Global| May 11 2021

Global| May 11 2021OECD LEIs Point the Way Higher

Summary

The OECD leading economic indicators are a set of indicators established to predict the economy's future performance. The OECD prefers the signal of change over six months. The indexes themselves are constructed relative to ‘normalcy' [...]

The OECD leading economic indicators are a set of indicators established to predict the economy's future performance. The OECD prefers the signal of change over six months. The indexes themselves are constructed relative to ‘normalcy' so that index values above 100 represent above normal growth while values below 100 indicate subnormal growth or worse. The signal for the OECD-area in April is that of slightly above normal growth for the second month in a row. It is the first two-month string above 100 since October-November of 2018, a period of about 2.5 years. In addition, the OECD index is higher compared to six-months earlier a signal of likely acceleration and the same metric from six-months ago also signaled acceleration. The OECD-area is in an above normal growth and growth acceleration zone albeit both signals are mild ones.

The OECD leading economic indicators are a set of indicators established to predict the economy's future performance. The OECD prefers the signal of change over six months. The indexes themselves are constructed relative to ‘normalcy' so that index values above 100 represent above normal growth while values below 100 indicate subnormal growth or worse. The signal for the OECD-area in April is that of slightly above normal growth for the second month in a row. It is the first two-month string above 100 since October-November of 2018, a period of about 2.5 years. In addition, the OECD index is higher compared to six-months earlier a signal of likely acceleration and the same metric from six-months ago also signaled acceleration. The OECD-area is in an above normal growth and growth acceleration zone albeit both signals are mild ones.

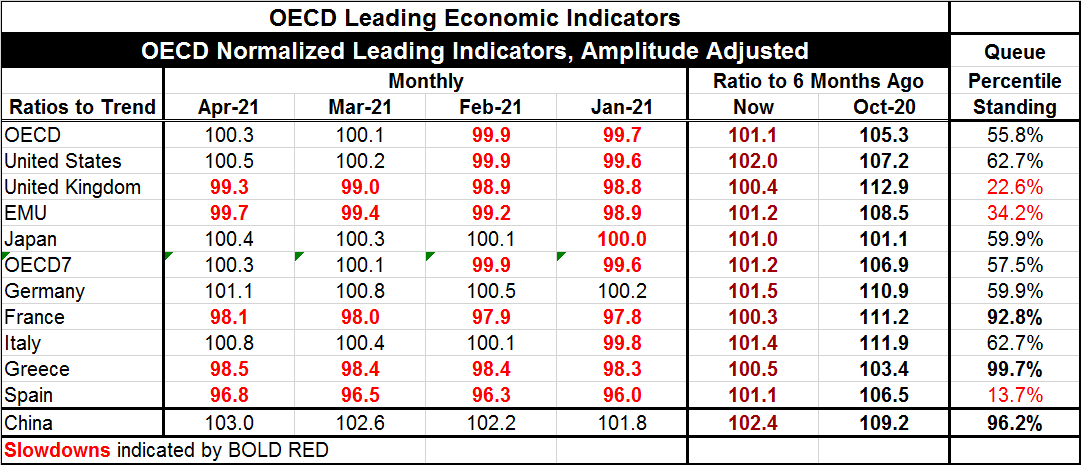

Table OECD Leading Economic Indicator lists a dozen entrees: nine countries and three aggregated measures. Among these twelve, five continue to post LEI values below 100 indicating that they are struggling with below normal growth. The strugglers are Spain (96.8), France (98.1), Greece (98.5), the United Kingdom (99.3), and the EMU (99.7). China at 103 has the strongest reading of all, followed by Germany (101.1), Italy (100.8), and the United States (100.5). Remember these are evaluations relative to each country or region's historic tendencies.

All the economies listed in the table show the ratio of this month's index to that of six-months ago as higher (all are above 100). And the same is true for the same ratio from six-months ago, indicating that expansion has been the order of business for some time now.

Still, there are five of twelve indexes that show sluggish growth; the rankings of the current LEI values in their historic queues of data also produce a number of weak results. Queue percentile standings show below median (below 50%) standings for Spain, the U.K. and the EMU. These three entities also have current index values below 100 indicting below normal growth is in progress. However, two of the three strongest queue standing readings are in Greece and France; yet, both of them have current readings below that level that signals normal growth. That result is a testament to how long Greece and France have been struggling with growth.

In fact, all five entries with current readings below 100 in April have current readings below 100 for at least four months in a row, but the table does not reveal the true extent of lingering weakness in these places. Greece has 12 subnormal monthly readings in a row (readings below 100), Spain has 13, France has 30, the EMU has 21, and the U.K. has 36- three full years, from Brexit to virus.

The other side of this coin finds China with the longest string of above 100 readings by month at six, Germany is second at four, Italy has three, along with Japan; the U.S. has only two. These data tell the clear story of an extended period of weakness stemming from a global trade slowdown that morphed into a pandemic and is now emerging as an early period of recovery.

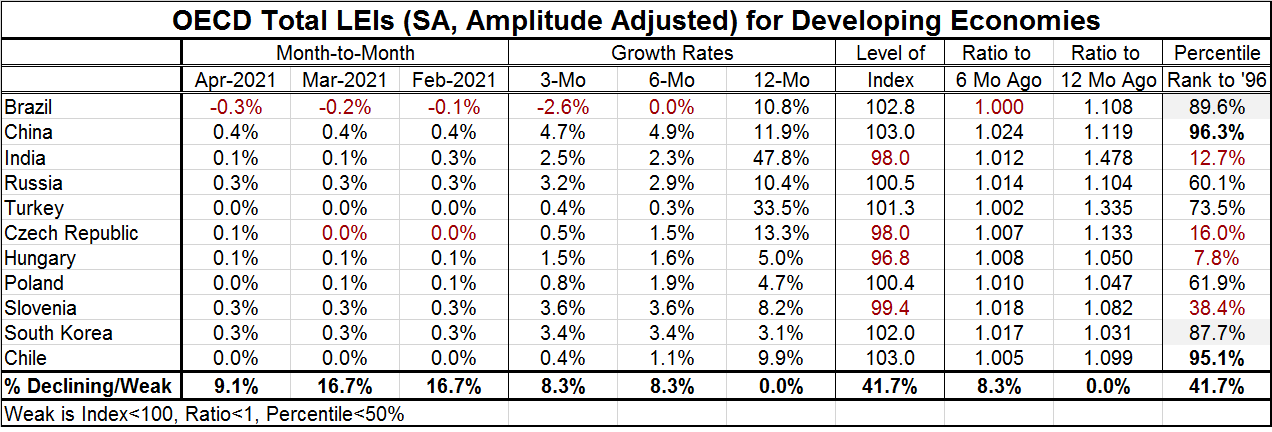

This analysis can be extended to encompass developing economics. There we see of the eleven economics (note that we put China in this matrix as well) no more than one of them weakens month-to-month over the last three months; in April three were flat, in March three were flat and in February three were flat. But in each period seven of eleven improved.

Three- to six- to 12-month growth rates show that growth is expanding in each time frame for each country except in Brazil where growth is flat over six months and backtracking over three months. For now India is still expanding, but it is not clear that that can stand up to its virus problems although Modi has held off on having broad lockdowns that are short-term growth-killers. I'm guessing here, but I think other world leaders have seen how the U.S. lockdowns swamped a strong U.S. economy and cast its head of state out of his job and that is causing some reluctance to shut economies to slow the spread. We have seen this in Brazil and India; in both cases the spread has worsened. Lockdowns are a double-edged sword in developing economies because there are so many multi-generational families that live together and because one of the best ways to spread the virus is to keep people indoors. These realities leave developing economies with a poor set of choices.

Of the eleven countries in the table, only four have LEI metrics below 100 signaling subpar growth these are: Hungary, the Czech Republic, India and Slovenia. Still, all show ratios that are higher compared to six-months ago except Brazil where the showing is essentially flat. All developing economies show rather strong improvements on the six-month ratio to six-months ago for the previous six-month change (from October 2020).

The percentile rankings on the level of the LEIs as of April find very strong standings in China and Chile as well as quite strong readings in Brazil and South Korea. Moderate yet solid readings are logged in Russia, Poland, and Turkey. Sub-median readings persist in Hungary, India, the Czech Republic, and Slovenia.

The average and median standings for the developed countries' LEIs are higher than for the developing group by some 10 to 8 points, depending on the measure. The developing countries are lagging and that is likely to get worse as recovery kicks into gear since developing economy populations are far less vaccinated than those in the developed economies. The virus- at least for now- is much more of a factor in developing economies with India and Brazil as the starkest examples. Today the WHO issued a warning that the variant of the virus circulating in India is a concern (here). They say it spreads more easily and needs more study. WHO says the variant has already spread to 30 countries. WHO apparently also recommends shutting the barn door after the horse escapes. The bottom line is that the global economy is not yet in ‘full recovery mode' and it is not clear when it will get there. The hesitancy is that full recovery mode will continue to be tempered by running the sort of policies that protect against the spread of the virus. As long as the virus is perceived as a threat to spread, it will continue to prompt a healthcare response that will curtail growth in some manner.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief