Global| Apr 08 2014

Global| Apr 08 2014OECD LEIs Slow

Summary

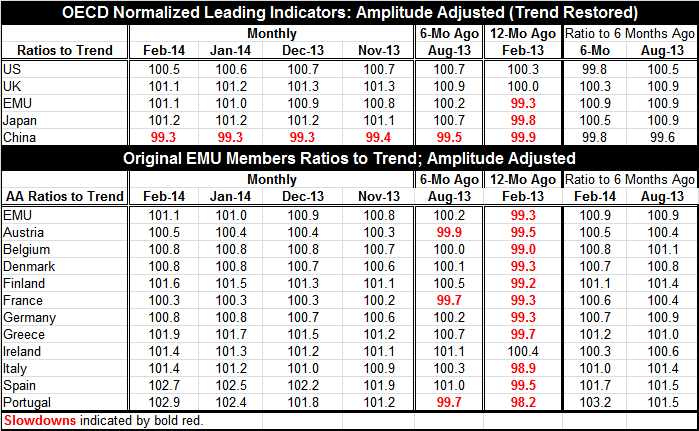

The amplitude adjusted index for the entire OECD area was flat for the third consecutive month. But flat at a level above 100; growth goes on. The US and UK indices each ticked down on the month. China and Japan were flat. The EMU [...]

The amplitude adjusted index for the entire OECD area was flat for the third consecutive month. But flat at a level above 100; growth goes on. The US and UK indices each ticked down on the month. China and Japan were flat. The EMU index ticked higher.

The amplitude adjusted index for the entire OECD area was flat for the third consecutive month. But flat at a level above 100; growth goes on. The US and UK indices each ticked down on the month. China and Japan were flat. The EMU index ticked higher.

None of this looks like the period of enhanced growth that the US and Europe have been expecting is about to unfold.

Compared to six months ago, the US and China are lower while the EMU, the UK and Japan are higher. Over the previous six-month period (ended August 2013), only China is lower. China has persistent weakness problems whereas among the other nations and regions, the US, the UK, Japan and EMU, seeing the indicators weaken is a more recent development.

Among the oldest-standing EMU members, all except Ireland were below the 100 level in February of one year ago. In February 2014, they all are above 100. This signals growth. Over six months and over the previous six months to that, all country indices are higher.

But several EMU nations are now stalled. From January to February, the indices did not change for Belgium, Denmark, France and Germany. There were one-tick increases for Finland, Austria and Ireland. Only Portugal, with a gain from 102.4 to 102.9, had a month-to-month pick up of more than two-tenths of a point. Portugal, Spain and Greece make the three largest gains on the month as the Mediterranean countries play catchup. Over three months, these same three countries lead the rebound.

On balance, the OECD leading indicators are not on board with the notion of a European or US acceleration. They are consistent with continuing growth. The data here are current only through February, but recent US data from March have not showed that much improvement from February. There does not seem to be much of a winter-lull effect in the US data.

The OECD indicators point to weakening growth in major emerging economies and continuing growth in the US and for Europe. Despite of much pick up this month, the OECD looks for a positive change in momentum as Europe has raised its indices from lower values over the last six to 12 months. The OECD likes to focus on changes over six months for their predictive values. On this basis, Europe looks a little stronger, but not the US.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief