term Spread Predict Output Growth and Recessions? A Survey of the Literature from the Federal Reserve Bank of St. Louis is available here.

| Chained 2005$, % AR | 3Q '09 Preliminary | 3Q '09 Advance | 2Q '09 | 1Q '09 | 2Q Y/Y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|---|

| GDP | 2.4 | 3.5 | -0.7 | -6.4 | -2.5 | 0.4 | 2.1 | 2.7 |

| Inventory Effect | 0.9 | 0.9 | -1.4 | -2.4 | -1.2 | -0.4 | -0.4 | 0.1 |

| Final Sales | 1.9 | 2.6 | 0.7 | -4.1 | -1.6 | 0.8 | 2.5 | 2.6 |

| Foreign Trade Effect | -0.8 | -0.5 | 1.7 | 2.6 | 0.8 | -1.2 | 0.8 | 0.1 |

| Domestic Final Demand | 2.7 | 3.0 | -0.9 | -6.4 | -2.4 | -0.4 | 1.7 | 2.5 |

| Chained GDP Price Index | 0.5 | 0.8 | -0.0 | 1.9 | 0.6 | 2.1 | 2.9 | 3.3 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief