Global| May 12 2020

Global| May 12 2020OECD LEIs 'Unprecedented Collapse'

Summary

The OECD's own headline on this report flags the LEIs as showing an 'unprecedented collapse,' I have simply gone with their lede. Weakness globally stems from the nearly synchronous spread of the Coronavirus and the impact of policies [...]

The OECD's own headline on this report flags the LEIs as showing an 'unprecedented collapse,' I have simply gone with their lede.

The OECD's own headline on this report flags the LEIs as showing an 'unprecedented collapse,' I have simply gone with their lede.

Weakness globally stems from the nearly synchronous spread of the Coronavirus and the impact of policies being pursued to continue and defeat it. As everyone knows by now the virus, started in Wuhan China and spread globally. It infected local pollution around the world with somewhat different timing and countries have taken steps but not all the same steps with the same timeliness to defeat the spread of the virus. However, statistics show that the impact is now more or less synchronous with a very few exceptions.

The LEIs in abnormal times...

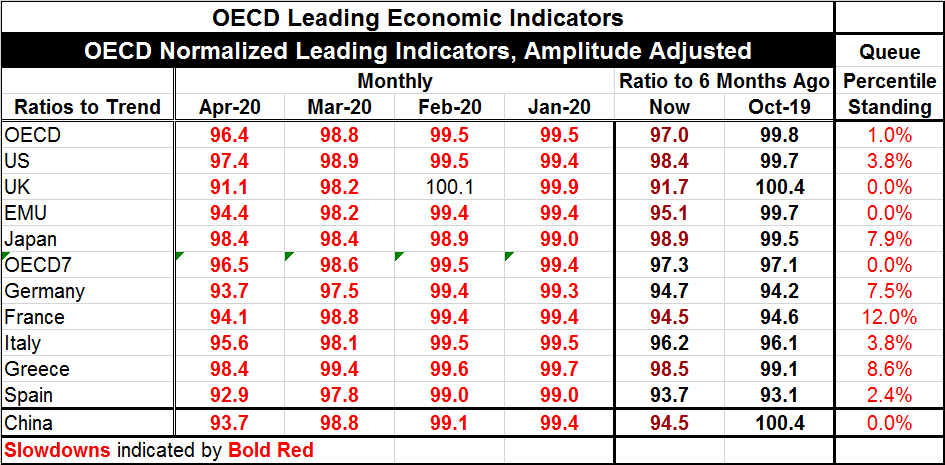

In the table, all recent LEI readings are below 100 indicating lower than normal growth. All show declines relative to six-months ago which is one of the OECD's preferred metrics for analyzing the LEIs. The composite leading indicators of the OECD tend to show turning points about six-months to nine-months before economic activity changes…under normal circumstances.

However, let me reproduce this note from the OECD about its own metrics this month:

"Note: Composite leading indicators (CLIs) are designed to anticipate turning points in economic activity relative to trend six to nine months ahead. However, care needs to be taken in interpreting CLIs in the current crisis as governments attempt to tackle the COVID 19 pandemic. Uncertainty surrounding the duration of lockdown measures has complicated the ability of CLIs to provide those forward looking signals. For those economies still in lockdown and with uncertainty about the timing or nature of easing measures, current estimates of the CLI should be viewed as coincident rather than leading. As always, the magnitude of the CLI decline should not be regarded as a measure of the degree of contraction in economic activity, but rather as an indication of the strength of the signal" (Source here).

Clearly, the OECD recognizes that these times are special and that the usual lagged response is not likely to hold because of the special role of government policies in depressing economic activity in an attempt to quash the spread of the virus. Still, the metrics have value assessing the depth of the impact across countries even if the LEIs are not functioning as an early warning system anymore.

Absolute weakness

The far-right hand column of the table below shows how weak these readings are. That column ranks the values for April in their respective queues of observations back to January 1996, a period of nearly 25 years. On this timeline, we find the United Kingdom, EMU and China on their all-time lows. France is the relative strongest country in this table with a bottom 12th percentile reading. Except for France, all readings are below their 10th percentile. Of the 11 entries in the table, 7 are below their 5th percentile. Obviously, weakness - and in all likelihood recession - is being signaled up and down the line.

Developing economies

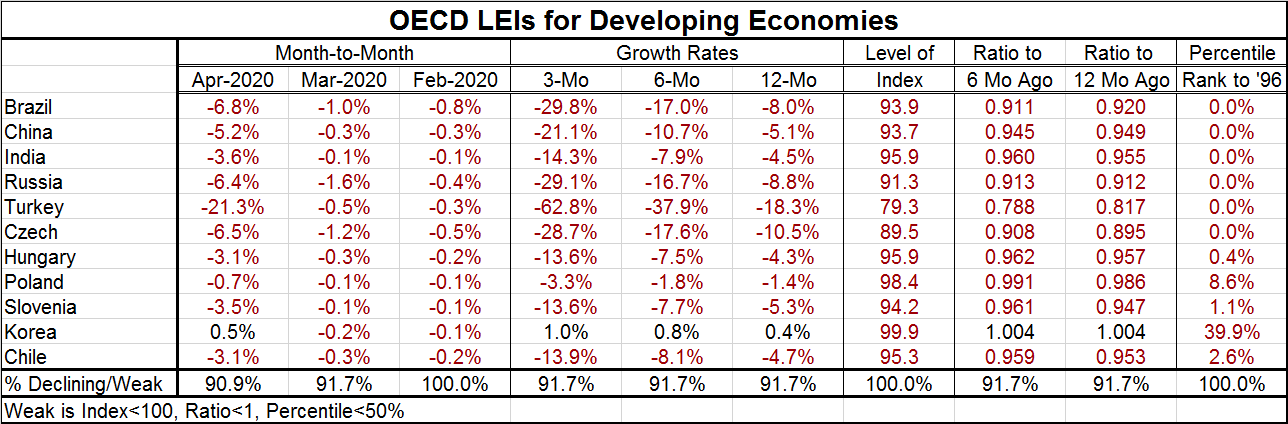

Separately, we look at the readings for developing economies (China appears in both tables because of its 'dual' nature). Among this group, only South Korea shows sporadic positive readings. However, all index levels are below 100 across the board (South Korea barely fits this at a 99.9 reading). South Korea has a 39.9 percentile standing, the strongest standing in either table. Apart from it, however, most entries in this table show all-time lows have been reached or at least that a reading below their bottom five-percentile. Developing economics are getting hit hard by the virus, by the impact on world trade, and by the collapse of global commodity prices.

The depth and breadth of the impact from this virus and the response to it is unprecedented. Unlike past episodes of weakness, one of the main actions governments can do to stimulate growth is simply to set their local economics free from lockdowns and other restrictions. But even as these policies are in place, governments have engaged in a host of added policies to support consumer and or business incomes. Governments, in fact, do not simply remove restrictions to stimulate growth because the restraint of growth is holding back the virus and that is the ultimate paradox here.

Still, it is quite clear that shutting down an economy is much easier than caring for everyone whose business gets shut down or job eliminated. People everywhere fall through the cracks in the support policy. Dedicating healthcare systems to one cause deprives others in need of healthcare of needed services to the detriment of their heath. Children are missing their vaccinations. People are missing their regular trips to their physicians and more. Lockdowns cause problems ranging from mere 'cabin fever' to increased spousal abuse, suicide, divorce, alcoholism and more. Even as governments aim to replace lost salaries, that action weighs on national resources even as many people's own financial standings are eroded. There are few if any winners from this process. Businesses will fail. Students are having their academic careers interrupted. And many different sorts of prices are being paid to have this lockdown. The lockdown does not simply or even clearly 'save lives.'

No vaccine

There is no vaccine for the virus and yet a global effort has been mounted to find one. There is no guarantee of success. If one is found, it will take a long time to make enough to inoculate all those who will need it. The current lockdown/shelter in place/restriction/social distancing approaches all are stop-gap meant to slow the spread of the disease and reduce deaths.

Not all action leads to solution

But none of those actions are solutions. And those actions go hand-in-hand with reduced economic growth and growing socio-economic problems especially many of a financial nature. At some point, a policy other than kicking the can down the road endlessly at great cost will be needed.

The road untaken

Some scientists have urged waiting and sheltering until there is a vaccine. I can't imagine that there is really much science behind such a view since many problems are created by such a long wait as well as many of a financial nature that will multiply. In my view, waiting for something to be invented to save you is more the stuff of science fiction than of science. What real 'science' we have at our fingertips is to let populations gain herd immunity. This refers to getting infection throughout about 60% of the population according to epidemiologists. Once that level of infection and spread of antibodies has been reached, the risk from a second wave of infections is blunted. This is a path to solution unlike endless waiting and social distancing – a policy that also results in deaths. But, as yet, only Sweden is seen to be putting its toe in those waters.

When global policy shift to pursue solution?

While many have died as a result of the infection from this virus, evidence increasingly shows that people with existing underlying medical issues are the most at risk. There is an avenue to growth for countries that are able to shelter their at-risk populations and relay on their most-healthy population to restart growth. So far, the idea of letting the disease spread a little more organically among those who are most healthy while more strictly sheltering the at-risk has not been policy. However, relatively clear data from the NYC experience suggests strongly that such a path could be very fruitful and could spread infection with the result of very few deaths. This approach has not found favor. And so far, healthcare officials continue to proceed as though there is only one population when we know we have at least two populations, one of which is at risk and the other that is quite resilient. That fact could be used to restart growth even on a global scale.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief