Global| Oct 27 2008

Global| Oct 27 2008Money Supply Growth Stabilizes

Summary

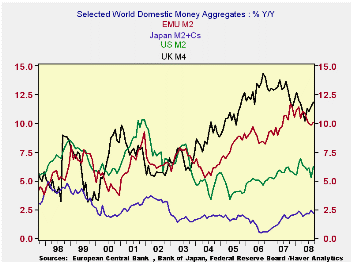

Europes money supply growth and credit growth do not show signs of further slowing in September. Growth is slower that it has been over the past 12months but 3-month growth rates are about the same or a bit higher than 6-month rates [...]

Europe’s money supply growth and credit growth do not show signs of further slowing in September. Growth is slower that it has been over the past 12months but 3-month growth rates are about the same or a bit higher than 6-month rates of growth. In the US and the UK rates of growth in three months have picked up beyond those for their respective 12-month paces. In Japan money growth rates are very low and continue to ease. The grow rates for real money balances actually look a bit stronger all around except in Japan.

As the financial problems have gotten worse one thing we have seen is that money supply numbers have bulged. Money demand has three components: precautionary, speculative and transactions demand. We tend to look at increases in money supply as being for transactions demand but in times such as these the precautionary element could be spiking as investors ditch riskier investments and flock to bank deposits. I would not look at the pick up in money growth or in the growth in real money balances as something that is inflationary for that reason.

| Look at Global and Euro Liquidity Trends | |||||||

|---|---|---|---|---|---|---|---|

| Saar-all | Euro Measures (E13): Money & Credit | G-10 Major Markets: Money | Memo | ||||

| €€-Supply M2 | Credit:Resid | Loans | $US M2 | ££UK M4 | ¥¥Jpn M2+Cds | OIL:WTI | |

| 3-MO | 10.1% | 8.5% | 7.2% | 7.0% | 16.3% | 1.2% | -63.7% |

| 6-MO | 9.2% | 8.1% | 7.0% | 4.0% | 14.3% | 1.8% | -3.5% |

| 12-MO | 10.1% | 10.5% | 8.7% | 6.2% | 11.8% | 2.2% | 30.8% |

| 2Yr | 10.2% | 10.8% | 9.7% | 6.2% | 12.3% | 2.0% | 27.2% |

| 3Yr | 9.6% | 11.2% | 10.2% | 5.7% | 13.0% | 1.5% | 16.4% |

| Real Balances: deflated by Own CPI. Oil deflated by US CPI | |||||||

| 3-MO | 9.2% | 7.5% | 6.3% | 4.3% | 9.7% | 0.0% | -64.6% |

| 6-MO | 6.6% | 5.5% | 4.4% | -1.2% | 7.2% | -0.7% | -8.3% |

| 12-MO | 6.2% | 6.6% | 4.9% | 1.2% | 6.3% | 0.0% | 24.6% |

| 2Yr | 7.1% | 7.7% | 6.6% | 2.3% | 8.6% | 1.0% | 22.4% |

| 3Yr | 6.9% | 8.5% | 7.5% | 2.4% | 9.6% | 0.6% | 12.7% |

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief