Global| Nov 03 2005

Global| Nov 03 2005PMI Surveys Around the World in October: Europe Looks Better, China Does Not!

Summary

Purchasing manager surveys suggest economies in Europe and Japan are improving, while China might be showing signs of moderation. These monthly polls are published by NTC Research in London and conducted by local business [...]

Purchasing manager surveys suggest economies in Europe and Japan are improving, while China might be showing signs of moderation. These monthly polls are published by NTC Research in London and conducted by local business organizations, such as Nomura in Japan and Reuters in the UK. The results are shown as diffusion indexes, which show the percentage of respondents that report increasing business for a given month. As with the ISM data in the US, manufacturing is reported on the first business day of the following month, with nonmanufacturing (mostly services) following two days later. The indexes are calculated as the percentage reporting rising business plus half of those reporting a flat performance. The resulting indexes are then seasonally adjusted.

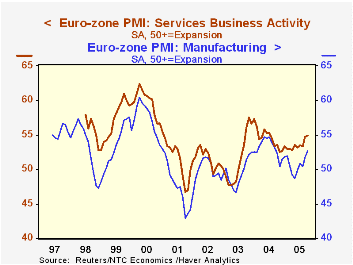

In October, companies in the Euro-Zone saw business increase more broadly, with a manufacturing index of 52.69 and services, 54.95. Both show notable improvements from earlier in the year. European manufacturing faced a mild contraction (readings below 50%) in the spring and the service sector experienced sluggish growth in the year through August before picking up smartly in the last two months. Patterns in the UK recently have been somewhat similar, with a brief outright contraction in manufacturing during the spring, but some subsequent pickup; activity at UK service companies has held within a persistent and narrow range since the middle of 2004, indicating steady moderate growth.

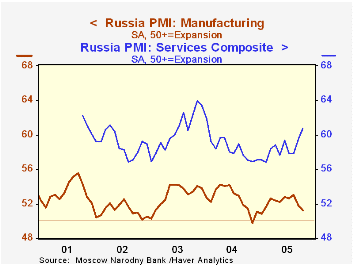

In contrast, growth in Russia's manufacturing sector has slowed in the last two months. This PMI index has ranged from roughly 50 to 55 over the last several years, with September and October dropping into the lower end of the span. Services, though, are holding up well with some strengthening evident so far in 2005. Price behavior in these sectors varies as well: input prices for manufacturers show a trendless, but widely varying oscillation, while service companies' input prices have risen at a dramatically larger number of firms recently.

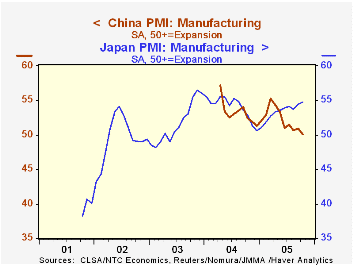

Only manufacturing surveys are taken in Japan and China. Japanese factories appear to be doing better, with that index ratcheting upward all year long. This firming even includes employment; this index worked its way above 50% during 2004, and since March of this year, it has averaged 52.5. While not high by world standards, it looks good for Japan. The survey began in October 2001, and both the total index and the employment component were down around 40 at the time. Such improvement in manufacturing seems at odds with the Japanese government's synthetic indexes reported here Monday by Louise Curley, in which marked slowing or even decline is indicated for the Japanese economy in Q3. Clearly, at the least, various data may diverge over brief time periods. In this case, the synthetic indexes are meant to describe demand conditions, while the PMI survey looks at supply, and that in only one sector. This makes judging the prospects for even the direction of business in Japan a tough call.

China is even more intriguing. Its manufacturing index has dropped steadily since its inception 18 months ago, and now stands just barely above 50%. The moderation appears in most of the survey components, including new orders and backlogs. Notably, output prices are below 50%, indicating declines at more companies than have increases. And in the last three months, employment at factories has been ever so slightly below 50%, basically indicating that it has stopped growing. These results feel odd for a country with GDP growth at about 9-1/2%, led by manufacturing. Perhaps the pattern is a relative one. With such a high growth trend, merely keeping up pace may give the impression of slowing, particularly from the high base that obtained in the spring of 2004 when the survey started. Asia is clearly full of interesting economic developments. We eagerly await more information on how they're doing.

| October 2005 | September 2005 | |

|---|---|---|

| Euro-Zone | ||

| Manufacturing | 52.69 | 51.74 |

| Services | 54.92 | 54.65 |

| UK | ||

| Manufacturing | 51.72 | 51.52 |

| Services | 56.14 | 55.05 |

| Russia | ||

| Manufacturing | 51.23 | 51.83 |

| Services | 60.75 | 59.48 |

| Japan | ||

| Manufacturing | 54.74 | 54.46 |

| China | ||

| Manufacturing | 50.07 | 50.85 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief