Global| Mar 10 2021

Global| Mar 10 2021PPI in EMU Begins to Stir- Still Restrained

Summary

Oil prices are leading inflation higher in the EMU as well a globally. Oil and other commodities are gaining pace as growth looks to be more established, as virus-fighting seems to be more effective, as vaccination progresses on a [...]

Oil prices are leading inflation higher in the EMU as well a globally. Oil and other commodities are gaining pace as growth looks to be more established, as virus-fighting seems to be more effective, as vaccination progresses on a more widespread basis, and in the wake of a mammoth U.S. $1.9 trillion spending program. The U.S. Treasury bond market has for some time been battling the specter of rising inflation and now it is a more widespread phenomenon globally because of oil prices rising even as benchmark inflation rates remain subdued.

Oil prices are leading inflation higher in the EMU as well a globally. Oil and other commodities are gaining pace as growth looks to be more established, as virus-fighting seems to be more effective, as vaccination progresses on a more widespread basis, and in the wake of a mammoth U.S. $1.9 trillion spending program. The U.S. Treasury bond market has for some time been battling the specter of rising inflation and now it is a more widespread phenomenon globally because of oil prices rising even as benchmark inflation rates remain subdued.

The finalized January PPI

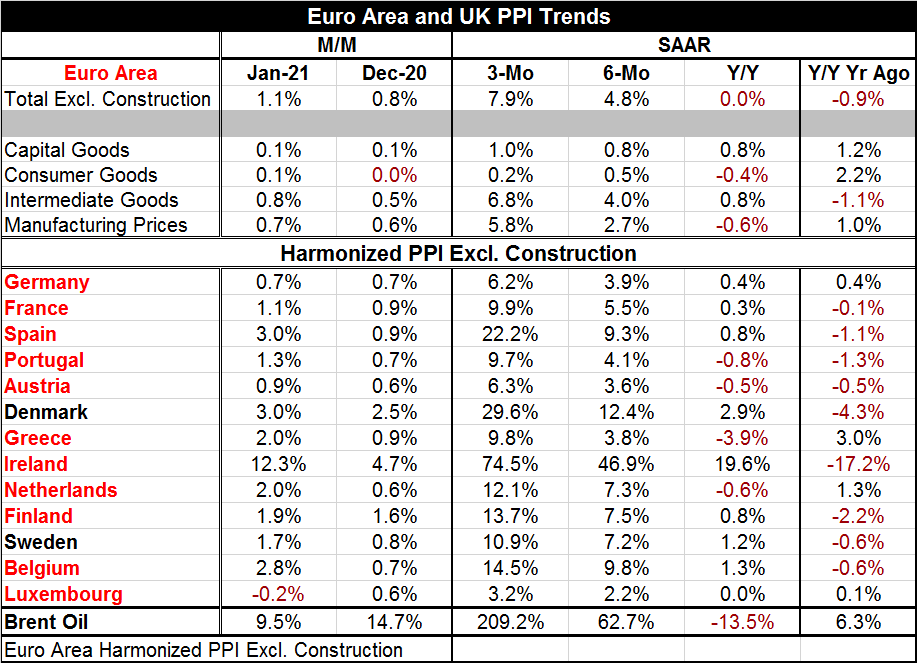

In the EMU, the PPI excluding construction rose by 1.1% in January. Manufacturing prices rose by 0.7%, led by a 0.8% gain in intermediate goods prices as consumer goods and capital goods each gained 0.1% on the month.

The PPI shows gathering pace with the year-on-year gain at flat, the six-month pace at 4.8% and the three-month pace at 7.9%. These annualized rates of increase for the PPI have been intensifying on shorter timelines.

Inflation is accelerating

Inflation is accelerating steadily and across the board with all countries in the table showing three-month inflation at a faster pace than six-month inflation and six-month inflation faster than 12-month inflation – there are 26 reinforcing observations there. Comparing inflation over 12-months to inflation of 12-months before shows inflation higher in nine of 13 countries (Germany, Greece, the Netherlands and Luxembourg are the exceptions). That is still a pretty broad sweep of acceleration.

Inflation still modest- but not in stealth mode

Despite all this inflation acceleration, year-on-year the price level is still falling in four countries and is unchanged in another. Contrarily, Ireland shows the PPI up by 19.6% over 12 months. In Denmark, it is up by 2.9%. Sweden and Belgium have prices up by 1.2 to 1.3%. The remaining four countries have year-on-year inflation at 0.8% or less.

Inflation still slips under the ECB's radar, but it is not in stealth mode and is making a lot of noise. Over three months, seven countries are posting a PPI gain in double digits. Three have gains in excess of a 20% annual rate. Clearly inflation is on the rise; the questions of ‘for how long will it rise?' and ‘where it will settle?' remain unanswered.

Inflation's boil stems from oil

Brent oil prices rose by 9.5% in January after a 14.7% gain in December. They are up at a 209.2% annualized rate over three months, at a 62.7% annualized rate over six months and yet are lower by 13.5% over 12 months.

Brent inflation is correlated strongly with all PPI components except for capital goods where the positive correlation is still present but is weak. The highest correlation is with intermediate goods prices. Intermediate goods prices are seeing faster inflation acceleration than either capital goods prices or consumer goods prices during this period when oil prices have accelerated. There can be little doubt about what is at work. Year-on-year, however, all categories of prices are still weak with gains of less than 1%. Over 12 months, consumer goods prices, in fact, are lower as are overall manufacturing prices.

Inflation vs. the Virus

The ECB has an inflation-only policy mandate. However, the European economics still face their greatest threat from the virus and they have not gotten their vaccination programs off the ground as rapidly as the U.S. as Trump's ‘Operation Warp Speed' put the U.S. vaccine program on a fast track. The U.K. is an exception to that having worked hard to control the virus spread with lockdowns and an aggressive vaccination program as the more communicable strain of the virus has circulated there. While the manufacturing sector has been able to prosper even in the face of virus, the service sector cannot and that is the greatest impediment to growth since the service sector also is the employment sector for these economies. Still, oil prices have recovered and they are boosting the price level even if only temporarily. Inflation is not a factor for policy just yet, but in a few months down the road that could change and could put the ECB in a tough spot. If there are calls to normalize rates on the first signs of on-target inflation and if that comes before the virus has backed off enough to permit normal activity to occur on a more widespread basis, that could put ECB policymakers on the hot seat.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief