Global| Apr 06 2007

Global| Apr 06 2007OECD LEIs Point to Slowdown/Moderation

Summary

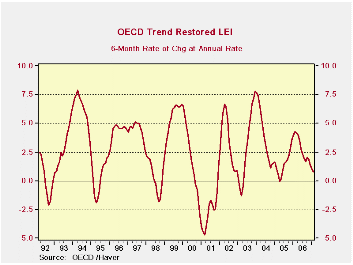

The OECD trend restored leading indicators show a clear deceleration across major areas and countries. Despite this ongoing slowdown Central banks across the region generally are fighting inflation and seem to see it as a still- [...]

| Feb-07 | Jan-07 | Dec-06 | 3-Mo | 6-Mo | 12-Mo | |

| OECD | 0.0% | 0.0% | 0.0% | -0.3% | 1.0% | 2.0% |

| OECD Major 7 | -0.2% | -0.2% | -0.1% | -1.7% | -0.1% | -0.1% |

| OECD Europe | 0.0% | -0.1% | 0.0% | -0.4% | 0.8% | 3.5% |

| OECD Japan | -0.1% | -0.2% | 0.1% | -0.6% | -1.0% | -3.6% |

| OECD US | -0.3% | -0.1% | -0.1% | -2.2% | -0.1% | -0.7% |

The OECD trend restored leading indicators show a clear deceleration across major areas and countries. Despite this ongoing slowdown Central banks across the region generally are fighting inflation and seem to see it as a still-significant risk. Yet, the slowdown is pervasive. Even so, the OECD is only calling it a moderation and nothing more dramatic.

The decline in the overall indicator is clear and it is also clear that it has not yet weakened enough for the region to worry about recession.

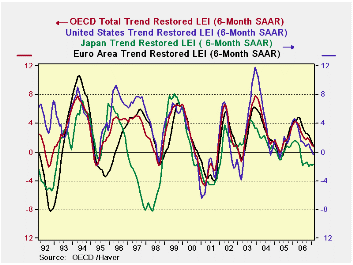

The chart below shows a number of regions plotted together. And it is also clear that there is NO EVIDENCE that the rest of the OECD area has decoupled from the US at all. Besides that, Japan seems especially weak on this score.

While there has been some commentary that the rest of the world has more independent growth and could weather a US slowdown, the chart above shows NO evidence of a break in the link with the US on the LEI front using the OECD measures. In an earlier report we had showed how manufacturing in the US and in Europe remains tightly linked, at least statistically.

Since trade drives a lot of growth we should be wary of seeing new broken linkages. Even China which many see as a major ‘independent force’ also derives a lot of its growth from trade and since all regions send a large amount of exports to the US we have ample reason to doubt that the rest of the world could weather a slowdown in the US.

Central banks must continue to fight inflation since, should it get away from them, bad things would surely happen. The slowdown in growth across the OECD area makes policymaking by the central banks more difficult but it should not deter them from their true goal.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief