Global| Mar 06 2018

Global| Mar 06 2018OECD Area Inflation Stays Down - Will Tariffs Push It Up?

Summary

Oil prices continue to try to work some inflation mischief in the background, but OECD area inflation in January ticked lower to log a 2.2% gain over 12 months, a tick below its December pace of 2.3%. The core inflation rate also [...]

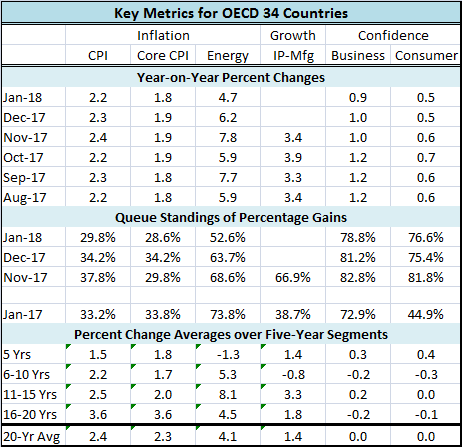

Oil prices continue to try to work some inflation mischief in the background, but OECD area inflation in January ticked lower to log a 2.2% gain over 12 months, a tick below its December pace of 2.3%. The core inflation rate also ticked lower to post a 1.8% gain in January, down from 1.9% a month earlier.

Oil prices continue to try to work some inflation mischief in the background, but OECD area inflation in January ticked lower to log a 2.2% gain over 12 months, a tick below its December pace of 2.3%. The core inflation rate also ticked lower to post a 1.8% gain in January, down from 1.9% a month earlier.

Core inflation continues to be very stable in the just-below-2% range. The core rate peaked its head above the 2% mark last on December 2011 and then promptly went back below 2%. It had previously been above 2% in December 2008. In October 2010, core inflation bottomed in the OECD area at 1.09%. By August 2011, it was back up to a 1.8% pace and has continued at about that pace since with some fluctuation, of course, staying below the 2% threshold.

The core inflation rate over the last four months has reached a 26-year low in terms of its inflation variability. I measure this as the standard deviation of the year-on-year inflation rate over the last 18 months. As of January, the inflation stability reading has been lower only 0.6% of the time over the last 26 years. That amounts to only two previous instances and those occurrences were November and December of last year. Inflation in the OECD area is low and rock-stable.

Headline inflation is a quite a bit less stable as its rank is only in its 63rd percentile over the last 26 years. For example, prior to 2007, headline inflation was usually more stable than it is right now. The ranking for headline inflation lines up with the 64th percentile standing for energy inflation in January. Energy price variability is one of the main drivers of headline price inflation variability and oil is at it again.

This back ground of sub 2% inflation for the 34 countries in the OECD area is another reinforcement of current low inflation trends throughout the OECD area.

This inflation performance is one of the main reasons that inflation in the major monetary center countries of the U.S., Japan and the EMU has remained so low. It acts like a fly wheel on a drive shaft and keeps the stability of this pace in place despite shocks. Of course, this is also a chicken-and-egg problem where low inflation in the monetary centers tends to promote low inflation throughout the region and low inflation in the region supports the low inflation in the center countries. But the main issue here is that with inflation so low in the OECD area policy mistakes that might lead to inflation being imported are not as dangerous.

Is there an inflation risk from tariffs?

This is point to be kept in mind as tariff talk circulates. If foreign inflation runs only at 2%, then a sustained inflation impulse from overseas can only be sustained at 2%. However, in case of tariffs or of currencies being knocked for a loop, more inflation is possible at least in regimented bursts. As things stand, aluminum and steel are relatively small items in terms of trade importance. Even though tariffs of 25% and 10% are large, the impact on U.S. inflation of these tariffs being imposed is small. What would happen is that foreign metal would either come into the country with a huge tariff surcharge on it, raising the import price and domestic costs, or foreign sellers would be so 'priced out of the market' that domestic metals would simply trade domestically at much higher prices.

The risk to inflation would come if countries overseas retaliated imposing their own tariffs and if the U.S. then imposed counter measures on these measures, and you can see the possibility of this getting out of control. In fact, the more out of control it gets, the more that the risk would swing to deflation and away for inflation.

Europe has already expressed concern, for example, that a U.S. umbrella tariff, rather than a targeted tariff, would deflect foreign steel to their own market and push prices even lower creating a disinflationary impulse.

If currency rates began to move in response to the various shifting of commercial polices, a further element of inflation transmission could be activated. When a currency rate moves, what happens is that the shift changes the foreign price level experienced in the U.S. economy and the realignment gets amortized as higher inflation providing an added kick to the underlying foreign pace for a time, until it has run its course. But the basic inflation being created from overseas is still the roughly 2% we see in the OECD area. The 'extra' inflation created by currency depreciation is temporary.

If things were to 'get out of hand,' my greater fear would be for growth, stock prices and deflation not for inflation.

What is the objective?

It should be clear to everyone involved that like it or not Donald Trump is trying to change the 'world order' that has been in place for the last nearly 40 years. U.S. trade partners are used to certain behaviors and practices that have culminated in the U.S. having had an unrelenting string of current account deficits from about 1980 onward. While deficits per se are not bad, the U.S. has been running deficits that have fancied consumption not investment. Thus, the debt that has been run up in conjunction with them (or the assets that have been depleted) has not been deployed productively and it represents a liability we hand down to future generations from our own largesse.

The President seems to be trying to get back to a world order where countries do not run persistent deficits or surpluses any more. It was thought that under floating exchange rates, markets would drive exchange rate movement to equilibrate current account imbalances. But that has not happened largely because national policies have interposed themselves and countries used foreign exchange buying practices to add to foreign exchange reserves and to keep their currencies weak and their exports strong. This is what Trump apparently wants to change. We don't know because he has not announced a grand strategy. But if that is his objective, it would put America on a path to improved jobs growth and a better shot at jobs in international industries. Of course, in such a world if exchange rates are going to adjust perpetually to rebalance current accounts, we could find the dollar under more persistent selling pressure. That could be an environment with more inflation than we are experiencing these days. But that is down the road. And it is not clear if the rest of the world is willing to play the game by its intended rules since they are all geared up to continue to play under what have been the prevailing rules.

If I am right about what Trump seeks to do, it is a strategy that is disruptive and it is disruptive to the current distribution and deployment of corporate assets and properties internationally. Not only will foreign economics not like it, but U.S. multinational corporations with operations that take advantage of current practices will be less productive. The Trump strategy may be good for growth and jobs in the U.S., but corporations spend a lot of resources overseas so this policy tilt may not be good for the stock values of multinational corporations at all. And this is not just because there is protectionism. It is because the world order will be in for a disruption because of what protectionism seeks to undo. For Trump, protectionism is not the end-game. It is only a tool. We need to assess what Mr. Trump really wants to accomplish.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief