Global| Oct 02 2009

Global| Oct 02 2009PPI Points Way Higher for Euro Area Inflation

Summary

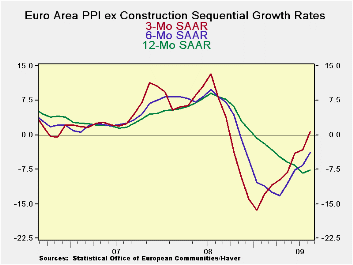

August’s EMU PPI excluding construction rose by 0.7% following a drop of 0.9% in July. Still the three-month growth rate (annualized) is now positive at 0.7% the six month growth rate is at -3.9% and the 12-month growth rate is at [...]

August’s EMU PPI excluding construction rose by 0.7% following

a drop of 0.9% in July. Still the three-month growth rate (annualized)

is now positive at 0.7% the six month growth rate is at -3.9% and the

12-month growth rate is at -7.6%. Inflation is gaining a toe hold again

in EMU at the producer price level. The ECB ahs a ceiling arrangement

for the HICP only (harmonized index of consumer inflation).

Even so, inflation does not appear to be cooking in any sense

of the word. For consumer goods, prices were still flat in August and,

at -0.3%, the three month growth rate for consumer goods is still close

to its six month annualized pace at -0.6%. There is no pressure there.

Capital goods prices continued to fall in August dropping by 0.1%. Over

three months, capital goods prices are falling by 0.8%; that is a

slight but only a slight improvement from dropping by 1.4% at an annual

rate over six months. There is not much inflation pressure from capital

goods prices either.

Virtually all the inflation pressure in the PPI is coming from

industrial supplies or intermediate goods. Intermediate goods prices

rose by 0.4% in August. They are also up at a 1.1% annual rate over

three months and down at an annual rate of 3.6% over six months.

Across EMU countries the headline PPI rose in all of the

largest of them. Ex food and energy prices rose in Germany and in

France as well. For all these price measures, the August rise is

balanced by a drop in July.

Still the bottom line is that prices are on the move again.

While it does not look like the pressures are very widespread across

commodity classifications or very intense, the pressure seems quite

real and widespread cross the larger EMU nations.

| Euro Area and UK PPI Trends | ||||||

|---|---|---|---|---|---|---|

| M/M | Saar | |||||

| Euro Area | Aug-09 | Jul-09 | 3-Mo | 6-MO | Yr/Yr | Y/Y Yr Ago |

| Total excl Constructions | 0.7% | -0.9% | 0.7% | -3.9% | -7.6% | 8.3% |

| Capital Goods | -0.1% | -0.1% | -0.8% | -1.4% | -0.2% | 2.4% |

| Consumer Goods | 0.0% | 0.0% | -0.3% | -0.6% | -2.6% | 4.2% |

| Intermediate & Cap Goods | 0.4% | -0.1% | 1.1% | -3.6% | -7.4% | 5.4% |

| MFG | 1.0% | -0.5% | 4.1% | -0.7% | -7.1% | 6.8% |

| Germany | 0.5% | -1.6% | -6.8% | -9.4% | -7.6% | 8.1% |

| Germany excl Energy | 0.3% | -0.2% | 0.0% | -1.9% | -3.3% | 3.2% |

| France | 0.7% | -0.4% | 4.0% | -2.9% | -8.4% | 7.7% |

| France excl Food & Energy | 0.1% | -0.3% | -1.1% | -2.6% | -3.6% | 3.4% |

| Italy | 0.9% | -0.9% | 1.1% | -2.8% | -7.8% | 8.1% |

| UK | 2.5% | -1.7% | 6.2% | 1.0% | -6.5% | 21.9% |

| Euro Area Harmonized PPI ex construction | ||||||

| The EA 13 countries are Austria, Belgium, Finland, France, Germany, Greece, Ireland, Italy, Luxembourg, the Netherlands, Portugal, Slovenia | ||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief