Global| Mar 09 2021

Global| Mar 09 2021OECD LEI Ticks Higher for the Eighth Straight Month of Gains

Summary

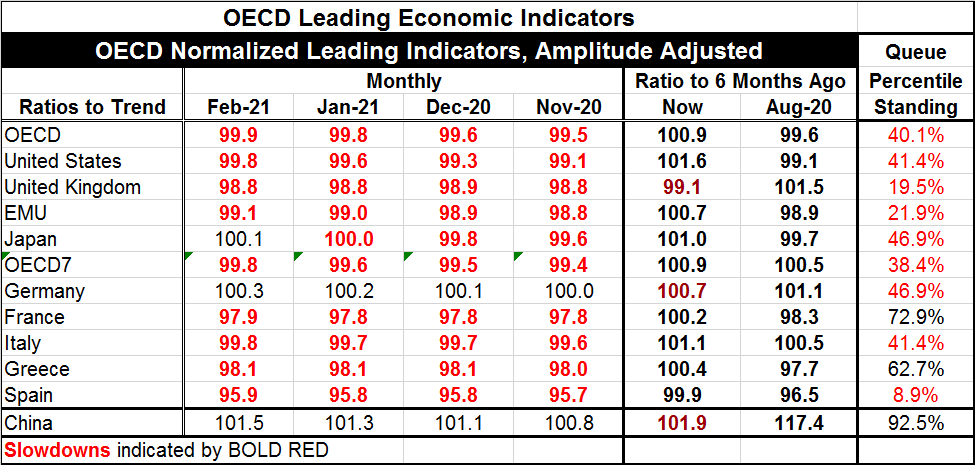

The OECD LEI continues to claw its way to higher ground. It has now risen month-to-month for eight months in a row. The LEI rose by one tick in February, by two ticks in January, and by one tick in December. While this is a steady [...]

The OECD LEI continues to claw its way to higher ground. It has now risen month-to-month for eight months in a row. The LEI rose by one tick in February, by two ticks in January, and by one tick in December. While this is a steady progression higher, the progress has become painfully slow. Only three countries in the table Germany, China and Japan have OECD index levels of 100 or more. The 100 designation indicates more or less normal growth. Countries rising above 100 are experiencing above trend growth; countries below 100 are experiencing below trend growth. Most countries/regions in the table have LEI index values in the 99 range; this includes Italy, the EMU and the United States. Greece and the United Kingdom sport values in the 98 range. Spain has a reading at 95.9. The OECD aggregate has a reading at 99.9 while the overall OECD7 reading is at 99.8 very near normalcy or trend.

As a predictor, the OECD likes to look at changes over six months. Two columns in the table show changes over six months; the first is for changes over the recent six months and the other is for changes on the six months before that. All countries except the U.K. show ratios above 100 (the ratio of the current index to six months ago multiplied by 100). And all are showing a speed up compared to their values of six months ago except the U.K., Germany and China.

The percentile standings of LEIs place them in a ranked queue of data back to November 1996. On this basis, only China, France and Greece have percentile queue standings above 50% which place them above their historic medians on that timeline. The OECD aggregate resides at its 40th percentile with both Germany and Japan at their 46.9 percentile, and Italy and the U.S. each at their 41.4 percentile. Even so, the whole of the EMU resides at its 21.9 percentile. The OECD7 is at its 38.4 percentile. Spain has the weakest relative standing at its 8.9 percentile (weaker since 1998 less than 9% of the time).

On balance, the OECD shows that the OECD area is gaining momentum and recovering, but that conditions are still for the most part close to or below what have been historic norms. However, the OECD is beginning to change its tune. It now sees the global economy as set to grow at a faster pace this year than projected earlier. A faster than expected roll-out of vaccinations and a better outlook for the U.S. economy made on the back of a huge stimulus program are the main reasons for the shift in view. The Paris-based think-tank raised the global GDP growth forecast for this year to 5.6% in its latest interim economic outlook report that was just released. This is up from the 4.2% it previously had seen in December.

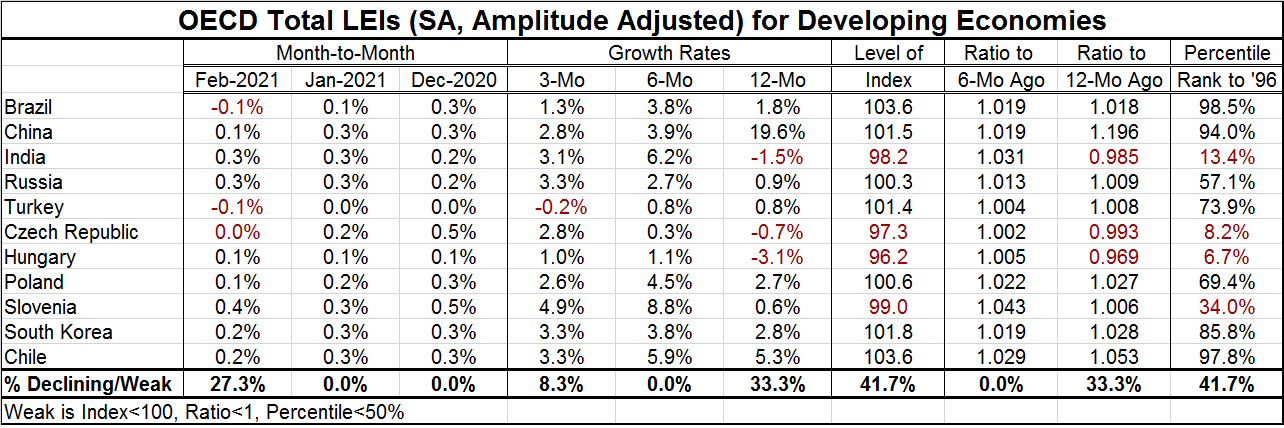

The OECD LEIs also show the impact on developing economics (we place China in this table as well). Among the countries listed in the table, only Brazil, Turkey and the Czech Republic reported slippage in February; there was no slippage in January or in December. Growth rates tabulated from 12-months to six-months to three-months show growth picking up over six months compared to 12 months (China excepted) and growth is slowing over three months compared to six months (Russia and the Czech Republic excepted). All countries show a step-up in their respective LEIs over six months compared to six months ago. The current index ratio to 12-months ago is weaker in India, the Czech Republic and Hungary.

The percentile queue standings for the developing group are quite mixed and varied. Three countries (Czech Republic, Hungary and India) have extremely weak current standings of their respective LEIs. In addition, Slovenia is below its median. Russia, Poland and Turkey have moderately firm standings in the 50th-70th deciles of their percentiles. Brazil, Chile, China and South Korea have especially strong standings. Note that countries that are heavily engaged in international trade are at the top of the performance list. For Chile, it may be because commodities especially copper prices are doing so well. Global trade is recovering and manufacturing sectors are carrying the day for growth across most countries and the services sector continues to be hobbled by the spread of the virus. The vaccine roll-out may be proceeding ahead of schedule, but it is still in its infancy especially for most developing economies.

Impact on Developing Economies...

While there is a decided pick up in optimism, health officials are still trying to throw a wet blanket over the optimism. In the U.S., Anthony Fauci is warning that the vaccine roll-out is still fresh and that the U.S. does not have enough immunity natural or vaccine-induced to provide enough buffer; a fourth wave of infection is possible with the new variants circulating and expanding their share of total infections. Health officials want to make sure that there is no backsliding even though U.S. data (for example) show sharp improvement and now the lowest infection rate since late-November of last year. The problem is the ‘Chicken-Little effect’. Health officials have always been warning that things could go much worse than they have actually gone. Even when they were right about infections spreading again, they have exaggerated the risk. In this latest round of infections generally, infections globally have exceed earlier peaks but deaths have not been commensurately as large as infections. Infection without death spreads herd immunity in the community. For now health officials are having a hard time coping with what looks a lot like success. Will the winning streak against the virus last or will the variants push through and create an unexpected additional wave? Of course, the LEIs know nothing about all this…

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief