Global| Mar 23 2020

Global| Mar 23 2020Policy-making in the Time of the Coronavirus

Summary

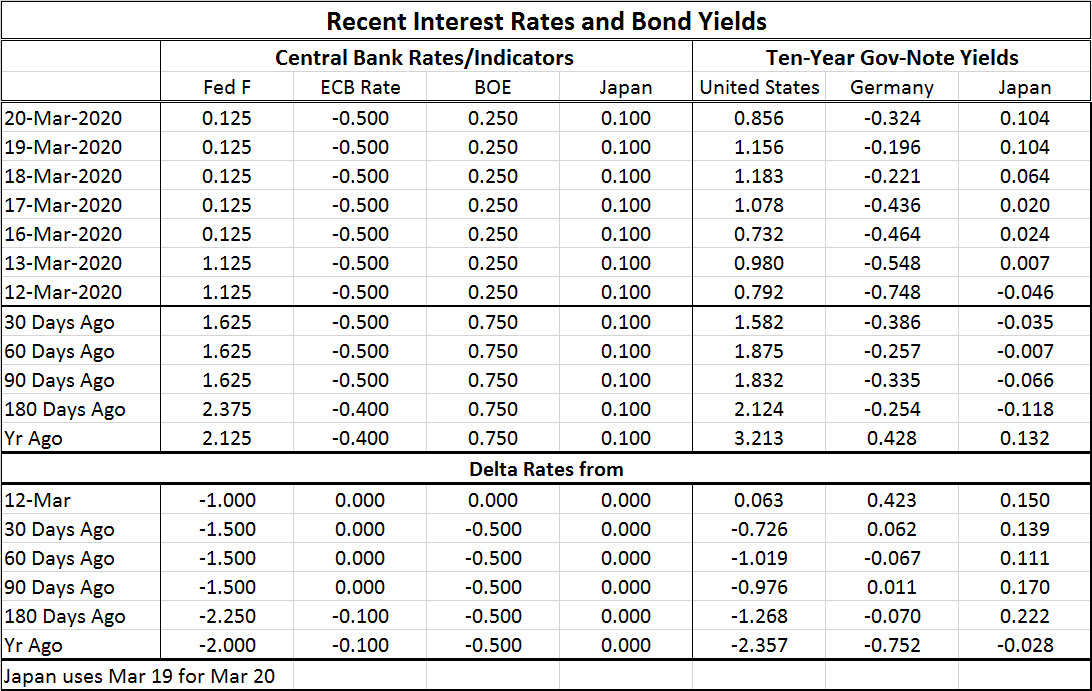

Typically when speaking of policymaking and central banks, we speak of interest rate levels. The chart and table memorialize how little room most central banks have had to work with as the coronavirus has struck and showed its hand. [...]

Typically when speaking of policymaking and central banks, we speak of interest rate levels. The chart and table memorialize how little room most central banks have had to work with as the coronavirus has struck and showed its hand. The U.S. has been able to make significant rate cuts but cuts that still are not substantial enough on their own. Clearly, the baton has been passed to fiscal policy. But what does that mean?

Typically when speaking of policymaking and central banks, we speak of interest rate levels. The chart and table memorialize how little room most central banks have had to work with as the coronavirus has struck and showed its hand. The U.S. has been able to make significant rate cuts but cuts that still are not substantial enough on their own. Clearly, the baton has been passed to fiscal policy. But what does that mean?

As fiscal policy has come into the picture even though it is more targeted and less the fiscal policy fix of your economic textbooks, the behavior of longer term interest rates has become less predictable. Concerns of fiscal excess are definitely in play. Forecasts foresee some outrageous numbers for unemployment rates as well as deeply negative GDP growth rates. Some have hinted of a U.S. unemployment rate as high as 25% to 30%. I have heard forecasts of Q2 growth as low as a -15% growth rate (at a compounded annual rate, of course). Still, that is s massive negative number.

There are no graphs or tables in anyone's data base to depict what we are at risk to. In fact, one amazing fact so far is how few economic data points point to anything out of the ordinary at all compared to what policymakers have done and what people now seem to fear.

We have little to fear but policy itself

I pen this tweaked sub-heading with apologies to FDR. But I believe it to be true. Policy is now inflicting much greater damage on the economy than the virus itself. Speaking as an economist and not as a public health official, let me make it clear that I see policy as a series of tradeoffs. Nothing is 100% sacrosanct. Once the marginal degree of substitution of one thing costs way too much in terms of another, it is time to rethink the trade-off. Policy right now is choking off and killing the economy and small business. Such draconian policy, if left in place too long, will create knock-on effects of its own that will have adverse consequences for public health, the state of this union, and all sorts of social economic factors. I'm not just worried about a GDP figure but about what destroying GDP would do to life.

This is a modern economy. We do not go out and forage for roots and berries or to shoot a deer in the woods when we lose our jobs. People undertake debt and make other economic decisions and some of them are not very good decisions when their backs are against the wall. Despite promises by governments to provide various monies, backstops, loan guarantees and maybe even grants, no one can know the needs of each person as well as that person himself or herself and that is the basis of capitalism. The state is meant to provide the environment for economic activity, but individuals are left to dot the i's and cross the t's. Government, in fact, does not begin to know how to do that for you. Government is set up to take money from you (taxes) not to funnel money to you except in a few specific cases.

The lockdown strategy may be a viable virus killer. But flooding your whole backyard is also a way to water your favorite plant. Some tactics simply reflect overkill. I am very worried about putting public health officials essentially in charge of economic policy. I believe we have gotten to the point where the greater risk to western nations comes from a policy of lockdown than from the coronavirus.

We know from the financial crisis that the government response will not make everyone whole and that government will play favorites. That's one reason not to assume that you can ruin people's economic lives and expect government to crazy glue them back together…just like new.

We also know that we are not facing Ebola or Dengue fever. The China evidence tells us who is most at risk, older people and people with certain pre-existing conditions. So it is time to pivot policy to protect them instead of trying to stamp out the virus everywhere --a job that is in any event nearly impossible and perhaps technically impossible without an abundance of test kits.

The mortality rates for those under 70 or so are about 0.2% and that number seems to include those with pre-existing conditions (Source here). The risk of death to most is low but if the fever spreads beyond the capacity of the healthcare system as it is currently configured special steps would have to be taken. But if the at-risk groups are protected, the peak demand for hospitalization would be greatly reduced. Moreover, policy could pivot to a less invasive mitigating approach and reopen many, many, businesses. Let people in risk groups work from home or target them for aid if they stay at home and could not work. Those who become infected/symptomatic would be required to wait it out at home for 14 days. There are other reasonable approaches beyond the lockdown to manage peak demands.

The coronavirus gives MOST PEOPLE cold- and flu-like symptoms. Children under 10 apparently are very mildly affected. At this writing none in that category have died.

So putting on my economist hat what is the Cost/Benefit here? Does this approach that wrecks the economy and could bring on depression-era unemployment levels make sense to avoid flu-like symptoms? Doesn't it make more sense to build a more protective wall around at-risk groups and limit the overall economic disruption which is beginning to look more like economic destruction?

Small business will be decimated by a lockdown. The more sophisticated ones will figure out how to use the system. But many small business owners will not.

My basic tenant is that the cure should not be worse than the disease and I think we are pushing the envelope if not already exceeding that parameter. It is time to get people to realize what they are hiding from.

Central banks, in addition to whatever rate cutting they could do, have engaged in securities purchases to aid liquidity and offered various liquidity facilities both nationally and internationally; the scope of the action is truly amazing. My first take on this crisis was that the policy objective would be to slow activity so that a macroeconomic fiscal response and even rate cutting was wrong because the idea was not to prop up activity since slowing the spread would mean reducing interpersonal contact and that would slow economic gains. In my view, targeted fiscal spending would have been appropriate even if difficult to arrange. But then policy took this whole thing to an extreme that I frankly did not see coming and still do not understand- the lockdown.

Were this Ebola, I would understand these drastic measures. But it is not. Neither do I jump off the roof of a five-story building to avoid a mosquito bite. Policy actions need to be measured and calibrated. I think it is time to begin thinking about calibration and a more layered calibration before we have done more damage to the economy than we can reasonably repair in a short time. I think that the medical objective of flattening the curve is given a too-high priority. Targeting and protecting at-risk groups is less invasive and might have the same impact.

I think it is time to open our minds to what we are doing. Everything we do has risk. Some people will not drive in a car at all. Some will not drive in the rain. Some will not drive in the snow. Some people will not fly. People can choose their own level of risk as they do in everyday life with perhaps a less draconian governmental mandate as the baseline. That makes sense- much more sense than an economy-wreaking lockdown to avoid flu-like symptoms.

This report is the opinion of the author and may not reflect the views of the website that publishes it.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief