Global| Sep 17 2008

Global| Sep 17 2008Orders Just Fall Off the Table in the UK

Summary

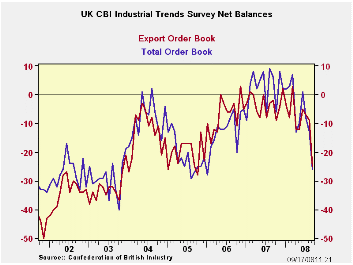

Orders overall and export orders have fallen off very sharply from August to September. The decline of 16 points in month-to-month export orders in September is a record going back to 1988. This drop occurs in the face of a weakening [...]

Orders overall and export orders have fallen off very sharply from August to September. The decline of 16 points in month-to-month export orders in September is a record going back to 1988. This drop occurs in the face of a weakening Sterling which implies an improvement in UK competitiveness. Total orders fell by 13 points month-to-month and that is the fourth largest m/m drop since the late 1980s. All of the outsized drops in total orders have come since October 2006.

While changes in orders on the month demonstrate a very severe drop, current readings on the diffusion levels remain higher, in the 55th percentile for total orders and the 72nd percentile for export orders. – lower but not as draconian as the monthly changes. Still both overall and total orders are deep net negative readings. The volume for output in the look ahead survey is at a new low. Prices expected in the next four months are still at all time highs: 100% of their range. The NTC survey available through August shows MFG is low in its range, in the bottom 15 percent. .

The UK economy looks extremely weak. Current levels in the CBI Industry sector are not quite as severely weak as for CBI orders but the pace of decline is something to have some real worries over and the outlook is as bad as it ever has been.

| UK Industrial Volume Data CBI Survey | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| Reported: | Sep 08 |

Aug 08 |

Jul 08 |

Jun 08 |

12MO Avg | Pcntle | Max | Min | Range |

| Total Orders | -26 | -13 | -8 | 1 | -2 | 55% | 9 | -40 | 49 |

| Export Orders | -25 | -9 | -7 | -5 | -6 | 72% | 3 | -40 | 43 |

| Stocks: Fin Goods | 21 | 18 | 13 | 8 | 13 | 80% | 23 | -2 | 25 |

| Looking ahead | |||||||||

| Output Volume: Next 3 Months | 11 | -13 | -7 | 2 | 4 | 0% | 28 | -13 | 41 |

| Average Prices for Next 3 Months | 31 | 34 | 28 | 30 | 24 | 100% | 34 | -20 | 54 |

| From end 2000 | |||||||||

| Compare to CIPS MFG | |||||||||

| Aug 08 |

Jul 08 |

Jun 08 |

May 08 |

12MO Avg | Pcntle | Max | Min | Range | |

| UK MFG | 45.93 | 44.13 | 45.88 | 49.46 | 50.21 | 15% | 56.32 | 44.13 | 12 |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief