Global| Sep 03 2019

Global| Sep 03 2019PPI Is Crushed by Weak Oil But Price Trends Aside from Oil Seem to Moderate, Too

Summary

Sequential price trends from 12-months to 6-months to 3-months show the PPI’s annual rate of expansion is steadily slowing and doing so for all three major price categories as well. The exception is for consumer goods where a six- [...]

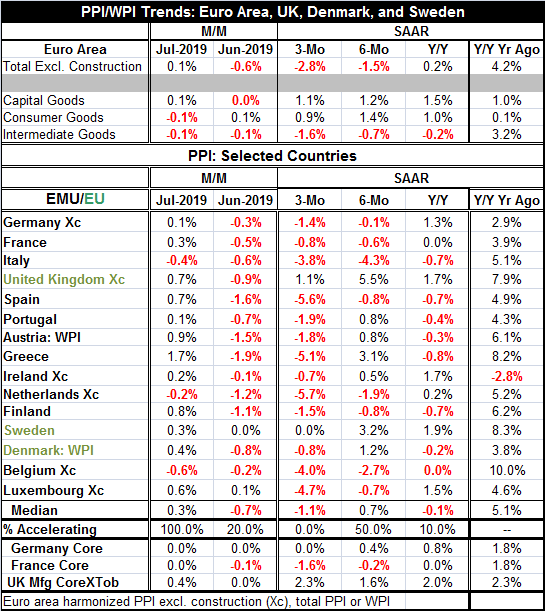

Sequential price trends from 12-months to 6-months to 3-months show the PPI’s annual rate of expansion is steadily slowing and doing so for all three major price categories as well. The exception is for consumer goods where a six-month speed up bucks the trend slowing even though the three-month result shows that weakness comes back on track. The headline trend show a meager 0.2% rise in the PPI over 12 months with declines over six months and three months. Neither capital goods nor consumer goods PPI prices show declines on any horizon. The trend to declining prices comes wholly from ‘intermediate’ prices where oil plays an outsized role.

Sequential price trends from 12-months to 6-months to 3-months show the PPI’s annual rate of expansion is steadily slowing and doing so for all three major price categories as well. The exception is for consumer goods where a six-month speed up bucks the trend slowing even though the three-month result shows that weakness comes back on track. The headline trend show a meager 0.2% rise in the PPI over 12 months with declines over six months and three months. Neither capital goods nor consumer goods PPI prices show declines on any horizon. The trend to declining prices comes wholly from ‘intermediate’ prices where oil plays an outsized role.

The small table below shows the simple correlations with Brent oil for 12-month percentage changes. The simple correlation shows the largest impact on manufactured goods prices at 0.79 with intermediate goods at 0.57 and consumer goods close behind at 0.55. Capital goods prices are very weakly correlated with Brent with a correlation coefficient of 0.11. Currently Brent prices are higher by 14.4% over 12 months. That pace of decline is slightly less than June’s 17.2% decline over 12 months. Oil prices had decelerated for three months in a row until July; but July still shows a substantial decline in Brent year-over-year that is being passed on to headline PPI prices and a small month-to-month Brent price rise.

The PPI actually accelerated in all the countries listed in the table and Brent prices rose modestly on the month. That ‘acceleration’ largely results from a switch from prices that declined in June to prices that rose (9 of 13 cases) in July. In fact, July did see some substantial monthly price increase from 1.7% in Greece, Austria +0.9%, Finland +0.8%, the United Kingdom and Spain with each up by 0.7%, and a moderate 0.4% gain from Denmark. That’s six of thirteen with substantial price increases in July. Generally, EMU-wide prices have tended to move in the same fashion as oil prices 75% of the time over the last 5.5 years. This month was no exception despite the small oil price move.

Oil is a bit complicated as a factor since the level of Brent oil prices hit is highest mark at $80.55/barrel in 2018 which was the highest price for oil by the barrel since October 2014. Oil prices moderated though January 2019 then picked up peaking at $71.55/barrel in April and holding high at $70.10/barrel in May. As a result, oil prices at $62.84/barrel in June and at 64.17/barrel in July reflect a moderation in the recent downward oil price pressure. But clearly, pressures vary depending on the horizon over which you look at oil prices- that is the compilation of oil. Oil price variability was highest in the last five years around June 2017; it has since been settling down with variability in a very narrow range over the last year and one quarter. Maybe oil’s impact on inflation will begin to settle down as well and become more consistent. Still, there is enough of it to affect the PPI monthly as well as year-over-year.

While PPI prices among these thirteen countries in the table shows acceleration in all countries month-to-month in July, only 20% showed acceleration in June on that basis. Over the last three months, in fact, none of them show acceleration compared to their six-month pace. The six-month pace for inflation shows half of the group accelerating and half decelerating compared to their respective 12-month paces. The 12-month pace shows acceleration in only 10% of the table for members compared to their respective paces of one year ago. As a result, inflation being higher on the month is a tempest in a tea pot and definitely is against trend.

While oil prices are having a significant impact, core prices for Germany and France show steady decelerations in sequential core prices in both countries. The U.K., a non-EMU country with its own currency and heaping Brexit issues still in need of address, shows core PPI prices are accelerating there…and that the currency is weakening.

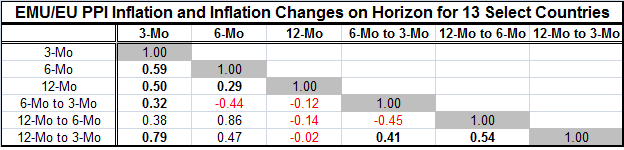

The correlation matrix below helps to describe some complicated features of this data set. Note that all of the inflation rate-to-rate correlations are positive. But all of the inflation changes are negatively correlated with the 12-month inflation pace. This seems to suggest that inflation is cycling more than trending. In countries with high inflation over 12 months, the tendency is for them to have a weaker change (or decline) in inflation over other subsequent shorter horizons and vice-versa. However, these correlations are low and can more solidly be described as suggesting that countries with high inflation over 12 months do not necessarily continue to show accelerating trends over shorter horizons. This also fits with the idea that inflation is cycling more than trending. So does the -0.45 correlation between the change in inflation for six-month to three-month vs. the change from 12-month to six-month. That suggests that inflation bulges tend to be followed by offsetting movements.

Although oil has had an impact on the evolution of inflation in the EMU, it is clear that, beyond oil, price moderation continues to be in force based on the moderated, contained and decelerating trends in France and Germany for core inflation. The U.K., of course, is a wholly different kettle of fish with a unique set of issues and with core inflation percolating.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief