Global| Feb 10 2010

Global| Feb 10 2010Much Of EMU’s IP Stumbles In December...How Worried Should We Be?

Summary

The drop –a sharp drop- in German IP has been echoed throughout the e-zone’s largest economies. In December IP has also fallen in France, in Italy and in Spain. The UK, an EU member country, reports that its IP rose by a strong 0.9% [...]

The drop –a sharp drop- in German IP has been echoed throughout the e-zone’s largest economies. In December IP has also fallen in France, in Italy and in Spain. The UK, an EU member country, reports that its IP rose by a strong 0.9% in December.

Over three-months all the large EMU members are showing moderating growth rates but only Germany and Spain have posted actual IP drops. Germany’s -14% rate of decline is huge. Spain’s three-month drop is just at a -4.7% annual rate- but is still substantial. Italy’s 5.9% gain over three months is the sharpest 3-mo gain among the lot of large e-Zone members. Outside the Zone, the UK’s 4.6% rise in output rivals Italy’s three-month gain. Better still, for the UK the acceleration in output is still in place.

For the fourth quarter, Germany continues to show that output expanded compared to Q3 even with the December weakness. France’s output also posted a rise in the quarter. Both Italy and Spain suffered setbacks in the quarter; Spain’s 6.2% annual rate of decline is especially deep. The UK’s IP registers a rise at a pace of 3.2% in the quarter.

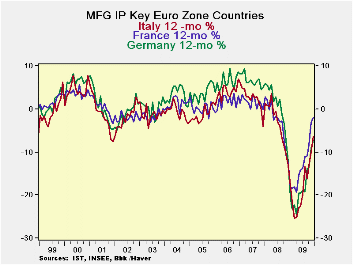

The chart at the top of this report plots Yr/Yr rates of growth and on that basis the recovery in output still seems to be fully in train. But the widespread drop off in output in December must be taken as bad news. But how bad? The UK is not in EMU but it is still in the same region and trades with most of the same partners as Europe yet its IP managed a rather large boost in December. Perhaps the UK results give us some reassurance that output in the Zone is not on the brink of collapsing. It’s too soon to tell what December means for the trend but the drop off is not the sort of signal of weakness or even of slowing growth that we want to see at this time. The recovery’s fragility underlines Mervyn King’s statement that it is too soon to put a definitive end the BOE’s securities purchase program.

Meanwhile those looking for more guidance on policy will have to wait another day. US central bank head Ben Bernanke has his testimony put off for a day due to a Washington DC snow storm. We will not get the usual information from questioning of the Chairman until he testifies on Thursday. But the Fed Chairman’s speech is being released on time today so his general thoughts will available as previously scheduled.

| Main Euro-Area Countries and UK IP in MFG | |||||||

|---|---|---|---|---|---|---|---|

| Mo/Mo | 3-Mo | 6-mo | 12-mo | Dec-09 | |||

| MFG Only | Dec-09 | Nov-09 | Oct-09 | Dec-09 | Dec-09 | Dec-09 | Q:4-Date |

| Germany: | -2.8% | 0.9% | -1.8% | -14.0% | 1.9% | -7.2% | 3.6% |

| France:IPxConstruct'n | -0.1% | 0.6% | -0.1% | 1.4% | 4.6% | -2.3% | 0.3% |

| Italy | -0.1% | 0.4% | 1.2% | 5.9% | 6.7% | -6.3% | -1.4% |

| Spain | -0.6% | -0.1% | -0.5% | -4.7% | 1.2% | -2.4% | -6.2% |

| UK | 0.9% | 0.2% | 0.0% | 4.6% | 2.3% | -1.9% | 3.2% |

| Mo/Mo are simple percent changes others are at saars | |||||||

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief