Global| Oct 08 2014

Global| Oct 08 2014OECD LEIs Show Weakness

Summary

The OECD leading economic indicator for the entire OECD area in August is unchanged from July and June at a reading of 100.4. This string of readings ticked higher from May when the level was 100.5. The U.S. has an unchanged reading [...]

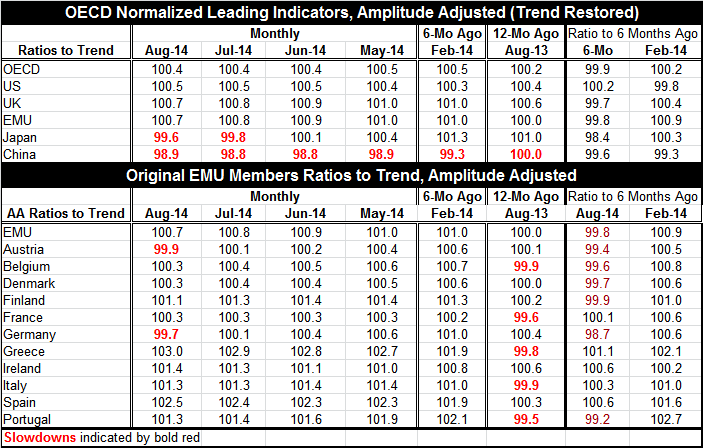

The OECD leading economic indicator for the entire OECD area in August is unchanged from July and June at a reading of 100.4. This string of readings ticked higher from May when the level was 100.5. The U.S. has an unchanged reading in August from July at 100.5. The U.K. has a slightly weaker reading in August at 100.7 compared to 100.8 July. The European Monetary Union reading has slipped to 100.7 from 100.8. It has been slipping for the last four months. Japan's reading at 99.6 is consistent with a slight slowdown; its August reading is down by 2 tenths from July's 99.8 reading. China continues to cruise at values below 100, consistent with a mild slowdown. However, in August, China's reading picked up slightly to 98.9 from 98.8.

The OECD leading economic indicator for the entire OECD area in August is unchanged from July and June at a reading of 100.4. This string of readings ticked higher from May when the level was 100.5. The U.S. has an unchanged reading in August from July at 100.5. The U.K. has a slightly weaker reading in August at 100.7 compared to 100.8 July. The European Monetary Union reading has slipped to 100.7 from 100.8. It has been slipping for the last four months. Japan's reading at 99.6 is consistent with a slight slowdown; its August reading is down by 2 tenths from July's 99.8 reading. China continues to cruise at values below 100, consistent with a mild slowdown. However, in August, China's reading picked up slightly to 98.9 from 98.8.

The OECD readings show very little change in these latest aggregate regional and country readings. However, while the overall OECD reading is flat, we see a tendency for some weaknesses in the U.K., the EMU and Japan. China managed to edge up in August, but its gauge continues to be weak. On balance, the message of the latest OECD indicators is not that everything is fine because the overall index is steady but that there is a clustering of weakness in some key areas in the report's details.

Turning to the table of early EMU members, we see that only two have index readings below 100 in August. Those two members are Austria and Germany. Both of them have slipped month-to-month and both of them are lower compared to six months ago. In fact, the overall EMU measure is lower compared to six months ago as are readings for six of the 11 countries in the table. In addition to Austria and Germany, Belgium is lower compared to six months ago, Denmark is lower compared to six months ago, and Finland is lower compared to six months ago as is Portugal.

If evaluating the OECD indices by their position in their historic queue from 1990 onward, we find the EMU measure is only in its 68th queue percentile. Germany is the relative weakest country in the union with its gauge in its 35th percentile. Austria is the next weakest in its 44th percentile. The countries that are strong in historic comparison are Spain: 99th percentile, Greece: 98th percentile, Italy: 82nd percentile, and Ireland: 81st percentile. These percentiles refer to the relative standing of the OECD LEI compared to historic norms. What these values tell us is that the former beleaguered EMU members are better posed for growth now than they have been on average (as well as for most of the time!) during their EMU membership. However, the weakness in the traditional leaders is still a significant threat as Germany is the largest EMU economy.

The OECD prefers to look at its gauges and their changes over six months. Over this period, we see a broad array of EMU member countries with values that have slipped. The countries of strength on this time horizon are France, Greece, Ireland, Italy and Spain- largely a group of countries that have undergone the most duress in the cycle. None of these countries is performing well enough to think that it will take over leadership in the EMU. Instead, countries that have provided leadership in the EMU are now starting to weaken. This is not a changing of the guard for European leadership but evidence of weakness being transmitted to the countries that used to be strong. It represents a challenge to growth.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief