Global| Mar 02 2016

Global| Mar 02 2016PPI Deflation and Other Growing Risks in Europe

Summary

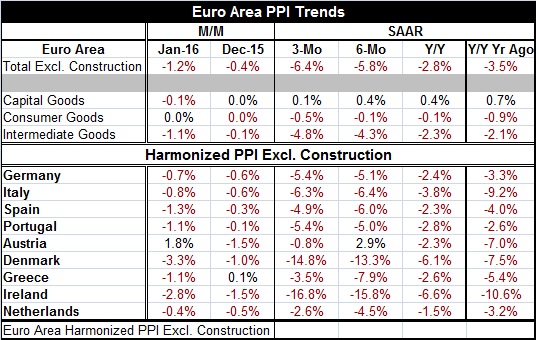

EMU PPI trends continue to feature price declines. The headline PPI series (PPI excluding construction) shows declines in January and December. In fact, the month-to-month declines go all the way back uninterrupted to March 2015. [...]

EMU PPI trends continue to feature price declines. The headline PPI series (PPI excluding construction) shows declines in January and December. In fact, the month-to-month declines go all the way back uninterrupted to March 2015.

EMU PPI trends continue to feature price declines. The headline PPI series (PPI excluding construction) shows declines in January and December. In fact, the month-to-month declines go all the way back uninterrupted to March 2015.

Sector price weakness is broad

Sector indices are consistently weak with capital goods prices falling in January after being flat in December. Consumer goods prices are flat for two months in a row while intermediate goods prices are lower in both January and December. Over a broader set of periods, the PPI headline shows an accelerating pace of decline from 12-month to six-month to three-month. On that same set of horizons, capital goods prices are expanding but are slowing. Consumer goods prices are dropping with their drop accelerating. Intermediate goods prices also are showing declines with an accelerating pace of decline to boot. This is broad sector price weakness. The leading sector for weakness is intermediate goods with energy, of course, the main reason, but with lots of weakness in other commodity prices as well. Other sectors with more product fabrication show weakness in step.

Incredible price declines and deceleration breadth

By country, we find weakness across the board. For the nine countries in the table, there are 18 month-to-month calculations and 16 of them show month-to-month price declines. The horizon calculations including the year ago period contain 36 calculations with all but one showing a price decline (yes, 35 of 36 possible). All this is remarkably consistent and an example of broad-based deflation for the PPI. Of the nine countries in the table, five show that the speed of price declines is picking up over three-month compared to six-month. Eight of them show that the speed of price declines is picking up for six-month compared to 12-month. In addition, only Austria shows a three-month speed of decline is less than its 12-month pace. But year-over-year declines show that annual price declines one year ago were generally even faster than they have been over the past 12 months. Portugal is an exception to this.

The ECB stresses and targets the CPI in its harmonized format (HICP). But on that basis, the ECB is badly missing its pledge to keep inflation just below 2%. PPI prices, however, tend to the more volatile series and what we see here is that there is NO sign of progress on being to stimulate inflation with the ECB's policies to date.

Migrant crisis as time bomb?

When we look at European policy, we continue to wonder whether the migrant crisis is going to blow up economic cooperation. Two new developments came into play on that front today. The first was the EU announcing a program (one that is long overdue) for migrants bottled up in Greece. Our view has long been that it has been unfair of `Europe' to shut the entry points, bottle-up the migrants in Greece, and to treat the Greeks like they have a problem that they must fix. This is clearly a European problem. Greece can hardly stop migrants from arriving by water despite the Belgian minister's urging to `push them back into the sea.' The second development comes from a NATO representative who claims that the exodus of migrants from Syria is the result of Russia `weaponizing' them to destabilize Europe. U.S. General Philip Breedlove, the senior NATO commander in Europe, said that the Russians are "weaponizing" migration to destabilize and undermine the continent. He further suggested that criminals, extremists and fighters were hiding in the flow of migrants. This view is that the migrants are not simply a casualty of war, but that Russia is perpetrating chaos in Syria with intent to drive the civilian population out and to Europe.

Migrant crisis as one of several economic events

Viewed in this way we cannot help but see the plight of the migrants as an economic event as well as a political problem. Ukraine is still destabilized and there have been some flare-ups there recently. Increasingly, it is hard to separate the geopolitical events from their economic consequences. The weakness in oil prices fits in that category. Today's turning back by China of Philippine fishing boats from traditional fishing grounds because China claims the local islands is yet another example of a direct economic effect from a political action. Here it is in the South China Sea. And just as there has been little progress on the economic front so has there been very little or no progress on any of these geopolitical fronts. Economic weakness, deflation and geopolitical instability continue to dominate the international scene and have become intertwined.

Where is the balance of risk?

In the U.S., the Federal Reserve still cannot puzzle out the `balance of risks' so monetary policy may be moving in the wrong direction there. In Europe, action on the migrant issue has been slow in coming. Europe has been way too slow even to recognize how it was at risk from the conflict in the Middle East; its inaction there is now a very expensive mistake. That has put in motion something that will be very hard to stop. Moreover, ECB approach against deflation continues to put promises on the frontline ahead of new actions. Fiscal policy remains `verboten' to use one word to describe its situation. I'd hardly call this a full court press to get things back to normal. I am reminded of the Meatloaf song with the verse, `I'd do anything for love, but I won't do that.' Germany may be putting Europe at much bigger risk by redlining fiscal policy compared to the risk that is being introduced by the ongoing monetary excess there. We just do not know that much about such monetary accommodation and by the time we find out it may be too late. Economic policy in Europe may be making the same kind of mistake at home that European foreign policy made in Syria. Some risks are hard to anticipate and come at you suddenly and unexpectedly. That is why it is good to implement policies that are well understood and time-tested instead of experimental. Better the devil you know than the one that you don't know. Europe needs fiscal stimulus. The Germans are wrong.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief