Global| Jun 08 2016

Global| Jun 08 2016OECD LEIs Still Struggle

Summary

The OECD's own results for this month's report are, in my opinion, way too weak to show, or do much more than very vaguely hint, at stabilization in the U.S., China or elsewhere. But that is the headline that news services are picking [...]

The OECD's own results for this month's report are, in my opinion, way too weak to show, or do much more than very vaguely hint, at stabilization in the U.S., China or elsewhere. But that is the headline that news services are picking up and one that the OECD has in some fashion put on its charts. So let's address those circumstances directly.

The OECD's own results for this month's report are, in my opinion, way too weak to show, or do much more than very vaguely hint, at stabilization in the U.S., China or elsewhere. But that is the headline that news services are picking up and one that the OECD has in some fashion put on its charts. So let's address those circumstances directly.

What the OECD actually said

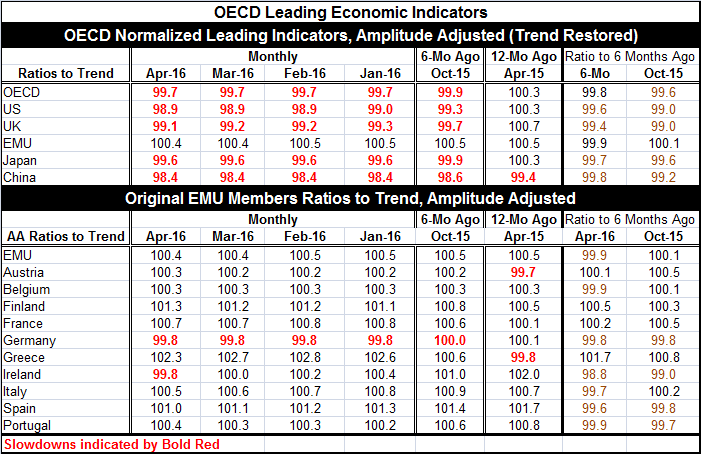

What the OECD said about China is that there is `stable growth momentum' which sounds good until you look at the chart (mine or the OECD's) and notice that China's index is still SINKING at a stable pace. That is not good. The table below shows that China's LEI is lower on balance over six months as well as being lower over six months as of six months ago. China was also producing readings below 100, six months ago as well as 12 months ago. The benchmark of 100 is a period average meant to flag neutrality. China remains below neutrality and is sinking further below it.

What U.S. `stability' means

As for the U.S., the `stability' means that the U.S. index is stuck at 98.9 for three months in a row. The U.S. index is lower on balance over six months and over 12 months and it is stuck at a subpar pace (below 100). If we take the U.S. index and rank it in its queue of values since 1991, we find the U.S. gauge has been lower only 17.9% of the time. This would not be a good place for the U.S. economy to `stabilize.' By comparison, China, on a timeline back to 1992 when its data begin, has been weaker only 13.2% of the time - and it is still slowing with `stable momentum.'

EMU: The best of the lot but showing erosion

Only the EMU among the grouping of countries and regions in the table has consistent readings above 100. And the EMU shows some crack in this stability as it notched lower in March and has stayed at the lower reading in April. The EMU gauge is net lower over six months but it is level six months ago at the same reading it had 12 months ago with both readings (100.5) above the key metric of 100. The details for the EMU corroborate that this sort of stability is still the common denominator across the euro area with members generally producing a string of readings below 100 as well as net declines over both six-months and 12-months. Of these 11 early EMU members, four show improved conditions over the last six months (Austria, Finland, France and Greece). The rest show six-month erosion but only Germany and Ireland show LEI values below 100 as of April 2016 and only Germany shows a string of such readings. However, Germany also shows net declines over six months and 12 months and is joined in that metric by Ireland, Spain and Portugal. So while the EMU continues to show readings above 100 indicating `better than normal' conditions, there is evidence of erosion at work and more than there is evidence that the EMU is building upon that stability.

Forecast reductions are still in train

In other news overnight, the World Banks has cut its forecast for 2016 again, this time to 2.6% growth from 2.9% growth- a sizeable reduction in the outlook. A Bank of France survey has led the BoF to reduce its expectation for French growth in Q2. China's central bank cut its forecast for Chinese exports this year but held to its projection of 6.8% for GDP growth. The World Bank cuts its own projection for China's GDP growth to 6.7% from the 6.9% growth pace China posted in 2015. Further news on China shows that it is still losing foreign exchange reserves with the dollar value of its reserves lower by $28 billion in May.

Poll-o-nomics

I guess we now also live in the age of Poll-o-nomics since expectations are a central part of economic theory. Today we have a poll telling us that the U.K. is believed to be weak because of fears of Brexit. Another poll suggests that Euroscepticism is in the rise. The Pew poll still shows a razor thin majority of 51% favoring the EU. And most EU members want the U.K. to `stay in.' But with this sort of thin balance, the stakes for Brexit appear to be high. We have every reason to believe that our fear over Brexit is not over Brexit alone but over Brexit as a potential catalyst for other succession votes. And because of that we have every reason to believe that if the U.K. does vote to leave it will not be treated kindly since the EU would not want to send the signal to member countries telling them that they can leave and yet `everything else' will remain the same. Brexit polls are producing all sorts of results. While two internet-based polls earlier showed that the `Out's had surged to the lead, several more conventionally based polls found that the tilt still favors `In.' I doubt that either side in this fight feels `comfortable' with its polling margin. Markets will hang on poll results in the coming weeks until the vote is in.

South China Sea/China Talks

Other potentially significant news on the geopolitical front today found China chiding the Philippines arguing that there is a mechanism for the two countries to discuss their differences. I wonder it if this is a way for China to be, or to appear to be, open minded on the South China Sea issue even as it prepares to reject the decision of the Permanent Court of Arbitration in The Hague. However, U.S. talks with China appear to have ended in disappointment with little progress reported on their bilateral issues. Talking with China does not seem to have been fruitful and it appears to have become less impactful over the years.

Summing up

On balance, despite a somewhat upbeat assessment from the OECD, there is still a lot of weakness and an environment in which forecasts of all sorts are being cut. This hardly seems like the stuff of stability. As always there are some cross currents as the U.K. reported solid gains in IP contrasted by Japan's economy watchers index (service sector gauge) hitting an 18-month low. Growth remains sluggish with many disappointing elements and there is no real evidence that there is any new break out in any direction, despite the way the OECD LEI data have been reported today. Decay still seems to be the order of the day.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief