Global| Oct 26 2004

Global| Oct 26 2004Pessimism Among U. K. Manufacturers Rises in the Fourth Quarter

Summary

The fourth quarter survey of industrial trends in the United Kingdom undertaken by the Confederation of Business Industries (CBI) revealed a sharp increase in pessimism among the 770 manufacturers participating in the survey. The CBI [...]

The fourth quarter survey of industrial trends in the United Kingdom undertaken by the Confederation of Business Industries (CBI) revealed a sharp increase in pessimism among the 770 manufacturers participating in the survey. The CBI publishes the percent balance between those respondents who have a positive outlook and those who have a negative outlook on a number of business issues.

There were 10% more pessimists regarding domestic prospects than optimists in the latest survey. This compares with an excess of optimists of 7% in the third quarter survey. The pessimists and optimists were equally balanced regarding the outlook for exports in the fourth quarter survey, compared with an excess of optimists of 3% in the previous quarter.

One bright spot in the survey is the outlook for output over the next three months. In spite of the decline in optimism and a one percentage point drop in the balance, 6% more respondents increased rather than decreased output over the past three months and the balance of those expecting to increase over those expecting to lower output in the next three months rose to 14% from 6% in the third quarter..

In contrast to the optimism among manufacturers regarding output over the next three months is the pessimism regarding the outlook for capital spending and employment. The balance between those who expect to increase over those who expect to decrease spending on buildings has gone from -16 in the third quarter to -26 in the fourth. The comparable balances for spending on plant and equipment are 0 and -17. Furthermore, the balance between those who expect to increase over those intending to decrease employment in the next three months was -15 in the fourth quarter, compared to -7 in the third quarter.

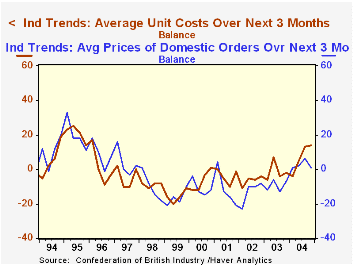

In the first quarter of this year, the balance of those expecting prices to rise over those expecting them to fall was, for the first time since early 2001, greater than the balance of those expecting costs to rise over those expecting them to fall, suggesting that the respondents to the survey were looking forward to better profit trends. This relationship was, however, short lived and once more the balance of those predicting an increase over those predicting a decrease in costs is greater than the balance of those predicting a rise over those predicting a fall in prices. The trends are shown in the attached chart.

| CBI SURVEY (Percent Balances) |

Q4 04 | Q3 04 | Q4 03 | Q/Q Pt Chg |

Y/Y Pt Chg |

2004 | 2003 | 2002 | 2001 |

|---|---|---|---|---|---|---|---|---|---|

| Business Optimism Domestic | -10 | 7 | -7 | -17 | -3 | 7 | -17 | -6 | -27 |

| Business Optimism Exports | 0 | 3 | -8 | -3 | 8 | 7 | -15 | -6 | -22 |

| Output, past three months | 6 | 7 | -19 | -1 | 25 | 11 | -12 | -13 | -4 |

| Output, next three months | 14 | 6 | -4 | 8 | 18 | 13 | -4 | 5 | -2 |

| Domestic Prices, next three months | 1 | 6 | -7 | -5 | 8 | 3 | -10 | -13 | -12 |

| Unit Cost, next three months | 14 | 13 | -2 | 1 | 16 | 7 | -1 | -7 | -4 |

| Capital Expenditures, buildings | -26 | -16 | -29 | -10 | 3 | -18 | -29 | -26 | -24 |

| Capital Expenditures, plant & equip | -17 | 0 | -14 | -17 | -3 | -3 | -21 | -23 | -15 |

| Employment, past three months | -4 | 2 | -21 | -6 | 17 | -6 | -25 | -31 | -15 |

| Employment, next three months | -15 | -7 | -26 | -8 | 11 | -11 | -28 | -26 | -21 |

More Economy in Brief