Global| Mar 02 2021

Global| Mar 02 2021Post Covid-19 Turbulence Rocks and Weakens German Retail Sales

Summary

German and other European retail sales have been put through a sort of test of fire in the wake of the covid-19 virus arrival and its various episodes of spreading. As an example, even in the U.S. where now over 20% of the population [...]

German and other European retail sales have been put through a sort of test of fire in the wake of the covid-19 virus arrival and its various episodes of spreading. As an example, even in the U.S. where now over 20% of the population is vaccinated - more than have tested positive for infection- there are still warnings of the possibility of a fourth wave. Medical professionals are simply flummoxed by the virus and its ability to mutate and spread even after it has seemingly been minimized.

German and other European retail sales have been put through a sort of test of fire in the wake of the covid-19 virus arrival and its various episodes of spreading. As an example, even in the U.S. where now over 20% of the population is vaccinated - more than have tested positive for infection- there are still warnings of the possibility of a fourth wave. Medical professionals are simply flummoxed by the virus and its ability to mutate and spread even after it has seemingly been minimized.

Of course, the various lockdowns and restrictions impact economic data and we see that in plain sight in retail sales. Germany extended a lockdown that ran through the end of February. In Asia, Japan has had a lockdown in the greater Tokyo area that it has been unwinding gradually. This is truly a global phenomenon.

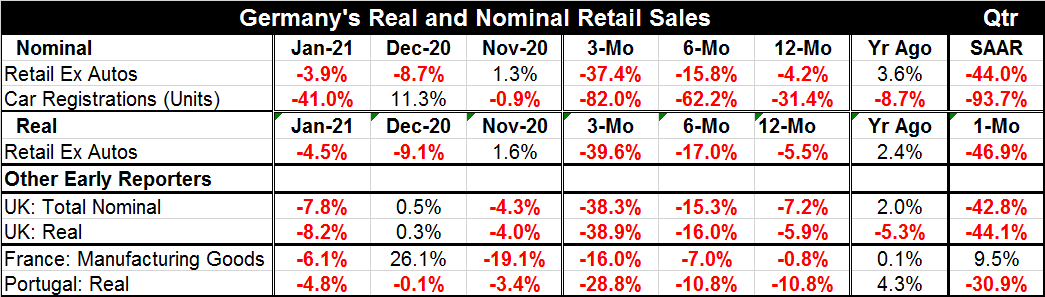

The German sales trends show sharp sales declines in December followed by another significant decline in January. Sales are sharply lower in both real and nominal terms. German retail sales again both real and nominal are getting progressively weaker in the more recent periods. This is a testament to the lockdown that has crimped activity.

However, PMI data released just yesterday underscore that the German manufacturing sector seems to be unaffected by the virus as its PMI gauge rose to 60.7 in February from 57.1 in January. The January report which is chronologically aligned with the retail sales report did slip, falling to 57.1 from 58.3 in December. In February, though, German unemployment has risen unexpectedly as the number unemployed rose by 9,000. The economic data continue to ebb and flow around the ‘virus cycle.’

Early in the new quarter German retail sales are plunging at a 44% annual rate in nominal terms and by 46.9% in real terms. Auto registrations have also tracked the weakness in overall retail sales and are falling at a 93.7% annual rate in the new quarter (that statistic is the January growth rate relative to the Q4 average of last year annualized). While Germany has often been lauded for its handling of the virus, it is now in the third iteration and is having a hard time controlling it. Its progress in terms of the death rate is still much better than in the U.S., but much of that is probably because of Germans being so much healthier than Americans where obesity and drug use have run wild.

There are also some early readings on retail sales in the U.K., France and Portugal. Each of these jurisdictions saw sales declines in January and each of them showed sales declines in at least two of the last three months. Moreover, each of them showed sales progressively weaker over more recent periods. Among these three countries, only France, where the statistic focuses on sales of manufactured goods, has an increase in sales in progress in the new quarter. Both the U.K. and Portugal see the same sorts of draconian sales declines in the quarter-to-date as we see in Germany.

On balance, Germany is still struggling with growth and that clearly links to the efforts to stave off spread of the virus. While retailing seems greatly affected, the German manufacturing machine drives on. The rest of Europe (based on a small sample here) appears to be affected much like Germany with retailing impaired and manufacturing more resilient. Europe’s progress on vaccinations is slower than in the U.S. But the vaccines are making progress and that is reason enough to expect to see these kinds of dour statics become isolated and to expect the return of growth. Still, the German retail sales graphic is a reminder that the virus can wreak havoc with economic data and can do so unpredictably.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief