Global| Feb 08 2017

Global| Feb 08 2017OECD LEIs Show Continuing Modest Expansion

Summary

The OECD overall gauge shows continued growth as the comprehensive index rises to a rounded up value of 100 in December from 99.9 in November and continues its one-tick per month advance that has been in play for the last three [...]

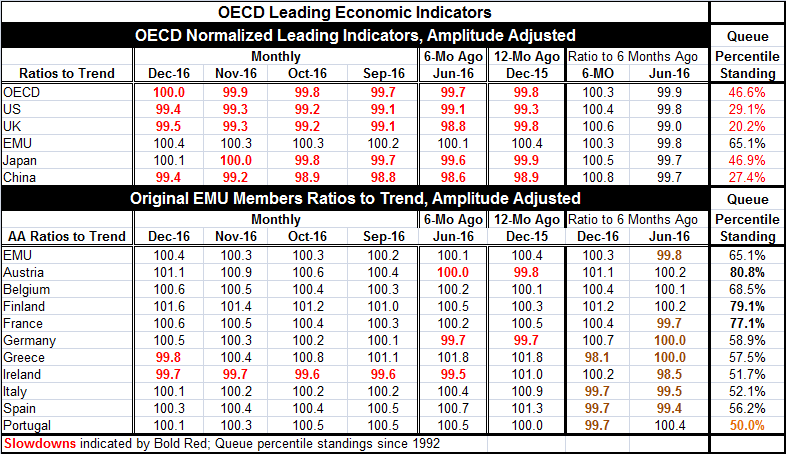

The OECD overall gauge shows continued growth as the comprehensive index rises to a rounded up value of 100 in December from 99.9 in November and continues its one-tick per month advance that has been in play for the last three months. On the OECD gauges, the LEI index value of 100 is the demarcation line between normal and subpar growth. Subpar assessments are still in place for the U.K., the U.S., and China. Japan elevates above that morass of stagnation with a 100.1 reading while the EMU at 100.4 has slightly more breathing room. While the picture is one that signals growth, there are no modifiers of reassurance here: growth is not robust growth, it is modest growth and it is barely an improved reading after a long string of ongoing disappointing readings.

The OECD overall gauge shows continued growth as the comprehensive index rises to a rounded up value of 100 in December from 99.9 in November and continues its one-tick per month advance that has been in play for the last three months. On the OECD gauges, the LEI index value of 100 is the demarcation line between normal and subpar growth. Subpar assessments are still in place for the U.K., the U.S., and China. Japan elevates above that morass of stagnation with a 100.1 reading while the EMU at 100.4 has slightly more breathing room. While the picture is one that signals growth, there are no modifiers of reassurance here: growth is not robust growth, it is modest growth and it is barely an improved reading after a long string of ongoing disappointing readings.

What to look for

The OECD prefers to look at six-month changes in its indicators. Over six-month changes in the indicators from the countries/areas listed at the top of the table are showing gains. So the levels of the indices signal subpar growth, but the changes in the OECD LEIs signal that there is some acceleration in train. Still, that signal is quite muted as the six-month ratio is higher by 0.8% in China, by 0.6% in the U.K., by 0.5% in Japan, by 0.4% in the U.S., and by 0.3% in the EMU as well as for the OECD overall. None of these are rollicking signals of substantial acceleration.

Moreover, the LEIs recalculated over their previous six months (June 2016 to December 2015) all show lower ratios. Thus, the step up to an accelerating phase is still nascent and not yet a solid foundation to build on and to take for granted

LEI index levels

I also evaluate the rankings of the levels of the OECD LEIs from 1992-to-date. On that timeline, only the EMU has an LEI value above its median reading. Japan as a 46.9 percentile ranking, all of the OECD region has a 46.6 percentile ranking, the U.S. has a 29.1 percentile ranking, China has a 27.4 percentile ranking, and the U.K. has a 20.2 percentile ranking. These readings underscore how weak the OECD gauges really are. They may be signaling growth, there may be some modest acceleration in train, but compared to past performance, nearly all these readings are lacking and badly lacking. They are not close to normalcy let alone on a clear path to normalcy. Growth still cannot said to have been solidly restored.

EMU

The EMU is an exception and is much more solid overall. The EMU has the only country/regional standing above its 50th percentile and in fact its standing at its 65th percentile and is nearly 20 percentile points ahead of the next best country. Within the EMU among its original members, the weakest by percentile standing is Portugal, whose LEI is on its 50th percentile which is its median ranging back to 1992. Ireland has a 51st percentile standing and Italy is at a 52nd standing. After those, the standings jump to 56th, 57th and 58th percentiles for Spain, Greece, and Germany, respectively. Belgium logs a reading at its 68th percentile with France at its 77th percentile, Finland at its 79th percentile and Austria at its 80th percentile with the strongest relative reading for this group.

Within the EMU, only Greece and Ireland have LEI readings below the 100 mark signaling worse than normal growth. To assess acceleration, we look at changes over six months; only four countries are weaker on balance: Greece, Italy, Spain, and Portugal. Despite everything that has been done, the Mediterranean counties are still lagging. Italy and Spain also show deceleration over the previous six months while Greece is unchanged over the previous six months. Portugal logs some improvement over the previous six months, but then that turns to deceleration again.

Summing up

On balance, the OECD amplitude adjusted leading indicators are showing growth and producing metrics that are not straying very far from their historic averages or medians. While that is not terrible news, it is not great news either and certainly does not represent the notion of some expedited pick up after a long period of underperformance. Growth shows no signs of making up for lost time. And since growth gains continue to be so hard fought even in the presence of historically very low interest rates globally, it raises the question of what happens when central banks pull away 'the prop' of lower rates. The U.S. is in the process of finding out. Mario Draghi is still resisting normalization in the EMU. Japan is still flat out, trying to generate growth and to boost inflation back to 2%. The U.K. is getting stimulus from a weak sterling and looking for an inflation pulse as a result but still fearing a coming slowdown because of its Brexit-related issues. China is simply showing mixed signs of stagnation amid other signs of some degree of pick up and fighting to reorient its economy. In short, global conditions are not threatening either inflation or a slowdown but do fall short of being reassuring as well.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief