Global| Aug 11 2014

Global| Aug 11 2014OECD LEIs Are Mostly Flat; Should They Be Even Worse?

Summary

The OECD's leading economic indicator for June posted a reading of 100.5, the same as it's been for the last eight months. The OECD portrays this as indicating ongoing expansion. However, there clearly is no acceleration in the cards. [...]

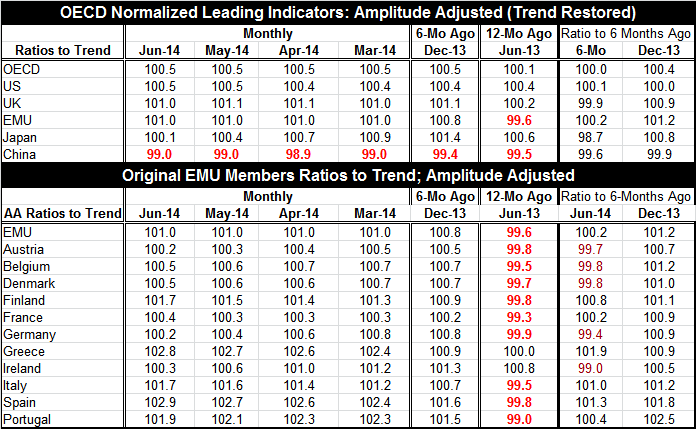

The OECD's leading economic indicator for June posted a reading of 100.5, the same as it's been for the last eight months. The OECD portrays this as indicating ongoing expansion. However, there clearly is no acceleration in the cards. The U.S. reading at 100.5 in June was the same as in May, up from 100.4 in April and in March and back to December of last year. The U.K. declined to 101.0 in June from 101.1 in May. Its signal has been waffling between those two values since November of last year. The European Monetary Union is stuck at 101.0 in June and has been since February of this year. Japan decelerated to 100.1 in June from 100.4 in May; its previous values were 100.7 in April and 100.9 in March. Japan continues to suffer from the implementation of its VAT tax. China's indicator was at 99 for two months running. That's up from 98.9 in April but it was previously higher and yet has been below 100 since April 2013. China's value is the only one below 100, indicating some mild deceleration.

The OECD's leading economic indicator for June posted a reading of 100.5, the same as it's been for the last eight months. The OECD portrays this as indicating ongoing expansion. However, there clearly is no acceleration in the cards. The U.S. reading at 100.5 in June was the same as in May, up from 100.4 in April and in March and back to December of last year. The U.K. declined to 101.0 in June from 101.1 in May. Its signal has been waffling between those two values since November of last year. The European Monetary Union is stuck at 101.0 in June and has been since February of this year. Japan decelerated to 100.1 in June from 100.4 in May; its previous values were 100.7 in April and 100.9 in March. Japan continues to suffer from the implementation of its VAT tax. China's indicator was at 99 for two months running. That's up from 98.9 in April but it was previously higher and yet has been below 100 since April 2013. China's value is the only one below 100, indicating some mild deceleration.

In the far two right-hand columns, we look at the ratio of the current readings to six months ago and of six months ago to 12 months ago. On that basis, we see that the U.K., Japan and China have decelerated from the readings of six months ago. The EMU and the U.S. have accelerated slightly. The OECD reading is exactly unchanged. Looking at that six-month reading compared to the previous six months, we see increases across the board except for China.

Turning to the countries that were the first members of the EMU, we see values above 100 for each member. Six months ago all the values were above 100 as well; 12 months ago all of the values were below 100 except for Greece and Ireland. When we look at the current values compared to six months ago, we see that there have been accelerations in Finland, Portugal, Spain, Italy, Greece and France as well as for the EMU. France and Italy are strange members on that list since their growth has been sputtering and Italy has dropped into recession. All EMU members accelerated six months ago compared to the previous six months.

These OECD leading indicators for the EMU are above 100, indicating there's some acceleration in progress. However, very few of the numbers are very strong. The strongest reading is for Spain, which has been putting on some very good economic numbers recently. Portugal, which has recently had some turbulence due to banking problems, also has a relatively high OECD score as does Italy, despite its current problems as it has plunged into recession. Finland has the same reading as Italy at 101.7. There are weak readings in the EMU from Austria and Germany, both at 100.2. Slightly stronger is Ireland at 100.3, France at 100.4 and Belgium and Denmark at 100.5. Notice that the OECD indicators have failed to predict Italy's slide into recession.

There have been some uneven data from Europe recently. Yet, the OECD leading indicators do not show any evidence of declines. OECD Indicators do show the impact of better growth in Spain and worse growth out of Germany. The OECD indicators, therefore, do seem to be picking up the same sorts of things that we are seeing in ordinary economic indicators. However, since economic news has continued to get worse and since these indicators are only available through June, it's too soon to say that the signal from the indicators trumps the weak and uneven readings from the monthly data. And then, of course, there is the small matter that these signals failed entirely to pick up Italy's dip into recession.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief