Global| Dec 22 2008

Global| Dec 22 2008Orders Make Record Drop in Euro During October

Summary

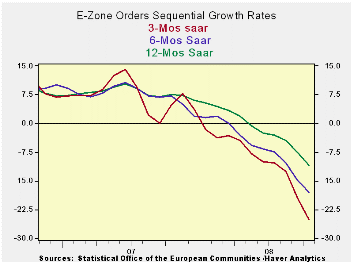

A rapid deceleration…The sharp drop in the growth rate for orders in the current quarter is telling of the rapidity with which this slowdown has struck Europe. Orders in the fourth quarter are falling at annual rates of 50% in [...]

A rapid deceleration…The sharp drop in the growth rate for

orders in the current quarter is telling of the rapidity with which

this slowdown has struck Europe. Orders in the fourth quarter are

falling at annual rates of 50% in Germany, 57% in France, 37% in Italy

and nearly 70% in the United Kingdom. This obvious bespeaks of a sharp

slowing for growth in 2008-Q4.

Severe real sector hit… While the headlines have focused on

the financial sector and banking problems and, although German consumer

sentiment has been supported, the hit to EMU MFG has been severe. Both

the EMU MFG and Services PMIs have taken sharp drops. These barometers

precede the availability of authentic activity measures. The purchaser

type surveys are merely ‘indicators’ While variables such as industrial

output and retail sales are the actual results.

Orders are an actual forward-looking series… The orders series

is also an actual result and not simply an ‘indicator’. Orders, while

not actual activity are true figures corresponding to activity that

been contracted ahead. The orders data are available for October but

PMI data for December already are in hand –and they continue to be weak.

The recognition lag... It has taken some time but Germany

seems to have come around to the idea of more stimulus. The drop in the

HICP for the Zone (bringing the Yr/Yr headline pace to 2.1%) may also

free up the ECB to become less tentative. Both orders and sales are all

falling and orders are falling with uniform and shocking weakness

across EMU. The dramatic policy moves and in the US have been rekindles

euro FX strength. Is that a good sign or a signal how far behind Europe

is in adopting needed stimulus? There should be no question about the

severity of the weakness in Europe. It’s not just a banking problem.

| E-zone and UK Industrial Orders & Sales Trends | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Saar except m/m | % m/m | Oct 08 |

Oct 08 |

Oct 08 |

Oct 07 |

Oct 06 |

Qtr-2 Date |

||

| Ezone Detail | Oct 08 |

Sep 08 |

Aug 08 |

3-Mo | 6-mo | 12-mo | 12-mo | 12-mo | Saar |

| MFG Sales | -1.3% | -1.6% | -0.8% | -13.7% | -6.7% | -0.7% | 5.5% | 8.0% | -14.6% |

| Consumer | -0.2% | -0.3% | -0.2% | -2.8% | -2.2% | -1.1% | 5.5% | 8.0% | -2.9% |

| Capital | -0.4% | -0.5% | -0.4% | -5.0% | -4.1% | -0.5% | 3.9% | 4.6% | -4.9% |

| Intermediate | #N/A | -5.6% | -0.3% | #N/A | #N/A | #N/A | 7.3% | 8.0% | -15.6% |

| MFG Orders | |||||||||

| Total Orders | -4.7% | -5.4% | -1.6% | -38.1% | -26.1% | -14.4% | 8.8% | 10.9% | -42.1% |

| Countries: | Oct 08 |

Sep 08 |

Aug 08 |

3-Mo | 6-mo | 12-mo | 12-mo | 12-mo | Qtr-2 Date |

| Germany: | -6.8% | -8.0% | 3.1% | -38.9% | -29.1% | -16.4% | 10.8% | 9.1% | -50.2% |

| France: | -11.3% | 0.4% | -7.7% | -54.3% | -37.7% | -18.3% | 4.7% | 10.9% | -58.0% |

| Italy | -5.4% | -2.5% | -1.9% | -33.1% | -18.6% | -10.1% | 6.1% | 12.7% | -37.8% |

| UK(EU) | -28.3% | 28.7% | -8.6% | -49.5% | -42.4% | -14.2% | 5.0% | 9.2% | -69.9% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief