Global| Mar 01 2016

Global| Mar 01 2016PMIs Drop in Step with Unemployment Rates

Summary

We are visited today by more dissonance in data as global and EMU PMIs fell, showing broad-based declines as unemployment fell across the EMU, in Japan, and has been staying low in the U.S. I guess we should cut the Fed some slack on [...]

We are visited today by more dissonance in data as global and EMU PMIs fell, showing broad-based declines as unemployment fell across the EMU, in Japan, and has been staying low in the U.S. I guess we should cut the Fed some slack on its confusion about how the economy is operating. Mixed signals are enduring. But the ECB has held its focus on stimulus and markets took the PMI declines today as more evidence that the ECB would be forced to act. Still, interest rates already are low. In Japan, the first negative rate auction of government securities was completed as people paid the government to hold their monies.

We are visited today by more dissonance in data as global and EMU PMIs fell, showing broad-based declines as unemployment fell across the EMU, in Japan, and has been staying low in the U.S. I guess we should cut the Fed some slack on its confusion about how the economy is operating. Mixed signals are enduring. But the ECB has held its focus on stimulus and markets took the PMI declines today as more evidence that the ECB would be forced to act. Still, interest rates already are low. In Japan, the first negative rate auction of government securities was completed as people paid the government to hold their monies.

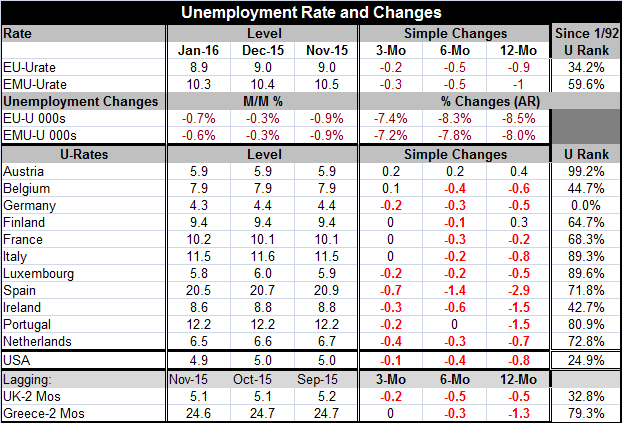

In the EMU, right alongside weak PMI data, we have a drop in the rate of unemployment as the EU rate dropped one tick to 8.9% in January and the EMU rate fell one tick to 10.3%. The unemployment rate in Germany fell one tick to 4.3%, the lowest rate since German reunification.

Overview on manufacturing PMIs in February

But the manufacturing PMI data continue to be weak. While the U.S. ISM manufacturing index rose to 49.5 this month, it stayed below 50 for the fifth straight month. Across most of the world and in the EMU, manufacturing PMIs fell broadly (weakened). As a result, a representative global list of 15 manufacturing PMIs finds only four them with PMI readings above their 50th queue percentile standing historically with seven having raw diffusion standings below 50 outright in January. Moreover, 13 of 15 PMIs have PMI diffusion values below 51. Even in those PMIs that show manufacturing advancing, the rise is quite mild. Vietnam, Canada and France all show PMI rankings in their respective 70th percentiles in terms of their queue standings. The EMU reading is above its 50th percentile at its 53rd percentile. But apart from these four, the remaining manufacturing readings are weak. Brazil, China and the U.S. have queue standings below their respective 15th percentiles. Higher than this but below their 40th percentiles are Germany, the U.K., Canada, Japan, Russia, India, Taiwan, and Turkey.

Manufacturing vs. services and jobs

Obviously, it is bit difficult to make sense of this sort of split. Manufacturing is a more volatile sector than services so we expect it to be weaker/weakest when the economy gets weak. Employment and unemployment conditions are relatively stronger than manufacturing because service sector output and employment have been relatively better maintained.

Still, unemployment is a lagging variable-coincident at best. It may not have such a different dynamic that than manufacturing as much as its dynamic lags behind it. This is the worry of many economists, the ECB, but apparently not a worry by those at the Fed.

Unemployment rates in EMU in January

Unemployment rates fell in January alone in six of 11 early unemployment reporters in the EMU. EMU area unemployment rose only in France, among those listed in the table. Still, unemployment drops are widespread over three months with six countries showing drops, three countries steady and unemployment rising in only two countries. Over six months unemployment rates falls everywhere except Portugal where unemployment is flat. Over 12 months unemployment rates fall in nine of 11 countries in the table. Austria and Finland are the exceptions with increases on that timeframe.

Unemployment rate rankings show Austria with one of the highest rates in its history in the top 0.8% (even so, Austria has the third lowest unemployment rate in the table in January). Fortunately, it is an exception. But Italy, Portugal and Luxembourg have unemployment higher than it is in January only 20% of the time or less. The Netherlands and Spain have unemployment higher only 30% of the time or less. Only Germany, Belgium and Ireland have unemployment rates below their queue medians (rankings below 50%). And both Belgium and Ireland have rankings in their 40th percentile range still not too far below their respective medians. Once again Germany is in a world of its own.

Between the manufacturing PMIs and unemployment rate differences, there is plenty to be confused about or reasons to draw different conclusions on the economy. Shortly, we will get the services PMIs for February to fill in the picture and `take sides.' But as of January, the services PMIs were not painting a different picture. Worldwide most services sectors are lower over three months and six months with mixed results over 12 months.

Mommy, where does inflation come from?

Economists have long been divided about `how the world works' and `what the true inflation process is.' This year a paper offered at the K.C. Fed's Jackson Hole Symposium concluded that there is a lot we don't know about inflation as it found all approaches lacking. The differences in the fundamental views of policymakers and economists about the inflation process, shows thorough in terms of countries' and central banks' approaches to policymaking. Germany, clearly the strongest EMU country and closest to overheating, is wary of the usefulness of any further monetary stimulus. The rest of the EMU, more or less, is anticipating more monetary action. Germany also is an advocate of holding countries' feet to the fire of the Maastricht debt and deficit rules.

Germany itself has been trying to run an outright budget surplus and was on track to do that until it had to foot the bill for migrant upkeep. Now the migrant issue is getting to be a serious problem with the Macedonia border shut. The refugee camp at its border is seriously overwhelmed and migrants have been trying to break down the not-so-great-wall-of-Macedonia to escape overcrowding and continue their journey. Europe has been warned by a UN agency that full-blown refugees crisis could be on the cusp of breaking out. That can't be good.

Whether the migrant issue is big enough to unseat trends in the EMU is unclear. But it is threatening the Schengen agreement which is the most loved aspect of EMU membership that permits free movement among EU members in the EU region. It is clear that monetary policy is now stepping out on some very thin ice. There be some evidence that it is working to stimulate lending, but it is still too soon to be sure. Europe is now balancing several significant risks.

The mixed signal for real economic data as well as the intrinsically different ways of looking at the economy are contributing to policy uncertainty and disagreement. I wonder, even if the economy's true needs show themselves, will policymakers be able (i.e. willing) to shift their positions and do what is necessary? If that turn is to weaker growth, I wonder what they will do at all. This question is the strongest argument for policy to do something more supportive of growth now instead of doing something restrictive. In the U.S., that is still not the way the Fed sees things, at least in public. In Europe, there is lots of lip-service that more is coming while doing absolutely nothing. It makes me wonder.is prayer a viable economic policy?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief