Global| May 15 2014

Global| May 15 2014Q1 GDP Release Ends Land of Make-Believe

Summary

The euro area put in a disappointing performance in the first quarter of 2014 as GDP is only rising at a 0.8% annual rate. Among the early reporters, GDP declined in Portugal, dropped sharply in the Netherlands, fell in Italy and fell [...]

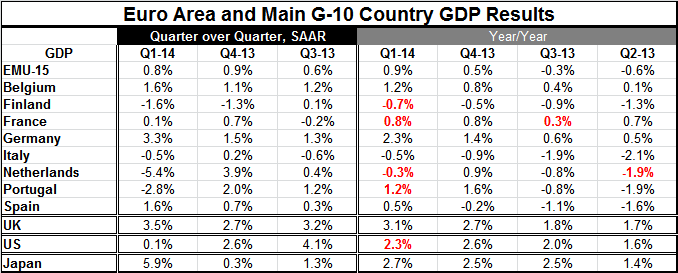

The euro area put in a disappointing performance in the first quarter of 2014 as GDP is only rising at a 0.8% annual rate. Among the early reporters, GDP declined in Portugal, dropped sharply in the Netherlands, fell in Italy and fell in Finland. France posted only the narrowest increase of 0.1%; that's essentially stagnation. Of the eight early reporters, four showed GDP declines. Germany put in a stronger quarter than expected; its gain was 3.3% at an annual rate. After that, Belgium and Spain each posted increases of 1.6% and then there's France with a gain of 0.1%.

The euro area put in a disappointing performance in the first quarter of 2014 as GDP is only rising at a 0.8% annual rate. Among the early reporters, GDP declined in Portugal, dropped sharply in the Netherlands, fell in Italy and fell in Finland. France posted only the narrowest increase of 0.1%; that's essentially stagnation. Of the eight early reporters, four showed GDP declines. Germany put in a stronger quarter than expected; its gain was 3.3% at an annual rate. After that, Belgium and Spain each posted increases of 1.6% and then there's France with a gain of 0.1%.

The year-over-year figures show that the European Monetary Union is growing less than 1% at an annual rate. Still, this represents acceleration from its fourth quarter gain of 0.5% at an annual rate.

Four of the eight early reporting countries show GDP decelerations based on their year-over-year growth in the first quarter compared the fourth quarter. Portugal has slowed from a 1.6% gain to a 1.2% gain in the first quarter. The Netherlands slowed from a 0.9% gain to post a decline of 0.3% year-over-year. Finland's -0.5% drop in the fourth quarter is now worse in the first quarter at -0.7%. France is technically weaker while posting the same (rounded) 0.8% year-over-year pace. In addition to those disappointments, Italy, while improving its rate of growth in the first quarter, is still declining year-over-year at a 0.5% annual rate.

Germany continues to be the strong man of this group; as the largest country in the euro area, it is an important part of the 0.9% increase for the EMU year-over-year. But it's also clear that this strength in Germany is not helping the rest of the monetary union very much. However, this quarter German growth changed its stripes to an important extent as growth was fueled by domestic demand rather than by external demand. That is significant and it could turn Germany into a positive force for growth for the euro area in the quarters ahead. But so far, that effect has been missing.

Two of the largest EMU countries show GDP increases year-over-year, Germany and Spain. While the other two, France and Italy, are still showing declines. On the whole, we score the euro area as floundering. At least that sense of consistency should make it easier for the European Central Bank to make policy. We would expect the Bundesbank to continue to be an outlier and to resist efforts at further accommodation. But EMU-wide weak GDP growth seems to support the notion of a more aggressive ECB.

Outside of the monetary union, the UK put in the strong quarter growing at 3.5% at an annual rate. The UK GDP growth continues to accelerate growing at a 3.1% annual rate year-over-year.

The US has already put in a paltry growth rate. Year-over-year US growth decelerates this quarter, falling to a 2.3% pace, down from 2.6% in the fourth quarter.

Japan posted a colossal growth rate of nearly 6% at an annual rate in the first quarter. This drives Japan's year-over-year growth rate to 2.7%, up from the pace 2.5% recorded in the fourth quarter.

Here, it's important to note the GDP growth rates are not always what they seem. Taken at face value, the US has an extremely weak quarter, putting in on a par with France. But below the surface, in the details of the incoming monthly data, we know that the US economy is already rebounding very strongly in the second quarter and that the fourth quarter result was largely a result of some extreme weather in the US. Meanwhile, France's problems remain. Conversely, the Japanese growth number greatly exaggerates Japan's economic strength and prospects. Japan's bulging GDP largely reflects the imposition of a consumer tax at the end of the quarter. This caused spending to cram into the first quarter in order to avoid in the second quarter the taxation of consumer spending. Thus, first quarter growth in Japan has borrowed heavily from the rest of the year; we expect second-quarter growth to be much weaker on account of the shifting forward of consumer spending. Already Japan's consumer confidence has been falling in reaction to this tax. Japan's GDP signal this quarter should be reversed.

GDP growth rates have to be viewed in the context of the events that underlie them to be understood. We're not terribly surprised by the disappointing results from Europe today, because there has been so much unevenness in the economic statistics that we have been seeing through the course of the quarter. Even German statistics have been tilted to the weak side in recent months. The bulge in Japan's data was also tipped off by monthly patterns in its data.

When making policy, the ECB will be looking at the real events and not simply at GDP growth rates. However, in Europe, the rates mostly speak the truth of the times. While there may not be much left for the ECB to do, we expect these GDP results to pave the way for more aggressive monetary policy. Policies of austerity continue to rock and in some cases dominate GDP growth rates in the euro area. Portugal, a country emerging from its bailout, was expected to show growth this quarter. Its failure to do that is a blow to that country. France was expected to have done better, but taxes imposed to hit fiscal targets sent France's growth off the tracks.

Not only does the euro area have challenges, but so do a number of its member countries. Not everything that is wrong in the euro area and in its member country economies can be fixed by monetary policy. While the path of monetary policy may seem clear, in the wake of these reports it remains unclear how effective monetary policy will be in turning things around.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief