Global| Jan 23 2009

Global| Jan 23 2009PMI Indices for EMU Bounce – Dead Cat or Live One?

Summary

Hooray! The MFG and Services PMIs for Europe in January have bounced. It’s too soon to call it a bottom but since they are bouncing off historic- or near-historic lows, maybe we have seen the worst of decay. Even if that is true it is [...]

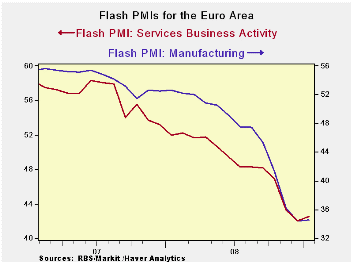

Hooray! The MFG and Services PMIs for Europe in January have

bounced. It’s too soon to call it a bottom but since they are bouncing

off historic- or near-historic lows, maybe we have seen the worst of

decay. Even if that is true it is a far cry from saying we are about to

embark on recovery.

What it means - At a reading of 34 for MFG, the sector is

telling us that about 34% of the industries are expanding… (That is

strictly speaking an improper interpretation since the PMI reading is

all the ‘up’ readings plus ‘half the unchanged responses’ and there are

myriad ways to get that result. A given PMI reading does not tell you

how many, or which proportion, of industries are expanding. But the

reading of 34 is ‘as if’ 34% were rising and the rest falling although

fewer may be rising and twice the residual might be unchanged. I will

use this short hand of treating the PMI as if it were an ‘up only’

index for simplicity but the reader should understand that the truth is

a bit more complex- I think nothing is lost by this expositional

device.). For services the reading of +42 is coming off that (shorter)

series’ all-time low.

Lots of weakness ahead - In any event it is clear that these

two measures can rise for some time and still not get back to neutral

(a reading of 50 is neutral- half the sectors expanding, half

contracting).

‘Neutral’ is not ‘normal’ - And of course ‘neutral’ is not the

same as ‘normal’. When you put your car in ‘neutral’ is neither in

‘drive’ nor ‘reverse’. If we were to average what gear your car were in

most of the time the average would not be close to neutral. Similarly,

since July 1998 when the services measure was launched it has averaged

54.2. Over the same span the MFG index has averaged 52. On balance more

sectors are expanding than contracting in normal times. So the current

readings are a very great distance away from being ‘normal’ and it

should take a good deal of time to get back to normal.

Diffusion increases do not necessarily mean that output

increases - When these diffusion indices rise, until they surpass a

reading of 50, they are indicating contraction at a slower pace but

still contraction and not expansion.. For now the PMIs are saying that

the worst – most severe phase of the contraction - is behind us, not

that recession is ending. And that is the message only if the December

bottoms stay in place and are not replaced by new weaker readings.

More weakness ahead - Rest ‘assured’ that more declines lies

ahead for conventional economic variables even if the diffusion indices

continue to rise from their lows.

Diffusing as Mr Sensitivity - Diffusion readings are very

valuable because they are so timely and because they are sensitive.

Formally the PMI indices are measures are gauges of the BREADTH not of

its strength. But everyone treats theses measure of breadth as if they

are of strength. Financial experts are well aware that is not so. For

stock markets analysts (for example) always looked at big ‘up’ or

‘down’ days in the stock indices to see if the breadth reinforced the

trend or not. Breadth in fact is not the same as strength – but they

are highly correlated. So again be careful how use diffusion data. They

often are the first whiff of slowdown or of bottoming. But they are

indicators and are not real economic variables so be careful how you

interpret them.

| FLASH Readings | ||

|---|---|---|

| Markit PMIs for the Euro Area | ||

| Markit PMIs for the Euro Area 15 | ||

| MFG | Services | |

| Jan-09 | 34.53 | 42.47 |

| Dec-08 | 33.87 | 42.06 |

| Nov-08 | 35.58 | 42.47 |

| Oct-08 | 41.10 | 45.76 |

| Averages | ||

| 3-Mo | 36.85 | 42.62 |

| 6-Mo | 41.74 | 45.19 |

| 12-Mo | 46.51 | 47.93 |

| 126-Mo Range | ||

| High | 60.47 | 62.36 |

| Low | 33.87 | 42.06 |

| % Range | 2.5% | 2.0% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief