Global| Mar 28 2013

Global| Mar 28 2013Money and Credit Trends Disappoint

Summary

Money and credit growth in the European Monetary Union continue to be disappointing. Money supply growth over 12 months is at a 4.3% annual rate while over three months it has slipped to a 3.5% annual rate. On unchanged velocity it is [...]

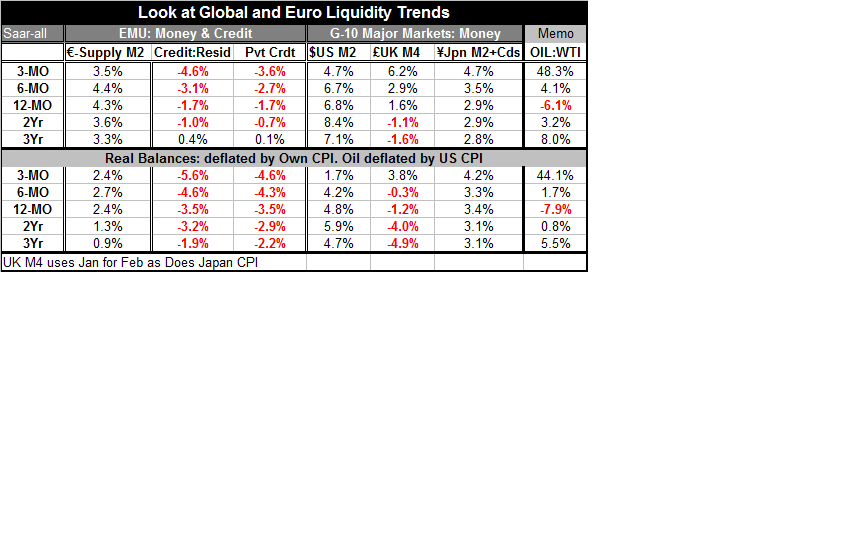

Money and credit growth in the European Monetary Union continue to be disappointing. Money supply growth over 12 months is at a 4.3% annual rate while over three months it has slipped to a 3.5% annual rate. On unchanged velocity it is unable to support 2% growth with 2% inflation. Over the last 12 months credit to residents has fallen by 1.7% over three months it's falling at a 4.6% annual rate. Expressed in inflation-adjusted terms the growth of the real money stock in EMU is more stable at a 2.4% annual rate over 12 months and at a 2.4% annual rate over three months. However, in real terms the extension of credit continues to contract and continues to contract and a quickening pace.

Money and credit growth in the European Monetary Union continue to be disappointing. Money supply growth over 12 months is at a 4.3% annual rate while over three months it has slipped to a 3.5% annual rate. On unchanged velocity it is unable to support 2% growth with 2% inflation. Over the last 12 months credit to residents has fallen by 1.7% over three months it's falling at a 4.6% annual rate. Expressed in inflation-adjusted terms the growth of the real money stock in EMU is more stable at a 2.4% annual rate over 12 months and at a 2.4% annual rate over three months. However, in real terms the extension of credit continues to contract and continues to contract and a quickening pace.

Global trends in money growth are mixed. In the US, M2 growth, which has been weaker the past year than it was over the past two years, has continued to decelerate: it's twelve-month growth rate of 6.8% is above its three-month growth rate which is running at a 4.7% annualized pace.

The UK has had a turnaround. UK money growth had been declining. But in the middle of 2012 its negative growth rates began to diminish. Currently its twelve-month annual growth rate is a +1.6% while its three-month growth rate is a positive 6.2%. UK has exhibited clearly the most volatile money growth since the financial crisis began. Its current acceleration in sterling M4 balances represents another abrupt move in the growth rate of money supply.

It's probably too soon to say that the new Bank of Japan policies are taking hold. However, Japan's money supply, M2 plus CDs, has stepped up its growth rate. Over the last year, as well as in the last two and three years, money growth has hovered a tick below 3% in Japan. However, over six months the growth rate in Japan has gone up to 3.5% and over three months the growth rate has stepped up to a 4.7% annual rate.

While the Eurozone may have succeeded in stabilizing the growth rate in real money balances, nominal money supply remains in a decelerating mode. More to the point, money and credit growth rates are diverging and have been diverging since the third quarter of last year. The money-credit creation process in Europe appears to have been divorced-irreconcilable differences! While money supply has been able to be placed on an upward trend the growth rate for credit has not.

While the European central bank is widely lauded (in some circles...) for its LTRO program, that program which helps to funnel money to banks and which helps banks to support the local government securities markets does not encourage banks to support the extension of credit to their local private markets. Duh!?

The emphasis has been on keeping the government sectors afloat and there has been a neglect of the private sector. In some sense this is understandable because if 'the ship' is sinking you look to plug the hole. But these ships have been sinking for some time and the captain of the ship also needs to pay attention to the direction in the course. As with the ship it's true that, if it sinks, the course and speed don't matter much. But in this case it's the course in the speed of the private sector that matters and if the private sector could be stabilized or better yet stimulated (!), that alone would help to plug the government's fiscal hole. Neglect of the private sector is making things worse. Meanwhile, the central bank thinks that it has stabilized the situation and eliminated corrosive speculation by stabilizing the government sector! In fact, it is helping to sink the real ship.

At what point in this recovery process will the political and economic leaders of the European Union decide that it's time to put the bunker mentality of crisis-fighting behind them and to focus on letting markets do their job? Right now policy in the United States as well as in Europe - and increasingly in Japan - leans heavily on the side of making the invisible hand as invisible as possible to the point of extinction. The tremendous rounds of quantitative easing in the United States and in the UK have all but obliterated the markets' ability to create reasonable expectations about the future and, because of their tampering with market prices and yields, market signals can no longer serve central banks as indications of what longer-term interest rate expectations or inflation expectations really are.

We have come to live in a world where fiscal policy has been so overused that using it further becomes dangerous, as with an overdose of any drug. Still some argue that the dose is not yet large enough! We now live in a world where monetary policy is believed to be the solution to all problems: perhaps we will use it to cure cancer and put a man on Mars.

In doing this, we have come to completely neglect the private sector as an engine of growth while policymakers have come to view it as a deepening well of tax revenues to solve their budget deficit problems. From getting the rich to pay their 'fair share' in the US, to President Hollande's attempt to stick a 75% tax on the super-rich in France, to say nothing of hikes in VATs across Europe, the private sector has become a stooge for revenue 'creation' (better-still: 'invention'). In this world no one seems to conceive of the potential for this well to run dry. The private sector is treated as though it lives in a world of its own. In this world it is unaffected by the fiscal shenanigans going on around it, while at the same time we are led to believe that the 'monetary' 'stimulus' that continues to show signs of being impotent eventually will work... through that same private sector Can you say 'selective perception? God help us, we know not what we do.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief