Global| Jun 11 2015

Global| Jun 11 2015Portuguese Inflation Takes Hold

Summary

Inflation in Portugal is now rising sharply. Year-over-year inflation is still tepid, below 1% in both the HICP and National inflation definitions. But over three months, inflation is at a 4.5% annual rate on the HICP definition and [...]

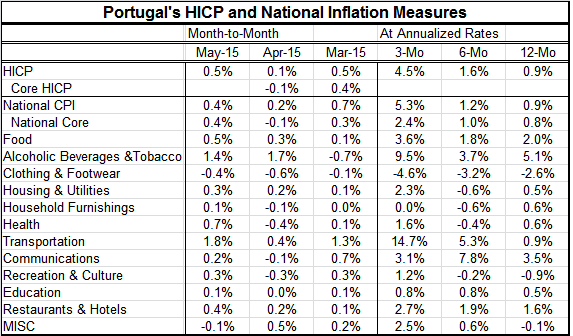

Inflation in Portugal is now rising sharply. Year-over-year inflation is still tepid, below 1% in both the HICP and National inflation definitions. But over three months, inflation is at a 4.5% annual rate on the HICP definition and 5.3% on the National definition. The National core inflation rate is also up by 0.9% year-over-year, but it is at a much more subdued 2.4% annual rate pace over three months. HICP core readings are not yet available.

Inflation in Portugal is now rising sharply. Year-over-year inflation is still tepid, below 1% in both the HICP and National inflation definitions. But over three months, inflation is at a 4.5% annual rate on the HICP definition and 5.3% on the National definition. The National core inflation rate is also up by 0.9% year-over-year, but it is at a much more subdued 2.4% annual rate pace over three months. HICP core readings are not yet available.

In May on the National inflation detail, prices fell in just two categories. In April they had fallen in six categories and in March they had fallen in two categories. Price weakness appears to be giving way to strength.

In May month-to-month inflation is up in 10 of 12 National categories. In April inflation had risen in only 5 of 12 categories. Over broader periods, inflation has accelerated; in three months compared to six months inflation is up in 9 of 12 categories as of May while over six months the acceleration is only in half the categories - six of 12. Over the past year, inflation is up compared to its annual rate of one year ago in 10 of 12 categories.

While the upturn in inflation is abrupt, it is also over rather brief period. As energy prices stop falling and turn to increases, they can have a pronounced impact on inflation. We see that in the differences in the trajectories between the headline and core rates of change.

Still Portugal is showing a good deal of inflation pressure and prices are rising on a broad front. While this is not the same sort of pressure that is being experienced, EMU-wide authorities will want to watch to see if inflation is taking hold faster in the peripheral countries than in the core countries as it always has in the past. Keeping EMU's progress on austerity is not just about reining in excess fiscal spending, but it is about keeping inflation at more or less the consistent pace in the various EMU members.

Right now Portugal is looking like it could be becoming an inflation problem. And this is with all eyes misdirected and focused on Greece. All hopes in the EMU are for some sort of facing saving deal for all that will not test the unity of the euro area. But while Greece is in the headlines, the EMU cannot afford to take its eye off the conditions prevailing in other member nations that also have been struggling. Running a currency union is always about multitasking.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.