Global| Jul 11 2018

Global| Jul 11 2018Portugal Shows Inflation Pressure

Summary

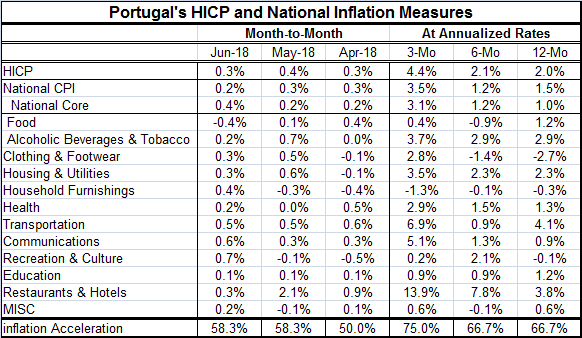

Portugal's inflation rate eased to a 0.3% gain in June after a 0.4% rise in May. That increase has the three-month inflation pace rising faster than the six-month pace and also represents a higher three-month pace at 4.4% than the [...]

Portugal's inflation rate eased to a 0.3% gain in June after a 0.4% rise in May. That increase has the three-month inflation pace rising faster than the six-month pace and also represents a higher three-month pace at 4.4% than the three-month pace of 1.7% that it logged last month.

Portugal's inflation rate eased to a 0.3% gain in June after a 0.4% rise in May. That increase has the three-month inflation pace rising faster than the six-month pace and also represents a higher three-month pace at 4.4% than the three-month pace of 1.7% that it logged last month.

Portugal's national CPI has similar characteristics this month. Its gain is smaller month-to-month and its three-month pace is higher than its six-month pace and its three-month pace accelerated compared to last month. And all those same characteristics carry over to the national core CPI as well.

Near-term Portugal has some inflation pressure. That conclusion is not particularly sensitive to the gauge used to measure it; that increases our confidence that the acceleration is a real event and not just a statistical anomaly. However, Portugal's pace of inflation over 12 months and even six months is still acceptable.

Portugal's HICP has reached the ECB speed-limit of 2%. Of course, there are no country by country objectives in any formal sense in the EMU. But based on the ECB's euro-area-wide objectives, Portugal's inflation is now at a sweet spot since the ECB objective is for inflation of a little less than 2%. Based on its domestic measures, inflation in Portugal is even lower at a pace of 1.5% overall and 1.0% excluding food and energy. With such low inflation in both the national gauge and its core, it's a possibility that the HICP has simply hit a bad month for seasonal adjustment and will be moving lower as well in the months ahead...or not.

The Portugal national consumer price index finds excessive inflation in only four of 12 categories in terms of their year-on-year pace. Over 12 months, prices rose 4.1% for transportation where fuel costs played a large role, restaurants and hotels show prices rising by 3.8%, alcohol and tobacco prices are up by 2.9%, and housing & utilities, another energy component, shows prices are up by 2.3%. On the whole, there are very few things to worry about in this report although inflation is also accelerating in each of these categories that show excessive (above 2%) inflation over 12 months.

More worrisome is that overall inflation is accelerating in most of the 12 categories regardless of its current or annual pace. In June and May, month-to-month inflation acceleration is present in 58% of the categories. In April, acceleration is balanced with acceleration/deceleration at 50%. But over 12 months and six months, inflation is rising compared to the previous period in the table in two thirds of the categories. Over three months, inflation is accelerating in 75% of the categories compared to their six-month pace.

Inflation may be gaining on a broad span in Portugal despite what the major trends seem to show.

What puts Portugal at risk for inflation is that the HICP is already on the razors edge of what is tolerable. While inflation is only at an excessive pace in four categories, in each of those inflation is accelerating further over six months and three months. Moreover, taken broadly inflation is accelerating in most categories regardless of the year-over-year pace. As an offset to these risk factors, we can point to more tranquil inflation according to the domestic national index and we can identify the three-month period as the real focus for inflation's acceleration. This flare up could be episodic and wholly oil-related and reversible. Over six months, the headline HICP is only up at a 2.1% pace while the national rate and its core are up at only a 1.2% pace. Inflation is perking up but not running away.

Energy prices have been a source of pressure for this period and we see that in the evolution of excessive inflation by categories in Portugal where acceleration is concentrated. But the rising breadth of inflation suggests that there is more to it than that.

Portugal is one of the former inflation trouble spots in the EMU. Portugal's inflation rate has not been excessive since October 2012 (excepting a one-month spike to 2.2% in April 2017). That followed an approximately two-year period of constantly excessive inflation in the wake of the tepid inflation caused by the global financial crisis and recession. Core inflation was last excessive in February 2012. Portugal has been controlling its fiscal debt as a percentage of GDP, but that ratio has been creeping up.

Portugal is country to put on inflation watch. It is a small EMU nation and as such it gets a small weight in constructing the EMU inflation picture. Portugal is not likely to send EMU inflation off on a tangent for those reasons. We watch inflation in Portugal mostly to keep tabs on the health of Portugal. However, Portugal remains as one country we will keep on the inflation watch.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief