Global| Jan 03 2020

Global| Jan 03 2020Money, Credit and GDP vs Geopolitics

Summary

Well, Happy New Year…but realistically it is what it is. Isn't it? The killing of Iranian general Qassem Soleimani, the architect of Iran's military expansion in the Middle East, has created a fire-storm of backlash. But the very [...]

Well, Happy New Year…but realistically it is what it is. Isn't it? The killing of Iranian general Qassem Soleimani, the architect of Iran's military expansion in the Middle East, has created a fire-storm of backlash. But the very description of who this guy is explains why the US (Trump) did what it did. Iran has been ‘getting away' with under the radar (perhaps literally) attacks on ships in the Gulf on Saudi oil facilities on US troops on oil contractors in the region and against the US embassy in Iraq. The knowledge of who was behind this was not matched by clear forensic evidence and so in each case Iran skipped free of blame suffering only raised eyebrows and deepening suspicions. But this now-dead soldier was architect of that that aggression and so now the game has changed, the rules have changed and fractures in all sort of alliances are further pressed to the breaking point or beyond. Most disturbing is the ongoing Democrat-Republican rift and the reaction to this event that is strongly along party lines. When will these two idiotic political parties understand that we are all Americans and being American bonds us together more than being a Democrat or Republican separates us? This lingering impeachment proceeding is a poison to the union.

Well, Happy New Year…but realistically it is what it is. Isn't it? The killing of Iranian general Qassem Soleimani, the architect of Iran's military expansion in the Middle East, has created a fire-storm of backlash. But the very description of who this guy is explains why the US (Trump) did what it did. Iran has been ‘getting away' with under the radar (perhaps literally) attacks on ships in the Gulf on Saudi oil facilities on US troops on oil contractors in the region and against the US embassy in Iraq. The knowledge of who was behind this was not matched by clear forensic evidence and so in each case Iran skipped free of blame suffering only raised eyebrows and deepening suspicions. But this now-dead soldier was architect of that that aggression and so now the game has changed, the rules have changed and fractures in all sort of alliances are further pressed to the breaking point or beyond. Most disturbing is the ongoing Democrat-Republican rift and the reaction to this event that is strongly along party lines. When will these two idiotic political parties understand that we are all Americans and being American bonds us together more than being a Democrat or Republican separates us? This lingering impeachment proceeding is a poison to the union.

This sort of political bifurcation and opposition to everything an administration does is more than just vexing, it is dangerous. And by that I do not play into the hand of those who call Trump dangerous it is the schism itself that is dangerous. It is Democrat's inability to accept Trump as their legitimate President that is causing this division. Get on with it! There is an election in less than one year. We do not have a parliamentary form of government that allows an administration to be toppled over lack of confidence – bit it is pretty clear that even by that standard Trump would not be removed.

So now, apart from the impact on US politics, alliances in the Middle East will be pressured. The Europeans are going to be angry as they – the great architects of appeasement always- have been trying to bring Iran back to a nuclear deal that may have been working (may not have been working). It was a deal cut in concert with them by former US President Obama that allowed ongoing meddling by Iran in the Middle East that is having consequences we can see day by day. The Iranians do not play ‘nice' and we may never know if they were really obeying their side of the nuclear agreement they made.

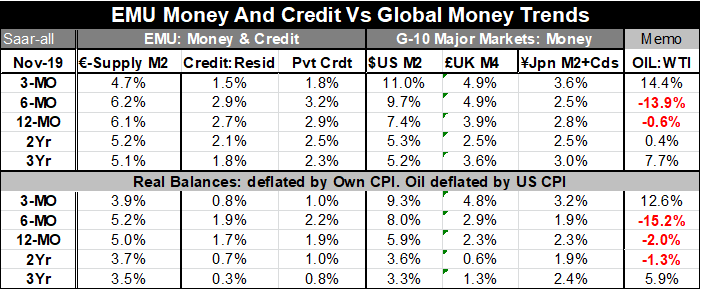

EMU shows some ongoing money and credit growth progress

EMU shows some ongoing money and credit growth progress

But in the wake of the news today bond yields are sharply lower, stock markets are quavering and politicians are lobbying.

Meanwhile… as they used to say in the old TV Westerns…back at the ranch…economic data have shown that money and credit growth globally has been responding to stimulus. Money growth is up in the main monetary center countries of the West and Japan and China has recently unlocked more liquidity in its system.

Real and nominal growth rates of money inside one year also show acceleration. What looks less than successful is the development of credit in EMU. Nominal credit growth has been creeping up but those gains have slowed. Growth rates inside one year have showed slowing in both real and nominal terms.

Meanwhile although many had cut their assessment of recession prospects (oops!) we have a new jolt of uncertainty from this new round of geopolitical confrontation that may or may not represent an escalation. From the stand point of events you can point to it as a watershed; it sure has grabbed headlines. But Iran was already far along the path of attacks on oil infrastructure from ships attacked or outright seized to an attack on Saudi facilities or against US troops and US contractors using their agents and so let's get real-what has really changed? It is that the conflict is now out in the open? But whether you know who killed you or not you are still dead! Right? So I'm not sure that this is as much the ‘escalation' it is being billed as, as it is the event that no longer allows the fact of the conflict and growing risk to be ignored.

The attack on the US diplomatic facility in Baghdad was a huge miscalculation by Iran. Now even the European who have been so good at appeasement over the years have to look the situation in the eye and deal with it for what it really is. The British response is to ask both sides for forbearance (good one!). It's hard to argue with that plea but also hard to see that happening. Iran is angry over sanctions, its economy is depressed. It raised its domestic oil tax because it is so strapped for funds; supporting the terrorist groups in the Middle East is expensive. Iranian citizens do not want to pay higher taxes to support that. Part of the US pressure was to force this compression to happen.

Iran's words assert that it will continue to support its religious groups in the region. But there is nothing religious about the terrorism it finances. To portray this as religious freedom is a hoax, ‘fake facts' of the worst kind. Europeans have been willing to turn a blind eye – to appease Iran's activity -and even to let it develop longer range missiles in return for ‘peace' now. But how is the pretense of peace now worth greater instability later, especially when ‘peace now' is only a cover story for the ongoing unattributable terrorism that Iran has supported and created?

So now we look ahead to 2020 (remember…I pointed out that 20/20 vision is only average vision and is not perfect vision). I warned about how poor our vision has been on average – we now have a much different start to 2020 than what had been expected.

Oil prices are now climbing and this is after the year was introduced as one that would see more modest shale production in the US. But as oil prices rise that prognostication becomes less likely. Will Iran become more aggressive in disrupting shipping in the Gulf? It might. But anything it does to expose its own hand directly also puts it at greater risk. And its economy is already held together by fragile forces. Iran has had to use force against its people to stop their anti-tax rioting. So who is more at risk in Iran is it the hardliners or the reformists? It is still hard to tell.

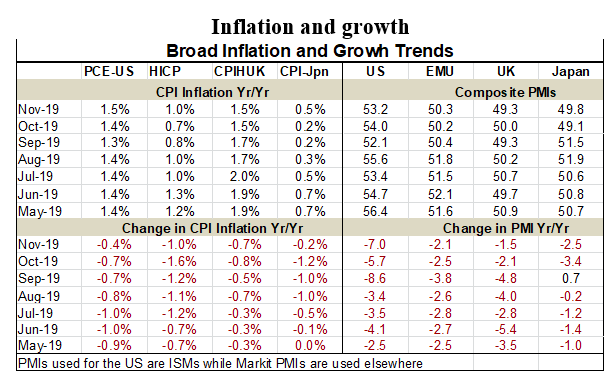

However, global economic data show ongoing erosion of the composite PMIs and especially manufacturing PMIs. While there has been some attempt to portray this as coming stability all we can really say is that some PMIs are off their lows but there is still erosion in train. The US manufacturing ISM today fell significantly month-to-month and at a level of 47.2 it is near the 46.5 average value that the manufacturing ISM has had at the start of all recessions since 1980. (on a longer profile comparison with past recession starts we are already below the average ‘trigger value on the MFG ISM ).So we are three days into the New Year already the best laid plans have gone awry. Optimists may hold that things will get better and this will be dealt with. Even Iran is saying it does not want war but it also said it would not shy away from conflict (something that we already knew). But conflict is much easier to engage in if you are the one inflicting damage on someone else without reprisal...the way it was before yesterday. I argue that Iran's world has changed a lot more than our world.

Obviously re-handicapping 2020 cannot be done on the breadth of a dime. But the outlook and back ground for 2020 seems to have change markedly compared to what had earlier been assumed. And there are many other hot spots that have yet to ‘report in' for 2020…North Korea being one of them. And it looks like Trump's good friend Kim Jong-un is going to go back to being rocket man, whatever that will entail or imply for US action and for regional security.

If uncertainty was the a major factor behind why the economy and investment were so weak last year, will someone tell me what has happened now to make global certainty less of an issue in 2020? I think we all know the answer to that one. So I would be surprised if the bond rally were a one day affair. Although in these circumstances oil prices are likely to remain ‘elevated' and that just might underpin a bit more inflation than we have seen recently. So we should be on a new global monetary policy watch – this time NOT for deeper negative rates.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief