Global| Mar 17 2021

Global| Mar 17 2021Passenger Car Registrations Continue to Sag in Europe

Summary

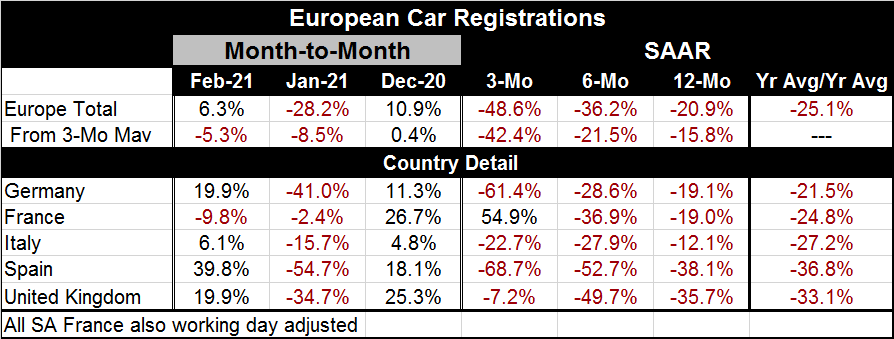

Passenger car registrations in Europe rose by 6.3% m/m in February but only after falling by 28.2% in January. Registration rose in the month in four of the five countries in the table, with France being the exception. This month’s [...]

Passenger car registrations in Europe rose by 6.3% m/m in February but only after falling by 28.2% in January. Registration rose in the month in four of the five countries in the table, with France being the exception. This month’s gain does not shift the trend.

Passenger car registrations in Europe rose by 6.3% m/m in February but only after falling by 28.2% in January. Registration rose in the month in four of the five countries in the table, with France being the exception. This month’s gain does not shift the trend.

Over three months, however, registrations in Europe fell at a 48.6% annualized rate. Registration growth rates fell in extreme double-digit terms in Spain (-68.7%), Germany (-61.4%) and Italy (-22.7%). Registrations fell at only a 7.2% annualized rate in the United Kingdom while sales rose over three months in France.

Sequentially European sales fell over 12 months and fell faster over six months then fell faster still over three months. That pattern is replicated by a calculation of growth rates from three-month moving averages as well. Germany and Spain also exhibit this sort of sequential deterioration in growth rates. Italy is a minor exception with growth slightly less weak (but still falling sharply) over three months compared to six months. The U.K. is a bit more of an exception as it posts only a 7.2% annualized decline over three months although showing sharply declining results over both 12 months and six months with registrations the weakest over six months. France logs a three-month increase of a substantial magnitude to solidly break with the rest of Europe as French registrations rise at a 54.9% annualized rate over three months.

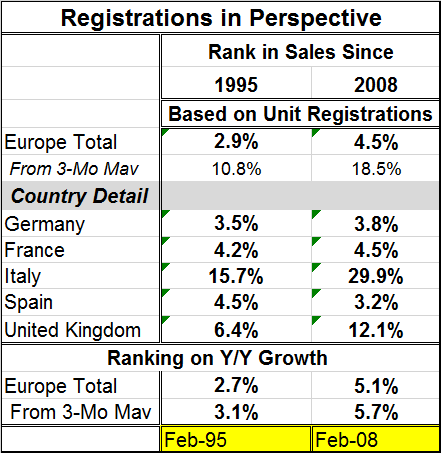

The table to the left ranks the registrations results for each country and for Europe on two horizons based on unit registrations. I will confine my attention to the rankings since 2008. On that basis, surveys of European unit registrations rank in the lower 4.5% of all reported monthly registrations on the period. Smoothing registrations (ranking the trailing three-month moving average) produces a higher rank but one that is still quite low, in its 18th percentile.

The table to the left ranks the registrations results for each country and for Europe on two horizons based on unit registrations. I will confine my attention to the rankings since 2008. On that basis, surveys of European unit registrations rank in the lower 4.5% of all reported monthly registrations on the period. Smoothing registrations (ranking the trailing three-month moving average) produces a higher rank but one that is still quite low, in its 18th percentile.

Registrations in Italy have a 29.9 percentile ranking; in the U.K., a 12.1 percentile ranking; sales in Germany France and Spain each post rankings below their respective fifth percentile. All of these results are very weak.

Registrations compared on a longer timeline back to 1995 are even weaker in every case.

At the table bottom, I rank total European registrations based on their year-over-year growth rates for each period. The results are not much different than for unit registrations. The registration growth rate has a lower 5.1 percentile standing similar to its unit-based ranking. The ranking of three-month averages’ year-on-year performance is only slightly better at a 5.7 percentile ranking. As with unit registration rankings on data back to 1995, the longer period rankings are slightly weaker but not in a way that would change the story at all.

The graph shows that year-on-year growth rates for registrations are still fading. There was a sharp plunge when the Coronavirus hit, then a rebound back near to a pre-Covid-19 pace for registrations, and then a second deterioration set in. Currently, that erosion is still in progress and is still worsening.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief