Global| Jan 12 2015

Global| Jan 12 2015OECD LEIs Move Sideways...for Now

Summary

The main message from the OECD LEIs in November is that not much is changing. The indicators for the OECD region, the U.S., the U.K., the EMU and China are little-changed and clustered around the neutral reading of 100. Japan and [...]

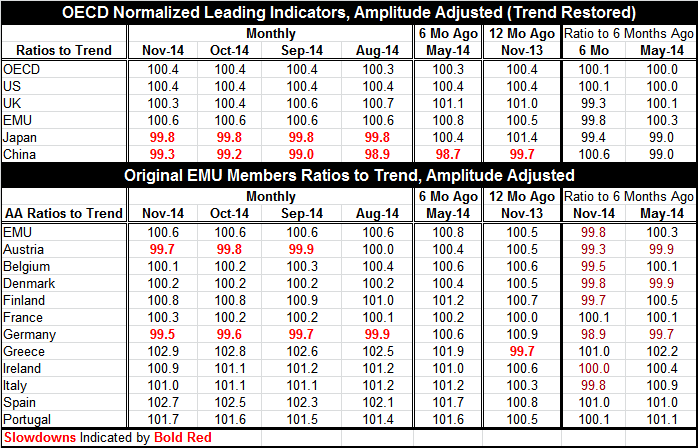

The main message from the OECD LEIs in November is that not much is changing. The indicators for the OECD region, the U.S., the U.K., the EMU and China are little-changed and clustered around the neutral reading of 100. Japan and China are below 100, indicating sluggishness while the EMU region has the highest reading of the group at 100.6. These readings precede a good part of the oil price drop.

The main message from the OECD LEIs in November is that not much is changing. The indicators for the OECD region, the U.S., the U.K., the EMU and China are little-changed and clustered around the neutral reading of 100. Japan and China are below 100, indicating sluggishness while the EMU region has the highest reading of the group at 100.6. These readings precede a good part of the oil price drop.

Compared to six months ago, the OECD area, the U.S. and China are stronger. China, with a topical value below 100, has nonetheless improved the most on this basis. The U.S. and the OECD region are barely improved. The U.K. and the EMU are weaker on a six-month change basis.

Turning to the individual EMU members, we see LEI values below 100 in Austria and Germany. Each of them has a string of values below 100 that has showed some very gradual erosion. However, compared to 12 months ago, only Greece is weaker. But the OECD prefers to look at changes on the six-month horizon. On that basis, the EMU region is weaker and six of 11 members are weaker with Ireland unchanged. Improving over six months are Spain, Greece, France and Portugal. The austerity countries are showing the most improvement while the rest of the euro area largely is eroding.

The message from the OECD data is that conditions are still weak and not changing much but with a bias toward erosion. China has been weak and has implemented special fiscal stimulus. The OECD gauges say China is improving, if still struggling. Japan is struggling and even with massive QE in place has deteriorated on balance over six months. The U.S. is stable, showing a weak degree of expansion. The EMU is slightly stronger than the U.S. on its LEI gauge but is fading.

Since the LEI gauge is for November, we do not have data for the latter period in which oil prices have fallen to their surprising lows. Oil was trading in the mid $70 per barrel range or higher in November. What these indicators do show is how weak the entire OECD region was as of November with little forward momentum. The drop in oil prices, while good for growth in consumer nations, is also destabilizing and having pronounced negative effects in the oil sector as well as across supplier industries ranging into the steel sector. While the focus from the IMF and other institutions, like the Fed, has been on the positive effects of lower prices, there is clearly a good deal of disruption in play and that will be something to keep an eye on in the coming months. Europe, Japan and China seem to be pretty clear winners from lower prices, although high energy taxes in Europe will keep consumers there from feeling the full drop. The U.S. has an energy sector that had been growing by leaps and bounds and had been a driver for the manufacturing sector so the U.S. response will be more ambivalent. The LEI gauge in the months to come will be important to track.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief