Global| Apr 13 2009

Global| Apr 13 2009OECD LEI's Are Sinking At The Fastest Pace In Over 40 Years

Summary

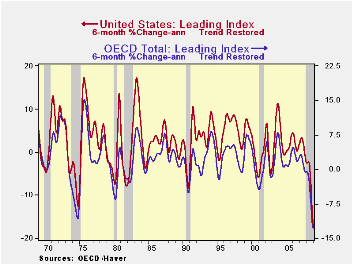

The OECD trend restored leading indicators show that a very deep recession is underway. The declines in the LEIs over 6-months are the most severe of the modern post-war period. The LEI declines are sharper than in either of the two [...]

The OECD trend restored leading indicators show that a very

deep recession is underway. The declines in the LEIs over 6-months are

the most severe of the modern post-war period. The LEI declines are

sharper than in either of the two severe global recessions of 1973-75

and 1981-82. The 1973 recession was spawned by a similar common cause:

higher world oil prices and subsequently an oil embargo on the US by

Arab countries. The 1981-82 recession was the result of central banks

finally drawing a line in the sand over inflation. The last two (US)

recessions were not especially severe and except for the grey bars that

identify them as recessions, they might be hard to recognize as such by

the amplitudes of the indices alone. But the current cycle is readily

recognized.

Moreover history shows how the US cycle has dominated the OECD

cycle. Despite a view ahead of this cycle that there would be some

decoupling, especially for the developing (non OECD) world it did not

happen. There is no evidence of decoupling in the US-OECD comparisons

and indeed, developing economies did not decouple at all. China’s and

India’s strong growth cycles and the huge building boom in the Middle

East all were undercut by the severity of this cycle. The flaw in this

logic was that all these regions depended heavily on trade and the US

economy was the engine of growth. Despite having powerful domestic

forces for growth, the rest of the world could not do without the

strength of the US economy. Decoupling was an idea without much basis.

The OECD indices show how much the entire OECD area moves in sync with the US economy. Recovery depends on the US economy too. So far there are some signs of green shoots according to the Fed Chairman and some glimmers of hope according to the President. But there is nothing for certain. The OECD area is still declining aggressively. The ECB could still cuts rates more. European stimulus is still being portioned out. China is now talking about doing more. While Japan looks to be on the brink of more deflation, in the US a core of believers is becoming concerned about eventual inflation.

| OECD Trend-restored leading Indicators | ||||

|---|---|---|---|---|

| Growth progression-SAAR | ||||

| 3Mos | 6Mos | 12mos | Yr-Ago | |

| OECD | -10.4% | -12.3% | -9.1% | 0.1% |

| OECD7 | -13.3% | -14.6% | -10.2% | -0.4% |

| OECD US | -16.4% | -17.6% | -11.7% | -0.4% |

| Six month readings at 6-Mo Intervals: | ||||

| Recent six | 6Mo Ago | 12Mo Ago | 18MO Ago | |

| OECD | -12.3% | -5.7% | -0.6% | 0.9% |

| OECD7 | -14.6% | -5.6% | -1.5% | 0.6% |

| OECD US | -17.6% | -5.5% | -2.6% | 1.9% |

| Slowdowns indicated by BOLD RED | ||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief