Global| Jan 13 2014

Global| Jan 13 2014OECD LEIs Largely Point Higher

Summary

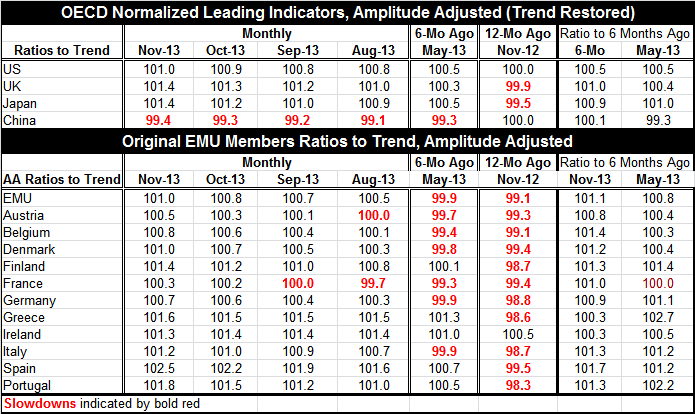

The OECD leading economic indicators continue to show progress. Even in China there is some increase in the indicator for November although China is a case of lingering weakness compared to most of the other countries in the sample. [...]

The OECD leading economic indicators continue to show progress. Even in China there is some increase in the indicator for November although China is a case of lingering weakness compared to most of the other countries in the sample. If we look at the ratios of the current index to six months ago, we find that for all the key countries and regions ratios are higher over six months. For the UK the value 101.0 indicates a 1% increase over six months. Japan is at 100.9; the European Monetary Union is at 101.1; and the US is at 100.5. China is showing bare improvement at 100.1. But in all cases there improvements for the current index compared to the 6 months ago.

The OECD leading economic indicators continue to show progress. Even in China there is some increase in the indicator for November although China is a case of lingering weakness compared to most of the other countries in the sample. If we look at the ratios of the current index to six months ago, we find that for all the key countries and regions ratios are higher over six months. For the UK the value 101.0 indicates a 1% increase over six months. Japan is at 100.9; the European Monetary Union is at 101.1; and the US is at 100.5. China is showing bare improvement at 100.1. But in all cases there improvements for the current index compared to the 6 months ago.

In the far right-hand column of the table, we can compare the ratio to six months ago in the current period versus the same ratio for six months ago. In most cases the ratio of the current index to six months ago is greater than that ratio was when it was taken six months previously, in May. However, Japan shows a slight backtracking; the US shows no change in its momentum on that basis measured in November 2013 or in May 2013.

The message is that the global economy is improving. The OECD leading indicators generally work best when they are used over six-month periods; hence we focus on changes in the indicators over six-month periods. If we look at the original EMU members as well as Greece, we see that over the last four months all of the LEI measures are above 100 except for three instances and only France, in the last four months, has a measure that is below 100. But since then even the French measures are improving. France that has been an outlier showing weakness in many reports, in the OECD framework, is demonstrating overall progress. I don't know if that is affected by the fact that the OECD is headquartered in Paris. OECD forecasts are known to be subject to scrutiny by the home country officials.

Six months ago and 12 months ago, the LEI readings for many of the EMU members were below 100, indicating subpar growth. In fact, 12 months ago all readings were below 100 except for Ireland.

Finland, Germany, Greece, Ireland, and Portugal are the EMU members that have seen their current-to-six-month ratios in November slip to lower levels than where they stood in May. For these members momentum seems to be slipping. It is a surprise to see Germany on the list. In part slippages about who had stronger momentum 12 months ago. 12 months ago Greece had the strongest current-to-six-month ratio of any EMU member in the table; its current reading is now the worst. Portugal also had a strong reading 6 months ago. It was the second-highest of all members in the table; it has slipped but only to the fourth strongest reading on the current horizon. Germany had ranked sixth; its ranking has now slipped to eight among EMU members in terms of its shift in momentum. Germany's ratio had been above the ratio value for the EMU as a whole in May, but in November it has slipped below that mark.

We are concerned with momentum as well as with expansion. The OECD measures show expansion gaining everywhere except China and it shows that momentum is improving across the board without exception over the last six months. However, the pickups are not very strong. As we have seen in the recent December data from the United States, the job market is not building unquestioned momentum. In Europe, the unemployment rate hovers at an all-time high in the Monetary Union. Japan continues to fight deflation with mixed reviews from abroad on its potential for success. The UK economy seems to show more strength and momentum in its usual batch of economic statistics tan what is revealed in the OECD indicators. China, a country that is undergoing substantial shifts as it has to wean itself away from unquestioned reliance on export led growth, is showing the pain of this switch but according to the OECD figures is still managing to show some growth improvement.

On balance the global economy is struggling, but it is growing. Progress is being made. The BIS has put off for some time its requirement for stricter capital asset ratios on banks, and that may help banks and may help growth in the short run. Meanwhile, there are many fiscal challenges and many private sector challenges that these economies are trying to surmount. The interim view of the OECD is that progress is being made.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.