Global| Oct 02 2014

Global| Oct 02 2014PPI Drop Accelerates in Euro Area

Summary

The PPI in the European Monetary Union fell again in August, dropping by 0.2% after falling by 0.4% in July. The year-over-year drop is now 1.4%, a bit sharper than the 1.3% drop reported last month. The table at the bottom has PPI [...]

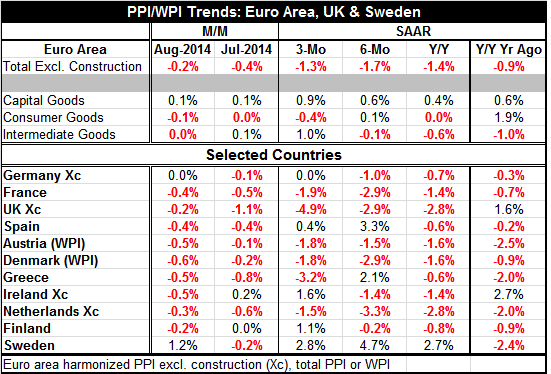

The PPI in the European Monetary Union fell again in August, dropping by 0.2% after falling by 0.4% in July. The year-over-year drop is now 1.4%, a bit sharper than the 1.3% drop reported last month.

The PPI in the European Monetary Union fell again in August, dropping by 0.2% after falling by 0.4% in July. The year-over-year drop is now 1.4%, a bit sharper than the 1.3% drop reported last month.

The table at the bottom has PPI data as reported by a mix of EU and EMU members with Sweden and the U.K. representing members of the European Union but not the Monetary Union. Among these countries, only Sweden had a PPI increase in August. All the rest saw price declines except Germany whose index was flat.

Over three months, six of the 11 countries in the table have prices falling, four have prices rising and Germany has prices flat.

Over six months, eight countries have prices falling and three have prices rising. Over 12 months, 10 of the 11 countries have prices falling with Sweden showing prices rising.

The downward pressure on prices is ubiquitous across time and countries.

The European Central Bank, however, is not focused on PPI inflation, but rather on inflation as measured by its HICP, the harmonized index of consumer prices. However, producer prices are not unimportant and their trends are quite clear.

The PPI sectors show the capital goods prices have continued positive over three months, six months and 12 months and actually have accelerated slightly. Consumer goods prices are flat year-over-year and falling over three months. Intermediate goods prices are falling year-over-year as well as six months but are up at a 1% annual rate over three months.

Growth continues its weakness in the euro area. Today, Christine Lagarde, IMF Managing Director, urged countries to boost growth. And she also urged labor reform, for countries to reduce tax evasion and to engage in infrastructure spending; only the latter measures is generally geared to boost in GDP growth. She has mentioned and warned of the growth in the shadow banking system. She is concerned about asset valuations and the persistent tendency for stock markets to rise. However, monetary policy around the world has monetary authorities with their feet flat down on the pedal and so these financial market effects are really only what you would expect in this environment. You can't endorse these policies and bemoan their effects.

Lagarde's urging for more growth fell short of the mention of more fiscal spending. Financial excess is one of the things that got us into the mess that we are in. As countries try to reduce their debt loads, they are also reducing leverage in their economies. There can be nothing else but downward pressure on growth rates while this process is in play. It may be that some temporary backtracking on this trend that allowed for fiscal policy stimulus could boost economies up to a stronger growth plane from which a reintroduction of fiscal responsibility would be more effective. But policymakers are not taking that course and Lagarde does not urge it. I compare her speech to someone rooting for a football team that s/he knows is very bad, but rooting for it nonetheless.

The IMF has cut its outlook and it recognizes the dire state of affairs in the global economy. It seems to be trying to manipulate people's expectations by urging more growth while at the same time being a member of the austerity club. And we know, you can't have it both ways. So enjoy the Lagarde speech but don't expect anything to come out of it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief