Global| Nov 28 2017

Global| Nov 28 2017Money and Credit Trends Finally Begin to Shift; Is It a Shift for the Better?

Summary

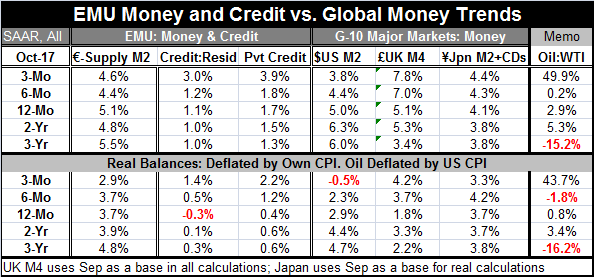

The EMU shows some acceleration in credit over the last three months. Private credit shows regular if slow step-ups in credit growth rates. Money supply, however, has slowed slightly compared to its 12-month pace. The real balance [...]

The EMU shows some acceleration in credit over the last three months. Private credit shows regular if slow step-ups in credit growth rates. Money supply, however, has slowed slightly compared to its 12-month pace. The real balance growth rate for money supply has slipped. However, private credit in inflation-adjusted terms continues to show a step-up in its growth.

The EMU shows some acceleration in credit over the last three months. Private credit shows regular if slow step-ups in credit growth rates. Money supply, however, has slowed slightly compared to its 12-month pace. The real balance growth rate for money supply has slipped. However, private credit in inflation-adjusted terms continues to show a step-up in its growth.

U.S. money supply shows a moderate but clear deceleration in progress. The U.K. and Japan show increases in the nominal money supply growth rate. Japan's pace is up slightly while in the U.K. the pace of money growth has stepped up significantly and it's excessive. And the Bank of England has begun to hike rates in the U.K. The growth of real money balances in the U.S. has actually turned negative over three months compared to a 2.9% pace over 12 months. In the U.K., the growth rate for real balances is double over three months compared to 12 months and about one percentage point stronger over three months than over two years. At 4.2%, the real U.K. three-month money growth rate is also excessive. In Japan, real balance growth has slipped slightly over three months.

The far right hand column shows the path of oil prices (West Texas Intermediate).

In assessing these trends, the upturn in credit in the EMU is encouraging, while the slowing in money growth is still modest.

In the U.S., the slowing in money growth and the drop in the three-month real balance growth rate is an eye-opener. At the same time, the U.S. yield curve has continued to flatten out and inflation remains under the Fed's target, as it has since the target was adopted in early-2012. In the University of Michigan survey, inflation expectations continue to be modest with median inflation in that survey at an all-time low. While U.S. growth is looking better and has picked up, in some respects growth still has challenges and has been stimulated artificially by hurricane damage induced spending on vehicles and on other replacements and repairs.

In the U.K., money supply growth is rising along with inflation. But in the U.K., wages are lagging behind prices. It does not appear to be engaged in a price-wage spiral. A weak pound sterling in reaction to previous BOE easing is partly responsible for the excesses we see in the U.K. But the U.K. is also seeing weakness in the form of weak building activity in London and a slowing nationwide service sector. There is a blow coming to the U.K. as a result of the Brexit process. EU institutions that had been located in the U.K. plus some banking activity will be moved outside of the U.K. borders causing a loss of incomes and of relatively high-paying jobs on a permanent basis. These realities leave the BOE with some tough choices. Some think inflation needs to be addressed now - and the BOE has begun to hike rates already. But adding a depressing monetary wave of restriction to an economy already facing persistent headwinds that will have lasting consequences puts the BOE in a tight spot.

In Japan, because inflation is so low and has been so low for so long, the stirring of nominal money growth is encouraging. But the fact of slightly weaker growth in real balances over three months suggests that the tick-up in nominal growth is not yet real good news. The slowing in Japan's real balances will require some monitoring.

There are finally some shifts in money and credit growth and more broadly in financial conditions as well as growth globally. But it is still a world of different strokes for different folks. As an over view, Japan seems to have the least in flux. The U.K. is in the most difficult policy box with the crush of Brexit in train even as inflation and money growth are both rising. In the U.S., despite some upbeat consumer surveys and growth news, inflation is undershooting and the bond market is offering a more questionable view of the future. The news in the EMU is perhaps the best of all. The pick-up in private credit growth is truly goods news, and while the tail-off in the growth rate of real balances is only a modest slippage, it is still something to monitor.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief