Global| Sep 09 2015

Global| Sep 09 2015OECD LEI Barely Goes Over the Hurdle of Neutrality

Summary

The OECD has put a brave face on its new round of leading indicators, portraying the global economy with stable growth. When these indicators are at 100, they are indicating no tendency to accelerate of decelerate so the overall OECD [...]

The OECD has put a brave face on its new round of leading indicators, portraying the global economy with stable growth. When these indicators are at 100, they are indicating no tendency to accelerate of decelerate so the overall OECD gauge can be properly be identified as the OECD has done. But is that the best reference to what this gauge really means? Maybe not.

The OECD has put a brave face on its new round of leading indicators, portraying the global economy with stable growth. When these indicators are at 100, they are indicating no tendency to accelerate of decelerate so the overall OECD gauge can be properly be identified as the OECD has done. But is that the best reference to what this gauge really means? Maybe not.

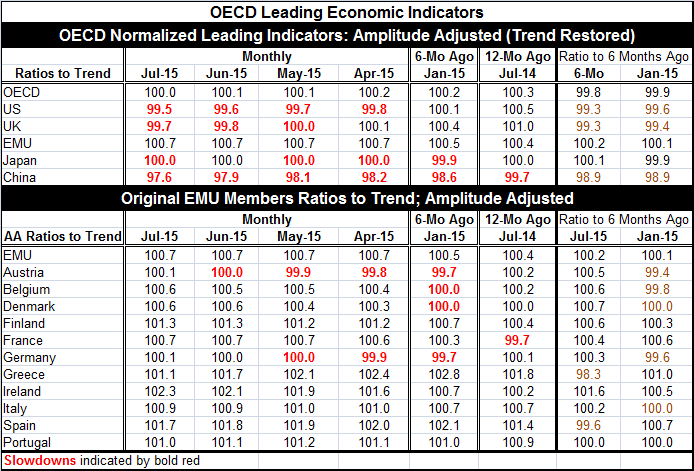

First of all, the global economy is growing slowly and poorly. The indication that growth is only stable in this trajectory is not good news to anyone. Of course, contracting growth would be worse, but the news as it stands is still touch-and-go. The overall OECD gauge slipped to 100.0 in July from 100.1 in June. In April it was at 100.2. The clear indication is that while there is not much momentum, what momentum there is, pushes global growth lower. That has not been the OECD's headline message, but it also is true.

We see that the U.S., the U.K., China, and Japan (if not rounded) have OECD LEI values less than 100 (the bold red indicates that the actual numerical value is below 100). These indicate slowdowns. It means we have the number one, the number two and the number three economies of the world in a slowing mode. Danger! Yes! But the OECD characterizes growth as `stable'. It seems the wrong emphasis to me. Additionally, with the U.S. in a slowing mode already, the Federal Reserves is seriously considering raising rates. If you were at the OECD, wouldn't you want the Fed to recognize this danger? Or would you rather suppress it so the Fed could go ahead and do what it wants with fewer impediments to deal with? Oh, let's remember that the U.S. is an OECD member and contributes to its output.

To be sure, the path of the global economy is not changing very rapidly. In some great broad sense, growth is simply about what it has been or some time. But technically, the OECD indicator for July is below where it stood six months ago and six months ago it was weaker than it had been six months prior to that. So while the OECD LEI series is moving slowly, it is nonetheless clearly marking erosion - ongoing erosion.

It is now quite clear that China is slowing. Its current index is a low 97.6 and it has slowed over six months and six months ago it was lower than it had been six months before that. China's slowdown is well baked in the cake.

The U.S. and U.K. are like two peas in a pod with indices below 100 in July and back to at least May and with current indices lower than they were six months ago and again six months before that.

The relative `bright spot' (and who have thought that?) is the EMU! The EMU gauges have been stuck at 100.7 for five months in a row and are a tick higher on balance over six months and that level is up from six months previous. The EMU has positive - if slow - upward momentum.

None of the earliest EMU members listed in the table have OECD LEI values less than 100. Only Austria, Belgium, Denmark and Germany show weaker values than six months ago (and for Belgium and Denmark the drop is only very technical, occurring before rounding).

Angela Merkel's claim that austerity (Germany's choice for the EMU) has been paying dividends is hard to argue with. Of course, there has been a cost. We are looking at momentum relative to six or 12 months ago while on a broader time horizon some of these members are still not looking so rosy. But on this near-term horizon, Germany can claim a success story. Of course, Greece still has to get through its next election cycle.

But right now we have very little in the way of encouraging momentum. The recent G-20 meeting affirmed that its members would not seek to employ competitive devaluations as a strategy to boost growth at home. But we will have to wait to see how this works out. Dropping commodity and oil prices are a mixed blessing. They impact adversely growth in the countries and industries that produce these goods and boost spending power among those nations that consumer these goods. It seems that in the short run, the adverse impact on supply disruption has been dominant. Many developing economies need commodity sales and revenue to fuel growth. Lacking that, they have been struggling. Among consumer nations such as the U.S. and the UK, there is also production and shutdowns of production has sent adverse ripple effects through those economies.

Beyond that there has been little written about how this shift in the oil price levels does to investment and growth going forward. Where will oil settle? What do people think about the future? What about investments made on the idea that gasoline would cost $4-$5/gallon? Now it is $2-$3/gallon? What does it do to desired commuting patterns? Will people still want to live in the city (low cost commute) or will they prefer suburbia? This uncertainty can crimp growth on an ongoing basis until there is some certainty about price levels for oil in particular but other commodities as well.

Of course, the world is complicated. As the U.S. struggles with supply effects, it also benefits from consumption effects due to lower prices for inputs and consumables. There is also a strong dollar to contend with and the confidence impact of global unrest on consumers.

It is fair to say that the global economy has a lot of balls in the air. If markets can stabilize, maybe some of the benefits of the lower prices can take hold. But policymakers have to do the right thing to calm markets. In China, the authorities seem clueless. In the U.S., the Fed is so determined to hike rates; it's hard to tell what it will do. Many Fed officials seem to be so compulsively worried about the long run that they have no concern at all about what a rate hike will do in the short run. The Fed may yet hear the voice of reason, but we also know that many Fed members are adamant about raising rates. If the Fed, the central bank of the world's principal reserve unit, the dollar, does hike rates, it is hard to tell how far and wide the repercussions will spread. It is fair to look at the OECD indicators and realize that they do not depict a stable situation, just one that is largely unchanged and that represents largely unfulfilled expectations. Do not take solace in the OECD's LEIs this month. It's not what they do say, but what they don't say that is chilling.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief