Global| Jul 08 2013

Global| Jul 08 2013OECD LEIs Show Some Comfort

Summary

According to the OECD's trend-restored and amplitude-adjusted indices, Japan and the US point to growth that is firming. In the euro-Area, European growth is gaining momentum. Italy's OECD metric shows positive momentum despite [...]

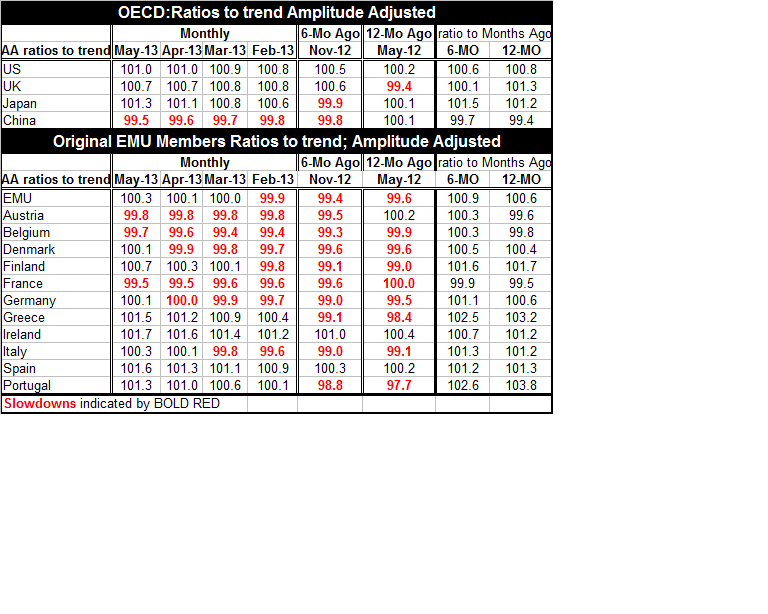

According to the OECD's trend-restored and amplitude-adjusted indices, Japan and the US point to growth that is firming. In the euro-Area, European growth is gaining momentum. Italy's OECD metric shows positive momentum despite recently-aired concerns about Italian growth prospects on the part of the IMF. France points to stable momentum in the OED framework. There, the BoF business survey just today reported a more upbeat assessment, at least partly on the back of improved demand overseas.

According to the OECD's trend-restored and amplitude-adjusted indices, Japan and the US point to growth that is firming. In the euro-Area, European growth is gaining momentum. Italy's OECD metric shows positive momentum despite recently-aired concerns about Italian growth prospects on the part of the IMF. France points to stable momentum in the OED framework. There, the BoF business survey just today reported a more upbeat assessment, at least partly on the back of improved demand overseas.

Businessmen were confronting French President Hollande today accusing the government of over-taxing business and of unstable economic policies. Business leaders are urging Hollande to cut spending and to adopt what are more conservative but unpopular fiscal measures. For now, on current policy the OECD indicators show the French economy as stable. France has for the most part raised taxes on high income earners to try to avoid service cuts and the yoke of austerity. That has succeeded in keeping growth somewhat more stable but France's current budget situation is a mess, as a result, as business leaders point out. Their discourse illuminates the shortcomings of the LEI signal. Sometimes a country keeps growth trends up by running up a bill on the future.

In the OECD framework, both Russia and Brazil are losing momentum. The Asean business cycle indicators are show resilient growth despite concerns in the markets about China. The OECD metrics see China as posting growth close to trend rates, just as it does for the UK and for Canada.

The table shows index slippage in May for original e-Zone members Austria, Belgium and France. Only France shows net slippage on this measure over six-months on the amplitude-adjusted basis. Trend-restored indices show steadier growth in France. Greece and Spain are experiencing some of the strongest upward movements in their amplitude-adjusted metrics this month. Revival of some of the peripheral countries as the core EMU nations have struggled is an ongoing theme.

The OECD framework does not exhibit a robust showing. There a little bit of improved momentum and lot of stability or worse. There are no signs of any countries with strong-break-out growth. In addition there are still countries trying to work their way out of some real difficulties. All the OECD indicators do this month is to point to some stability as long as things stay as they are. But the prospects for that to happen are dim.

Data on the day show investor confidence weakening in EMU. The German trade surplus is off sharply and while German IP fell in May it still has some very strong-to-solid growth in train. But industrial output in May was lower in Sweden and in the Czech Republic as well as in Bulgaria and Turkey. There is some IP revival in Switzerland in Q2 and then there is the positive news of that upbeat Bank of France business survey.

Asia remains one of the biggest question marks with growth in China having cooled this year and with China's financial sector difficulties dogging the outlook. Japan, while benefitting from its QE program and a weaker yen, is seeing its economy-watchers index fall for the third month in a row.

It's these sorts of trends and observations that make the OECD results less than encouraging. What's percolating in the global economy's pipeline is not likely to give a boost to growth anytime soon. It might make the global economy stronger eventually- but 'eventually' comes later, not 'sooner.' The OECD indices do not address those sorts of things.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief