Global| May 11 2007

Global| May 11 2007PPI: Sheep in wolf’s clothing

Summary

Wolf of a headline but lamb inside... Of course the PPI headline is scary. But we know that it is energy with an assist from food. But if you look at the core you will see that not only this month but in general it has been pretty [...]

Wolf of a headline but lamb inside...

Of course the PPI headline is scary. But we know that it is energy with an assist from food. But if you look at the core you will see that not only this month but in general it has been pretty stable. We still think that inflation problems lurk but we do not think energy is the source of worry.

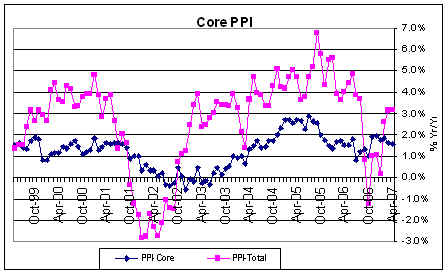

When headline inflation swung it did tend to transmit some of those changes to the core, as the graph above shows. But the transmission effects were very muted. Headline inflation bottomed at -2.8% in January 2002 while core inflation bottomed at -0.6% in December of that same year. Headline inflation swept higher to peak at 6.8% in Sept 2005 while core inflation peaked at 2.9% and did so in July ahead of the headline. With headline inflation swinging in a range of 9.6 percentage points core inflation swung in a range of 3.5 percentage points. And those statistics refer to the most extreme monthly observations. We are still seeing some ‘wild’ swings in headline inflation but they are not as long-lasting as in 2001. Thus the impact will be blunted. Core inflation is in fact falling over the past six months when the headline has been rising. We are more worried about the transmission to core inflation from labor costs since headline inflation looks much more like it is unstable month to month than it looks to be trending higher.

Moreover, this next push up in energy prices will be small compared to the previous one.

The table shows that inflation trends of all sorts are still fairly well contained. However since goods inflation has been lower than service sector inflation we need for goods inflation to be well be the 2% mark for it to be compatible with the Fed’s 2% (or 2.4% in CPI terms) ‘core’ maximum in terms of its unofficial comfort zone – I know it sounds like something from a foot doctor.

It is striking how inflation has built over the past three months in energy and foods but how when you remove the food and energy from PPI measures inflation rates calm down immediately. Finished consumer goods inflation, the part of this report that feeds into the CPI fell by 0.1% this month. For the CPI however we have to add in the markups to take producer goods to retail, then add services and add in imports to get to the CPI itself. There is no assurance on this but since service sector wages have been decompressing and import prices for consumer goods and vehicles have been moderate, looking for a moderate CPI core is a reasonable thing to do even in the face of surging energy and rising food prices.

| Apr-07 | PPI Trends By Type Of Good | ||||

| PPI | 1Mo:M/M | 3-Mo:ar | 6-Mo:ar | 1-Yr | Yr-Ago |

| Total PPI | 0.7% | 12.8% | 10.0% | 3.2% | 4.0% |

| Finished Consumer Goods | 0.9% | 16.6% | 12.2% | 3.5% | 4.9% |

| Consumer Foods | 0.4% | 15.4% | 12.7% | 7.8% | -0.9% |

| Finished Consumer Goods Excl Foods | 1.1% | 16.8% | 11.9% | 2.1% | 7.1% |

| Nondurables less Food | 1.7% | 25.2% | 15.7% | 2.8% | 9.9% |

| Consumer Nondurable excl Food and Energy | -0.1% | 3.8% | 3.1% | 2.2% | 2.7% |

| Durable Goods | -0.2% | -1.2% | 3.1% | 0.4% | 0.1% |

| Finished Core Consumer Goods | -0.1% | 1.7% | 3.2% | 1.4% | 1.6% |

| Capital Goods | 0.1% | 1.4% | 3.2% | 1.8% | 1.5% |

| Manufacturing Industries | 0.2% | 2.1% | 3.0% | 2.8% | 1.8% |

| Nonmanufacturing Industries | 0.1% | 0.8% | 3.3% | 1.5% | 1.3% |

| Core PPI | 0.0% | 1.5% | 3.2% | 1.6% | 1.5% |

| Memo: Finished Energy | 3.4% | 50.6% | 30.2% | 3.5% | 17.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief