Global| Dec 12 2014

Global| Dec 12 2014Never-Ending Process of Adjustment in the Euro Area

Summary

Inflation in the euro area remains contained. In fact, it remains way under the level to which it is supposed to be contained. Inflation is so low that it is out of control in a manner not appreciated and not planned for by the [...]

Inflation in the euro area remains contained. In fact, it remains way under the level to which it is supposed to be contained. Inflation is so low that it is out of control in a manner not appreciated and not planned for by the founders of the European Monetary Union. Therefore, the EMU itself is out of control.

Inflation in the euro area remains contained. In fact, it remains way under the level to which it is supposed to be contained. Inflation is so low that it is out of control in a manner not appreciated and not planned for by the founders of the European Monetary Union. Therefore, the EMU itself is out of control.

The EMU remains a work in progress. It is probably true that the best explanation of what the EMU is, is that it is a union formed for political reason that has imposed economic conditions on counties not totally suited to be bound together in that fashion. And it is paying a price for its lack of attention to details.

For the moment, the euro turns out to be a fiat currency with many of the same drawbacks as a gold-based system. I doubt that members thought it would work that way when they joined. Economic conditions in the EMU are weak. The inflation rate is under the goal that is set for it and has been below that goal for some time (nearly two years). Yet, the guardians of the euro area and the charter of the ECB continue to prevent this fiat currency from adopting suitably stimulative policies, rendering it much the same as a system based on gold.

The ECB was not outfitted for a plan of attack should inflation fall persistently below its objective. In fact, its rules were so geared to prevent it from creating or tolerating inflation that the prospect of deflation was totally ignored. And the ECB was set up to ignore other risks as well. Despite concerns about inflation and a known bias for inflation among many EMU member nations, the ECB was given no monitoring role, no mandate and no tools to address any inflation that might arise at the member-country level. The ECB was only concerned with the impact of any nations' inflation rate to the extent its weighted impact affected the EMU overall HICP. In hindsight, the ECB's mandate, focus and tool box were too limited. The lack of a common fiscal policy meant that monetary policy should have been more vigilant and more interested in eradicating regional differences in inflation. But it was not.

Maybe in the future, EMU members will release the ECB from its constraints to allow it to employ a QE procedure or something like it to address deflation. However, for the moment, with constraints on the EBC fully biding, it is not allowed to take such steps. As result, the ECB continues to miss its target shattering its reputation as a credible target-hitting central bank.

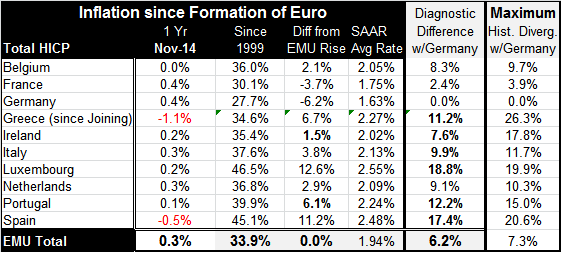

The chart above shows how through the process from financial crisis to recession to aftermath Germany has transited from being the persistently low inflation country (see Table, too) to being the high inflation country. Germany's 12-month inflation rate is as high - or higher - than any EMU member in November. Conversely, Germany has seen its price level rise THE LEAST of any EMU member country since the inception of the EMU.

The EMU was like an Alfred Hitchcock movie with a bomb ticking and the moviegoers seeing it but the participants unaware, going about their normal business. As it would be in the movies, EMU participants were shocked and devastated when things blew up. Those of us watching from a distance, as if at the movies, had been warning of the inevitable explosion for some time but were rebuffed. So now Germany is the high inflation country and it has been this way for about the past year. Germany has not undertaken the role to reflate, rather German inflation has fallen even below its past low tendencies but other EMU countries have suffered an even more severe deflation. In this situation, they can only slowly and painfully gain back the competiveness lost to Germany since joining the EMU.

The EMU's battle with deflation comes as a consequence of its individual members having ignored the EMU-wide inflation target of 2%. Only France and Germany have seen inflation average less than the ECB's 2% per year top tolerable rate since the advent of the EMU. But since every EMU member was in the same currency area those with higher local inflation rates, were losing competiveness to countries that held inflation in check. These `renegade' EMU members were oblivious to the fact that Germany (and France) having such large weights in the EMU allowed other countries to maintain an overshot while the ECB still hit its only target of interest. But that did not prevent those inflation imbalances and troubles from building up and eventually blowing up in their own faces.

The table makes a comparison between the largest price level divergence each country has had with Germany during its life in the EMU. The maximum divergence can be compared with each nation's current divergence. What we see up and down the line is that every country has improved relative to its worst competitive position with Germany- but some have made much more progress than others.

Greece and Ireland have made a huge amount of progress. But Luxembourg, Portugal and Spain have not made as much progress. These countries are still at a huge competitive disadvantage relative to Germany in comparison with where they were when the EMU was first formed. Spain is still suffering a great deal of deflation. Luxembourg, being a financial center, is much less affected by all this.

The chart below shows that the countries that have had fiscal issues, Greece, Portugal, Spain and Ireland, have been running inflation rates at or below zero for over a year. Germany has run an inflation rate (0.4% year-over-year) that is well below its average rate since joining the EMU (1.6%) so countries that lost competitiveness to Germany have improved their competiveness standing by running inflation rates that are even lower. Germany has not reflated to make the adjustment any easier. In fact, Germany is trying even harder to reduce its own fiscal deficit further, a deficit which is already quite low.

For now the EMU is a Zone with some very odd bedfellows. While it is a currency union and also a customs union (within the EU), it does not have any but the most rudimentary aspects of a common fiscal policy. And what is there is only to support the regulatory structure of the EMU/EU. There is no EMU-wide fiscal policy and that makes it harder for European nations to think as one.

For now the EMU is a Zone with some very odd bedfellows. While it is a currency union and also a customs union (within the EU), it does not have any but the most rudimentary aspects of a common fiscal policy. And what is there is only to support the regulatory structure of the EMU/EU. There is no EMU-wide fiscal policy and that makes it harder for European nations to think as one.

Despite the low EMU inflation rate, the Germans are still guardians of the sanctity of the ECB treaty. They apparently are blind to the problems of its fellow member nations- or they are insensitive to them. Despite EMU inflation at 0.3% year-over-year, the euro area's monetary conservatives fear any policy deviations that might set a precedent for the future. But with EMU inflation at 0.3%, German inflation is at 0.4%, Portuguese inflation is at 0.1%, Belgian inflation is at zero, Spanish inflation is at -0.5% and Greek inflation is at -1.1%. Ireland, Italy, Luxembourg and the Netherlands each have annual inflation rates below Germany's pace. How can inflation be the issue? Why would any EMU member want to cripple the ECB and keep it from boosting prices to put inflation back at its target? You can bet that if inflation were 1.7% above its target at 3.7% (instead of 1.7% below it), the Germans would be howling for a tightening.

The ECB has a clear bias for deflation over inflation. Its charter was poorly set to prevent it from taking special action in the event of deflation and the Germans, the Austrian and the Dutch may be determined to keep it that way. Still, the lack of symmetry in ECB policy is a problem. I continue to wonder if it will become a fatal problem. Germany is easily able to prosper in this low inflation environment while that puts so much pressure on other EMU member nations that, to improve their competitiveness, must run inflation rates even lower than Germany's. This hardly seems to be a sustainable situation. The so-called internal devaluation model is in play. Make no bones about it: it is a policy of deflation and it is creating huge differences in the welfare among the people of the EMU. How long can it last?

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief