Global| Oct 07 2019

Global| Oct 07 2019Orders Suggest That Germany Flirts With Some Sort of Recession

Summary

Germany's manufacturing orders continue to run weak. Overall orders are still declining. Total orders have fallen month-to-month five times in the past eight months. Currently, order weakness concentrates in the domestic sector where [...]

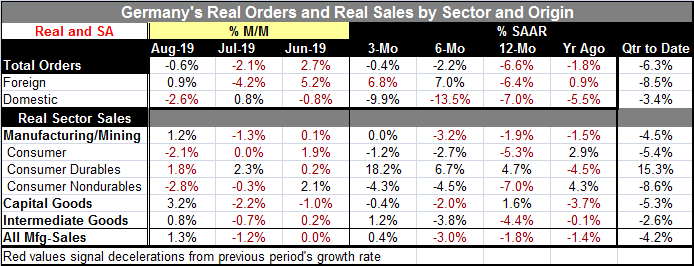

Germany's manufacturing orders continue to run weak. Overall orders are still declining. Total orders have fallen month-to-month five times in the past eight months. Currently, order weakness concentrates in the domestic sector where orders have fallen sharply in August and are lower month-to-month in six of the last eight months. Foreign orders are stronger month-to-month in August and lower month-to-month in four of the last eight months. Order weakness has spawned serious talk that Germany may slip into what is being called a 'technical recession.'

Germany's manufacturing orders continue to run weak. Overall orders are still declining. Total orders have fallen month-to-month five times in the past eight months. Currently, order weakness concentrates in the domestic sector where orders have fallen sharply in August and are lower month-to-month in six of the last eight months. Foreign orders are stronger month-to-month in August and lower month-to-month in four of the last eight months. Order weakness has spawned serious talk that Germany may slip into what is being called a 'technical recession.'

Technical recession? Is it real?

Since German GDP declined by 0.1% in Q2 (-0.3% annualized), any decline in Q3 (without an upward revision to Q2) will constitute two quarters in a row of declining GDP, which some call a 'technical recession.' This phrase has always puzzled me and also bothered me. Economics is a fairly complicated science with lots of numbers, complex mathematical models and sometimes impenetrable econometrics. Yet, counting to two is construed as 'technical? Actually it is more in keeping with the science and terminology of economics to call such a simple rule 'a rule of thumb' making that a rule-of-thumb recession. It is odd, baffling and just plain wrong to call two quarterly declines in GDP (of any magnitude!) a technical recession. There is nothing technical about it. And such a 'signal' might not even merit being called a recession in a more reasoned analysis. Moreover, in Europe, GDP steady-state growth rates are so low that the potential for quarterly rates of growth to come-in flat has become more likely. So Yes, Germany is at risk to being put into a rule-of thumb recession, but with the first quarter's decline so shallow I would not get too excited about the event.

Recession or not here it comes...

The German economy is still under great deal of pressure and it has been slowing down. Domestic orders fall by 7% over 12 months and then at a stepped up -13.5% pace over six months. But over three months domestic orders are falling at a 9.9% pace, still a rapid decline and worse than the year-over-year pace but not worsening compared to the six-month pace. Moreover, foreign orders, that are lower by 6.4% over 12 months, are now rising over six months as well as over three months, in both cases at nearly a 7% rate of positive growth. And the German economy is very dependent on its foreign orders. So the downward momentum seems to be abating even as it is in train.

How severe will 'IT' be?

Output for Q3 is still poor. Orders still highly favor the notion that the rule-of-thumb recession will emerge. Total orders are falling in the quarter-to date (QTD) at a 6.3% annualized rate. This is the calculation for orders two months into Q3 with the annualized growth properly calibrated over the Q2 average for orders. In the previous quarter, orders fell at a 3.6% annualized pace as foreign orders rose and domestic orders imploded at a 15.2% annual rate. But of course these are orders and orders formally are not part of GDP; orders are an 'indicator.' But we can also look at real sales. Real manufacturing sector sales also are falling QTD and at a rapid 4.2% annualized pace. Manufacturing real sales fell at a 6.3% pace in the previous quarter. So the pace of decline is abating in Q3 compared to Q2, the same trend we see for domestic orders. But foreign order growth is getting worse on a quarterly comparison even as its sequential performance (in the table) shows improved three-month and six-month trends. Clearly, there is a lot of downward momentum, but it is also clear that the degree of momentum is mixed

'Trend' as opposed to a specific quarter's growth

The three-and six-month trends may be the best gauges for how the trends in orders and sales are being affected. But to suss out GDP developments, it is better to look at quarterly data since GDP is a quarterly animal itself. Weighing and balancing all these trends, Q3 seems most likely to print a negative GDP results but the 'recession' if we can call it that does not right now look like it is digging in and deepening. Real sector sales are actually increasing at a 3.8% pace over three months after logging a slightly decelerated decline over six months compared to 12 months. AND then there are those positive gains in foreign orders over three months and six months. The details on real sector sales show the consumer holding up and actually accelerating demand (real sales) for durable goods as that series is still steadily accelerating its growth from 12-month to six-months to three-months – yes positive acceleration in the face of all that other weakness. Consumer nondurable goods weakness has stabilized; after falling by 7% year-on-year, three-month and six-month consumer nondurables sales are steady at about -4.5%. Capital goods sales trends worsened over six months but that weakness has abated over three months as capital goods real sales fall at a very minor -0.4% annual rate over three months compared to -2.0% over six months. Even intermediate goods sales seem to have gone past their peak weakness as sequential growth rates there show improvement from 12-months to six-months to three-months, culminating in a three-month rise.

Recession vs. Stimulus!

The case of the German economy and its potential for recession makes great headlines. And with the ECB pulling hard to right the sinking euro-ship, it is frightening to think that Germany will slip into a recession with the ECB pulling so hard in the other direction. But the truth is different from that tooth-grinding 'fake-news' set up. The truth is that the current quarter could turn up quite weak, much weaker than Q2, but that the previous quarter was more 'flat' than 'down.' Rounding to integers -0.1% rounds to zero, not to -1. Next, the trends clearly are not in a free-fall as they were earlier this year. So while Europe's strongest economy may not look so strong, on closer looks this episode of weakness is looking more like a serious stumble than like a bone-crushing fall. Third, the ECB stimulus plan is still quite new and would not have had any effect on the data that is reported as of August.

Trouble ahead? Yes, but manageable

I am not saying that there are not still serious risks. But the revival in Germany's foreign orders is a notable development. The fact that Germany is running a fiscal surplus and has plenty of room to switch gears and to provide domestic stimulus is very significant even though that potential may not ever be realized. That it is there is a strong reason to believe that the German economy will not suffer a sustained hard fall. And while the U.S.-China trade war is in effect, the fact that Germany's foreign orders already are faring better in this environment is very encouraging.

Manageable...but still trouble...and risky

However, there are still some significant negatives in play. The U.K. Brexit deal is far from arranged and Germany has significant exports to the U.K. that could yet run afoul of a bad Brexit resolution. There is also a brewing U.S.-EU trade spat over airframe subsidies and the U.S. won a ruling in the WTO against Airbus and the EU for its subsidies. In addition, there are significant U.S.-EU trade negotiations still to be conducted. And there is no guarantee that the U.S.-China trade war won't get worse or that the trade slowdown won't have a wider negative impact before it is resolved. All of this causes the German data and trends to be considered more as a sort of wheel within a wheel rather than decisive on their own. There are forces in play that German economics, German fiscal policy, and ECB monetary policy cannot determine or even affect. We do see some of complexities in the trends of the German data themselves which are not wholly pointing in only one direction. It is fitting that when we consider the prospects for the German economy we think of the potential for a rule-of-thumb recession and to bear in mind the proper context for that evaluation. Unless there is another leg down in global growth, German growth trends right now do not seem so damaging; they seem to offer hope even as they seem to embrace the reality of a Q3 downturn and a possible recession. Ah, recession…would a recession by any other name stink as badly? As it turns out recessions have a broad spectrum of stink, as I have argued above. This one may just turn out to be only slightly offending.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief