Global| Jan 11 2006

Global| Jan 11 2006Mortgage Applications Recovered

by:Tom Moeller

|in:Economy in Brief

Summary

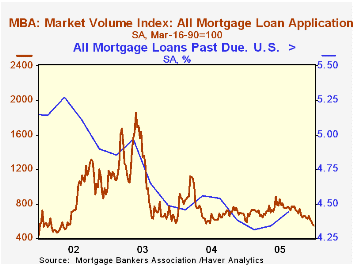

The total number of mortgage applications recovered 9.9% during the opening week of 2006 following four consecutive weeks of decline. The rise, however, was to a level up just 1.0% from the December average. Following four consecutive [...]

The total number of mortgage applications recovered 9.9% during the opening week of 2006 following four consecutive weeks of decline. The rise, however, was to a level up just 1.0% from the December average.

Following four consecutive weeks of decline, purchase applications surged 9.3% w/w to a level 0.4% above the December average.

During the last ten years there has been a 50% correlation between the y/y change in purchase applications and the change in new plus existing single family home sales

Applications to refinance also recovered 9.9%. On top of the prior week's 8.3% gain, refis were 5.8% above December.

The effective interest rate on a conventional 30-year mortgage slipped nine basis points to 6.33%, the fifth consecutive down week, versus an average 6.48% in December. The effective rate on a 15-year mortgage also fell to 5.95%, the first week below 6% since October. The interest rates on 15 and 30 year mortgages are closely correlated (>90%) with the rate on 10 year Treasury securities.

The Mortgage Bankers Association surveys between 20 to 35 of the top lenders in the U.S. housing industry to derive its refinance, purchase and market indexes. The weekly survey accounts for more than 40% of all applications processed each week by mortgage lenders. Visit the Mortgage Bankers Association site here.

| MBA Mortgage Applications (3/16/90=100) | 01/06/06 | 12/30/05 | Y/Y | 2005 | 2004 | 2003 |

|---|---|---|---|---|---|---|

| Total Market Index | 600.1 | 545.9 | 2.1% | 708.6 | 735.1 | 1,067.9 |

| Purchase | 457.4 | 418.3 | 16.4% | 470.9 | 454.5 | 395.1 |

| Refinancing | 1,497.5 | 1,363.2 | -13.0% | 2,092.3 | 2,366.8 | 4,981.8 |

by Carol Stone January 11, 2006

Five moderate-sized European countries reported industrial production today for November. That simple statement is about the only general statement we might make about their reports. It looks that one cannot make a simple, broad generalization about the condition of industry in this region as a whole. It is true that only one country, Sweden, saw production decline. And even though output rose in the other four, the trends are uneven. The biggest gain was in Ireland, a sizable 10.6% in just the one month, following 3.0% in October. This also produced a large 14.7% gain from a year ago. Even so, monthly amounts have swung widely, so we cannot conclude with any confidence that Ireland's industry will maintain a forward path. As seen in the table below, Ireland's production fell almost 9% in September and, for 2004 as a whole, it increased only 0.3%.

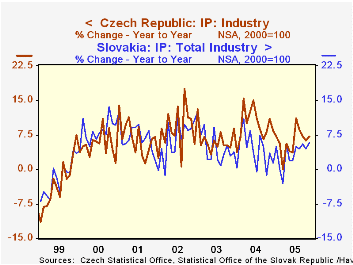

Somewhat more consistent growth is evident in the Czech Republic. While experiencing the occasional monthly decrease, production there has maintained a generally strong uptrend, with a 7.2% increase over the last 12 months. Transportation equipment is one industry that has contributed, although other individual industries have shown zigzag patterns. Neighboring Slovakia also keeping up a firm pace, although not as rapid as the Czechs; Slovakia's year-on-year advance is a nice 5.7%. Chemicals and metals are among sectors that have gained recently, while mining activity and transport equipment have lagged.

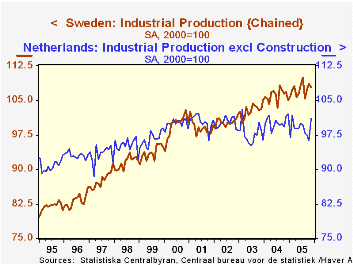

The Netherlands saw a 5.0% surge in November, but that followed declines in the two previous months and the last 12 have managed only a minute 0.1% rise. Dutch production is on the slowest trend overall of these countries. Much of manufacturing has been sluggish, while the utilities sector behaved like industry as a whole, up in November, but after a sizable decline in October.

Finally, Sweden may have lost some output volume in the latest month, but it has otherwise grown modestly in general, averaging 1.7% since 2002. Recently clothing, wood products and machinery have added output, while mining and transport equipment have slowed.

These five countries illustrate that smaller production units may experience more volatility, and that neighboring countries may experience varying patterns of growth and decline despite their proximity. In one sense, this behavior resembles regions of the United States, where the fortunes of one state may be opposite to those of even the locale next door. In these smaller units, there is less diversity, making each location more vulnerable to developments in just a few products or materials. All this said, we'd opine that the growth of industrial production in most of these countries is a sign that industry is resilient and adaptable in the face of moving exchange rates and substantially higher energy costs.

| Industrial Production (% Changes) | Nov 2005 | Oct 2005 | Sept 2005 | Year/- Year | 2004 | 2003 | 2002 |

|---|---|---|---|---|---|---|---|

| Ireland | 10.6 | 3.0 | -8.9 | 14.7 | 0.3 | 4.7 | 7.2 |

| Sweden | -0.6 | 1.0 | 2.0 | 1.0 | 3.1 | 2.5 | 1.2 |

| Netherlands | 5.0 | -1.2 | -0.5 | 0.1 | 2.6 | -2.4 | -0.3 |

| Czech Republic | 3.0 | 0.9 | -2.6 | 7.2 | 9.9 | 6.4 | 8.6 |

| Slovakia | 4.5 | -4.1 | 1.1 | 5.7 | 4.2 | 5.0 | 6.4 |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief