Global| Aug 10 2020

Global| Aug 10 2020OECD LEIs Continue to Turn Up But Signals Remain Weak

Summary

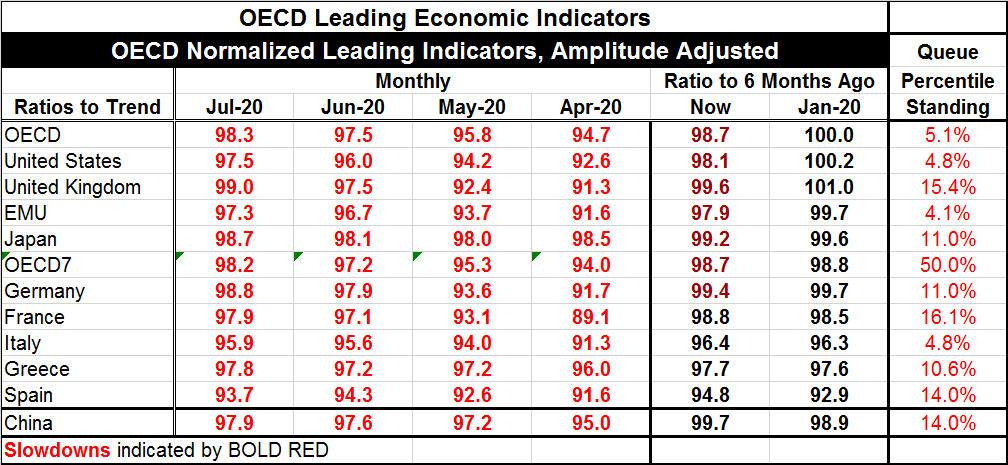

The OECD total amplitude adjusted LEIs are below 100 across the board, a sign that the composite statistics that form the indexes are below their normal values. These readings point to ongoing weak growth although they mark [...]

The OECD total amplitude adjusted LEIs are below 100 across the board, a sign that the composite statistics that form the indexes are below their normal values. These readings point to ongoing weak growth although they mark improvements month-to-month for every entry in the table. In fact, all except Greece had improved for two months in a row and ten of them (out of 12) have improved for three-months running from a very weak April reading. Japan had deteriorated in May; Greece was flat month-to-month in June; those are the two exceptions. The record is one of ongoing improvement, but it is a slow pace emitting still very weak signals. There is nothing here to hang your hat on.

The OECD total amplitude adjusted LEIs are below 100 across the board, a sign that the composite statistics that form the indexes are below their normal values. These readings point to ongoing weak growth although they mark improvements month-to-month for every entry in the table. In fact, all except Greece had improved for two months in a row and ten of them (out of 12) have improved for three-months running from a very weak April reading. Japan had deteriorated in May; Greece was flat month-to-month in June; those are the two exceptions. The record is one of ongoing improvement, but it is a slow pace emitting still very weak signals. There is nothing here to hang your hat on.

The ratio of the current readings to their respective values of six months ago, a preferred OECD comparison, shows all are weaker now than they were six-months ago. And if we compare the readings of six months ago with values from six months earlier, we find that seven entries are weak over six months and weaker than their ratio to six months from six months ago as well. Six months ago only the OECD as a whole, the U.S. and the U.K. had ratios above unity indicating that only for those three were values above their respective levels of six months ago – demonstrating expansion. There had been a broad slowing in place prior to intrusion of covid-19.

In addition to poor momentum, all the individual countries and the EMU metrics are below their 50 percentile queue ranking, a sign of weakness that puts them below their historic medians. In fact, the queue rankings are exceptionally low. While there is a multi-month revival in place, it is in slow-motion.

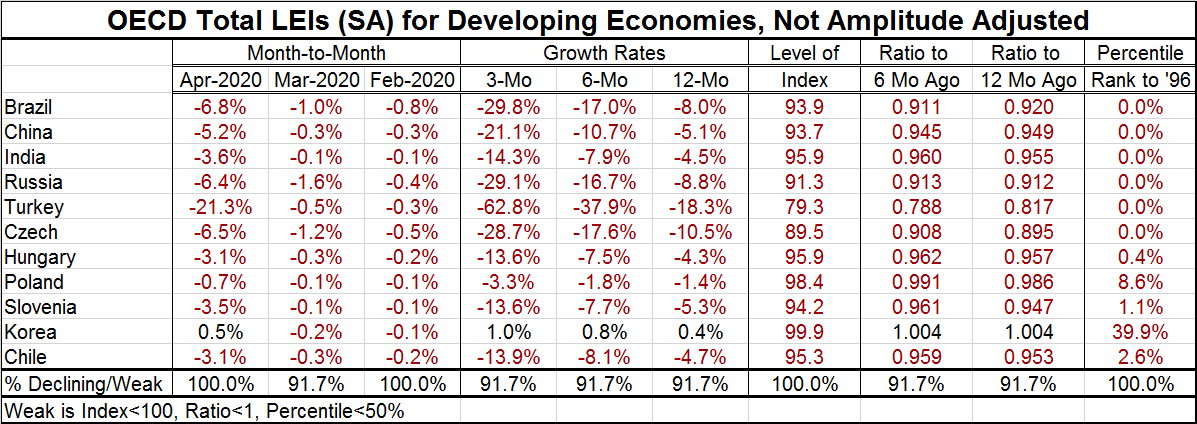

Developing economies’ total LEIs show ongoing across the board weakness. South Korea is the lone exception. These are not amplitude adjusted readings. Turkey seems to be undergoing an intense episode of downturn at the moment. All have ratios to six-months ago below unity (except South Korea) and six-months ago all had ratios below unity as (except South Korea) signaling a broad slowing down under way. The declines progressively deteriorate (except South Korea). The percentile rankings are terribly low for all of them; low but not quite as terrible for South Korea.

On balance, the OECD LEIs signal broad slowing in the global economy. As much as we have been focused and concerned about the developing world and the potential for backsliding and for reinfections to introduce new weakness the developed world, the developing world is in much worse shape. The LEI framework reemphasizes how bad off these countries are with extremely weak queue standings.

The rise in gold prices make sense against this background. Agricultural prices are weakening however. In the U.S., farmers are letting field lie fallow. Some farmers are choosing to not grow corn because ethanol demand is down and prices are so weak. Cotton prices and plantings also are down in the U.S. as demand for clothing has been weak. Farmers are hoping this is a one-off event, but of course nobody knows. Developing economies tend to depend more on the prices of commodities so weak prices hurt them much more. The covid crisis continues to touch on everything everywhere and tends to keep any forecast or view of the future on its back foot.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief