Global| Aug 04 2016

Global| Aug 04 2016PMIs Stage Small Recovery As BOE Cuts Rates and ECB Spats Over Risk

Summary

The U.S. trading day is still unfolding and Europe already has put in a full enough allotment of news and events to fill a week. The BOE shows its colors The long awaited BOE meeting is now out of the way and the BOE has queued up [...]

The U.S. trading day is still unfolding and Europe already has put in a full enough allotment of news and events to fill a week.

The U.S. trading day is still unfolding and Europe already has put in a full enough allotment of news and events to fill a week.

The BOE shows its colors

The long awaited BOE meeting is now out of the way and the BOE has queued up several different points of stimulus. It has cut rates by 0.25%. In doing so, it also has said it is prepared to cut rates again to their effective minimum - adding a bit of `forward guidance' to the policy mix. Governor Mark Carney has made it clear that to him the effective lower bound is a positive number. He said specifically that he is not a fan of negative rates. Now the BOE will expand its balance sheet with asset purchases of bonds, gilts and corporate that will affect the U.K. economy. The plan is to purchase another 60 billion pounds in securities. The final piece is a special term funding scheme that it envisions using possibly to the tune of another 100 billion pounds. The rate cut plan was a unanimous decision, but there was some reluctance associated with other elements of the plan with some MPC members thinking that the bank need not fire such a full barrage at the moment.

BOE outlook has been cut

The BOE forecast on growth for the year ahead has been cut and the bank warned of minimal growth in the second half of the year. It looks as though Governor Carney has decided that marginal economic plans are not very effective and has decided to put a full menu on the table for maximum impact from the start. While estimates of growth have been reduced, the bank has put markets on notice that it is prepared to do more, charging the day's announcements with extra vigor.

ECB and Germany at odds?

Meanwhile, the ECB seems to have a war of words in play. While Jens Weidmann has today said that Brexit seems to have posed little risk and that the recovery from the unexpected announcement seems to be complete, he went to say that he saw no reason to adjust the outlook for the EMU economy in the wake of Brexit. However, the ECB put out a statement acknowledging the apparent small impact of the unexpected Brexit move but at the same time pointing to weaker growth and more fragility in the global economy. Oil prices have dipped below $40/barrel then recovered again. It seems that the ECB and Mr. Weidmann have different views of the risks and of the policy needs in the period ahead. And that is not exactly a shocking development. At each turn of stimulus, Germany has looked for a way to blunt it or to turn it back. With the strongest economy in the EMU, Germany is the one -if any- at risk to the emergence of inflation.

Global economy does better, but still poorly

Comprehensive readings on the global economy became available today that allow us to look at the global economy overall and by sector as well as by emerging vs. developed market divisions.

Manufacturing improves globally, but services languish

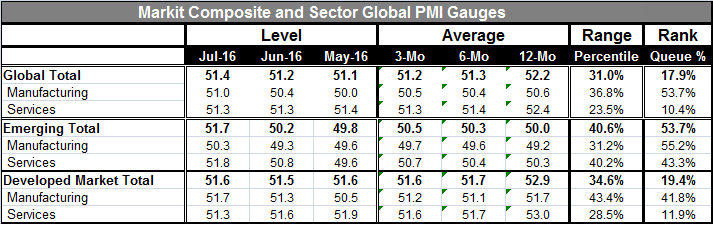

Viewed in this way, there was a small overall improvement in the global economy in July with the global composite index up to 51.4 from 51.2. Manufacturing is up to a 51.0 reading from June's 50.4 while the services sector rating has stayed flat at 51.3 in both June and July. Both sectors show growth although not much of it. When we look at these gauges in some historic perspective back to January 2011, we find the current month's global index ranks only in its 17th percentile for the period leaving it at a very weak value. Manufacturing is much firmer than services with a 53.7 percentile standing in this historic queue of data. The services sector's standing in its 10.4 percentile position has been weaker than this only about 10% of the time over the last 67 months.

Emerging economies take a step ahead

Emerging economies, with a series of composite PMI diffusion readings clustered just a bit above the breakeven 50 mark over the last year, showed some improvement in July. The emerging market composite index rose to 51.7 from 50.2, making its largest month-to-month gain since June 2014. That monthly gain was led by manufacturing that gained one point on its diffusion index, its largest one-month rises since March. The services sector gained a point month-to-month and that builds on a slightly stronger gain from the month before. Still the emerging market composite PMI has a standing at its 53.7 queue percentile, above its median and led by a 55.2 percentile standing for manufacturing and a weaker 43.3 percentile standing for services. The emerging markets have broken a three-month string of below 50 readings for manufacturing this month, implying that the manufacturing the sector is now increasing.

Developed market economies stagnate

For developed economics, conditions did not materially improve in July as the overall sector index for the group rose to just 51.6 from 51.5. While this is still a reading that connotes growth for this period, evaluated since January 2011, it is a reading that stands in the lower 19.4 percentile of its historic queue of readings. Developed market economies manufacturing sectors moved higher in July to a reading of 51.7 from 51.3, pushing it up to a queue standing into its 41.8 percentile, a still-weak reading that remains below its period median. Services weakened in July to 51.3 from 51.6, falling to a very anemic 11.9 percentile queue standing. The services sector has been weaker only about 12% of the time since January 2011.

Emerging market forces/tensions

On balance, we can see the global forces developing. China in data released yesterday showed an improved manufacturing sector vs. weaker services; continuing to show a very weak services sector. But outside China, services in emerging markets were improving not slipping.

EMU and Germany

In the EMU and Germany, the manufacturing sectors slipped while services firmed as the total gauges for Germany and for the EMU improved. But Germany's manufacturing sector is starting to shake off its dislocation and has risen to an 82nd percentile ranking for this recovery period. In the EMU, manufacturing and services as well as its overall gauge continue to be stuck with intermediate readings. Germany may feel that it is regaining its legs in the wake of the financial crisis despite the Brexit shock while the rest of Europe seems to be much more stuck in the same morass it has been mired in all recovery long.

The global picture

Global conditions, despite some more positive turn of events in July, remain weak. EMU-wide recovery forces are still muted. Money and credit are still not responding to past monetary stimulus in the EMU. The U.K. move today should advantage the U.K. economy at the expense of the EMU to some extent. Looking ahead, this is a powerful new bout of stimulus and it is driving the pound exchange rate lower. On balance, we can see all these shifting gears, but the bottom line is that, shift as they will, their pace is still slow and there is still a risk of falling out of gear completely. And the ECB's position on risk remains the one mostly clearly in force and applicable to the global economy today. The global economy made its recovery peak in early to mid-2014 and has since been slipping. There is now only a small sense of stabilization and a pick up that is too nascent to make it the basis of any new policy assessment. And as to Brexit, there may be another shoe left to drop when the real impact of Brexit hits home not just the market reaction to the event.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief