Global| Apr 19 2007

Global| Apr 19 2007Philadelphia Index Remains Near Zero

Summary

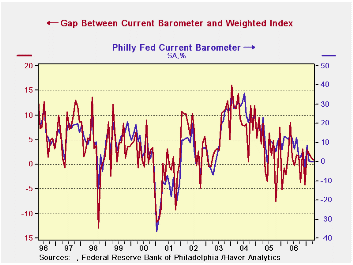

What is interesting is that the weighted Philly index and the barometer are related in particular way. The gap between the barometer and weighted index is a directional statement on the economy and functions similar to the Philly [...]

| · The table below contains the main elements of the Philadelphia Fed regional manufacturing index. At the far right another column introduces a different index. This index is what the Philadelphia Fed index would be if it used ISM weights. But Philadelphia does not do that. Instead, it has a separate survey on managers where they tell you how they feel. Recently they have been candidates for a new Excedrin™ headache number “XXX” commercial. |

|---|

| FAO-Index | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | Current Index | Current New Orders | Current Shipment | Deliveries | Inventory | Backlog | Pr:Pd | Pr:Rcd | Current Employment | Worked Hours | INDEX Weighted |

| Apr-07 | 0.2 | 2.8 | 4.3 | -11.9 | -3.1 | -13.7 | 24.3 | 5.2 | 2.5 | 5.5 | -0.6 |

| Mar-07 | 0.2 | 1.9 | 6.8 | -13.2 | -3.7 | -20.9 | 21.8 | 16.3 | 2.3 | -4.9 | -1.2 |

| Feb-07 | 0.6 | -0.5 | 1.7 | -6.3 | -1.9 | -10.5 | 15.8 | 9.4 | -0.4 | -12.9 | -1.7 |

| Jan-07 | 8.3 | 1.3 | 23.9 | -7.1 | 0.4 | -15.4 | 11.9 | 11.6 | 7.9 | 1.8 | 5.3 |

| Dec-06 | -2.3 | -0.9 | 14 | -4.9 | -0.9 | -18.6 | 19 | 8.9 | 7.5 | -2.3 | 1.9 |

| Nov-06 | 5.4 | -1.1 | 7.8 | 1.8 | 5.3 | -5.5 | 25.2 | 7.4 | 3 | 2.3 | 2.2 |

| Oct-06 | 2.3 | 10.7 | 6.1 | -4.8 | 10.9 | -10.5 | 32.7 | 17.2 | 10.4 | -0.4 | 5.9 |

| Sep-06 | 2.3 | 0.2 | -4.4 | 0 | 4.7 | -3.8 | 37.8 | 20 | 10.3 | 5.4 | 0.6 |

| Aug-06 | 12.6 | 12.8 | 20.3 | 1.4 | 6.8 | -2 | 46.6 | 17.3 | 8.1 | 11.7 | 10.8 |

| Jul-06 | 6.5 | 9.9 | 10.7 | -1.3 | 0.5 | -6.5 | 49.5 | 17.6 | 11.7 | -2.4 | 6.7 |

| Jun-06 | 12.1 | 17.2 | 18.3 | 0.2 | -3.5 | -0.7 | 49.3 | 16 | 8.2 | 8.2 | 10.6 |

| May-06 | 13.6 | 3.5 | 14 | 9 | -5.3 | -2.8 | 53.9 | 11.3 | 2.9 | 9.6 | 5.1 |

| Apr-06 | 11.7 | 12 | 17.7 | -2.9 | -9.7 | 5.6 | 30.4 | 15.1 | 16.3 | 7.9 | 9.8 |

| Mar-06 | 12.9 | 21.1 | 23.2 | 2.5 | 11.6 | 4 | 22.5 | 15.7 | 7 | 7 | 15.0 |

| Feb-06 | 13.2 | 12.9 | 23.5 | 6.6 | 9.3 | 10 | 32.3 | 18 | 10.5 | 7 | 13.9 |

| Jan-06 | 6.4 | 11.5 | 19.5 | 7.8 | 6.6 | 0.3 | 40.2 | 20.3 | 11.8 | 7.4 | 11.6 |

| Dec-05 | 12.8 | 7.3 | 5 | 1.5 | 3.9 | 0.8 | 45.8 | 28.1 | 7.5 | 5.5 | 5.2 |

| Nov-05 | 10.7 | 13.2 | 21.5 | 5.7 | 3.8 | -8.2 | 53.9 | 31.8 | 18.4 | 12.4 | 12.2 |

| Oct-05 | 5.1 | 19.8 | 19 | 0 | -2 | -2.9 | 25.6 | 12.7 | 15.9 | -1.2 | 12.6 |

| Sep-05 | 8.8 | 1.3 | 16.2 | -0.7 | -0.9 | -8.6 | 50.5 | 6.6 | 3.9 | 2.6 | 4.0 |

| Aug-05 | 10.6 | 15 | 14.3 | -0.2 | -8 | 3.9 | 28.1 | 3.1 | 7 | 1 | 8.7 |

| Jul-05 | 10.1 | 7.2 | 12 | -1.3 | -8.7 | -8.1 | 30.4 | 13.1 | 2.4 | 5 | 3.7 |

| Jun-05 | -1.1 | 4.8 | 9.9 | -10.8 | -0.8 | -16 | 28.3 | 12.4 | 8.5 | 4.3 | 2.4 |

| May-05 | 9.1 | 16.5 | 18.8 | 0 | -0.9 | -3.6 | 31 | 16.5 | 8.7 | -0.7 | 10.5 |

| Apr-05 | 23.2 | 19.3 | 28.6 | 4.1 | 0 | -3.8 | 49.1 | 26.6 | 12.3 | 15.3 | 14.8 |

| Mar-05 | 14.1 | 15.3 | 15.5 | 1.3 | -2.4 | -3.3 | 33.9 | 18.1 | 12.2 | 8 | 9.9 |

| Feb-05 | 20.1 | 12.3 | 22.2 | 3.5 | -5.2 | -1.8 | 45 | 23.6 | 11.4 | 7 | 10.6 |

What is interesting is that the weighted Philly index and the barometer are related in particular way. The gap between the barometer and weighted index is a directional statement on the economy and functions similar to the Philly future index. On the left we plot the gap (the barometer less the weighted Philly values) vs the barometer itself.

You can see that gap between what managers say and what the index actually does tracks the direction of the index itself. In other words when managers are more optimistic they offer a barometer reading that is stronger than the component’s weight composite calls for. When conditions are getter weaker, they give a reading that is less buoyant relative to the surveyed components. It turns out that when managers are so pessimistic that the barometer reading is lower than the weighted reading it is a very bad sign for the economy. The good news is that we are not there yet. The bad news is that other Philadelphia measures have already crossed the line and are now worrisome in their degree of weakness.

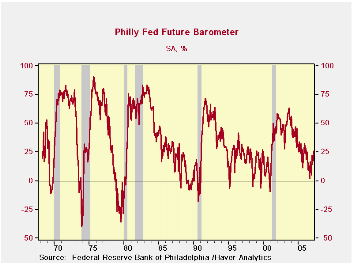

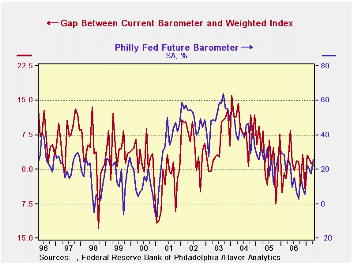

The Philadelphia Fed’s future barometer is a good example of what is disturbing. It has very regular cyclical properties, as you can see. Generally it turns negative before recession. Often it is actually rebounding even before the onset of recession or shortly after the onset of recession. In 2007 it is giving off all the recession signals except for having broken the zero line on the graph. However, we can form a second gap index for the future components just as did for current conditions. And that index performs just as the current conditions index performs. When plotted it has cut though the zero line and rebounded as it does in recession periods.

Next we show how the current gap indicator tracks the future barometer from the Philadelphia Fed. It is not too surprising that managers who respond to the survey are CONSISTENT in calling future conditions better at the same time they are evaluating current conditions to be better than their own assessment of the main business components at the time of survey.

The point of all this discussion is to head off some of the criticism of this indicator. There are some economists who do not like it or trust it and think the Philadelphia survey is too small and too unreliable. But what is interesting about it is how the various components of the survey give off compatible signals and how those signals have been so closely correlated in the past with the cycles in the NATIONAL ECONOMY. It is and has been a better NATIONAL indicator than the ISM.

I have not been a pessimist about the prospects for this economy. But the Philadelphia Fed MFG survey with all its consistent slow-down signals is not giving us any room to be very optimistic. I also run a specific recession diagnostic off this index and it has been forecasting a national recession for several months running. That is not a finding that has found favor. The Philadelphia Fed survey has, using my method, been fighting off a recession signal starting back in March of 2005. It has turned that signal on and off several times since, but it now has six monthly recession signals in a row. Historically the lead time from this index’s signal to the onset of recession is 13 to 18 months. So we are touch longer than that from the first signal, but then signals are still in the offing.

Alan Greenspan has spoken of recession and called the probability about one-third and then said he thought that the economy would grow. Other economists have noted that a one-third probability of recession is not that high. But now I have this Philadelphia Fed index that is so persistent in emitting this signal that it is all a bit frightening. We also have persistent, but not yet deep weakness in the LEI (Leading economic Index). Jobless claims have recently ratcheted higher. While housing measures seem to have stabilized and job growth still seems at least firm (strong enough to drive the unemployment rate down!) the economy is indeed sending out some very mixed signals. If it were food it be Chinese: sweet and sour.

We have noted the wide disparity in the various regional indicators. Maybe Philadelphia is going to prove to be not so representative of the nation in 2006 and 2007 as it was in the past. But it is certainly giving off weak signals and there is nothing in the index to reassure us.

The Philadelphia barometer has been below the level of 9 for six months running. The orders index has not been above 2.8 in that period. Shipments have held up a lot better but they are still below the mid point of their normal range of values and well below their average and median readings. But employees hired and hours-worked are still above average and median norms. Job data are of course, notorious for lagging.

Even so…. what does not SMELL like recession about this report is– like the LEI- the fact that the rate of change is so slow. The Philadelphia Fed report says that the MFG economy is just sitting there and has been doing so for six months. Is this a regional problem or a national trend? Will manufacturing drag the economy down or will services hold it up? On this score I am still betting on services but recent economic reports have not been kind to this view. The regional disparities give us some reason to distrust the Philadelphia track record as a national bellwether. But we do that at our own risk. Remember, the famous last words are, ‘this time it will be different.’

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief