Global| Feb 23 2005

Global| Feb 23 2005Mixed Trends in Japanese Sectoral Activity

Summary

Has Japan fallen into yet another recession? Last week's GDP report, with a third consecutive decline in Q4, was read by some analysts as indicating just such a renewed slump. Wednesday in Tokyo, the Ministry of Economy, Trade and [...]

Has Japan fallen into yet another recession? Last week's GDP report, with a third consecutive decline in Q4, was read by some analysts as indicating just such a renewed slump. Wednesday in Tokyo, the Ministry of Economy, Trade and Industry (METI) published industry activity data for December that might be seen casting a somewhat brighter light on the Japanese economy.

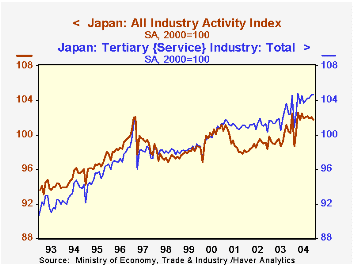

The All-Industry Activity Index (2000=100) fell 0.3% in December after a 0.2% rise in November. The graph shows that it was strong but erratic in the spring and has softened in the last several months, basically stagnating over the second half of the year.

Among its components, construction activity has been in a long downtrend since the outset of its index in 1993 and it remains on that path. The most favorable observation on this series is that the 3.8% year-on-year decline in December is the smallest since July 2003.

The industrial production index, reported about a week ago, fell 0.8% in December, but that followed a 1.7% jump in November, tracing an erratic month-to-month pattern. The trend, indicated by the December-to-December growth, saw a 1.8% advance, which is slower than the gains for 2003 and 2004 overall.

Tertiary activity, that is, services, was flat in December, but it too had risen in November, and in December was 2.2% ahead of a year earlier. In contrast to other sectors, services seem to be picking up somewhat. This tendency varied widely among service sectors, however, as wholesale and retail trade held some gains, while restaurants and accommodations stumbled. Information services sagged markedly early in 2004, but firmed noticeably late in the year.

Thus, it's difficult to put a single characterization on the Japanese economy at this time. "Fragile" might fit, with an easy potential to weaken. But service industries, as in other nations' economies, may be providing some stability, helping to diminish cyclical tendencies.

| Dec 2004 | Nov 2004 | Q4/Q3 | Dec 04/ Dec 03 | 2004 | 2003 | 2002 | |

|---|---|---|---|---|---|---|---|

| All- Industry Activity | -0.3 | +0.2 | -0.1 | +1.7 | +2.3 | +0.9 | -0.4 |

| Construction | -1.6 | -1.0 | -0.9 | -3.8 | -5.7 | -5.3 | -4.3 |

| Industrial Production | -0.8 | +1.7 | -0.7 | +1.8 | +5.6 | +3.2 | -1.2 |

| Tertiary Activity | 0 | +0.4 | +0.5 | +2.2 | +2.1 | +0.8 | 0 |

| Memo: GDP | -- | -- | -0.1 | +0.6 (Q4/Q4) | +2.6 | +1.4 | -0.3 |

Carol Stone, CBE

AuthorMore in Author Profile »Carol Stone, CBE came to Haver Analytics in 2003 following more than 35 years as a financial market economist at major Wall Street financial institutions, most especially Merrill Lynch and Nomura Securities. She had broad experience in analysis and forecasting of flow-of-funds accounts, the federal budget and Federal Reserve operations. At Nomura Securities, among other duties, she developed various indicator forecasting tools and edited a daily global publication produced in London and New York for readers in Tokyo. At Haver Analytics, Carol was a member of the Research Department, aiding database managers with research and documentation efforts, as well as posting commentary on select economic reports. In addition, she conducted Ways-of-the-World, a blog on economic issues for an Episcopal-Church-affiliated website, The Geranium Farm. During her career, Carol served as an officer of the Money Marketeers and the Downtown Economists Club. She had a PhD from NYU's Stern School of Business. She lived in Brooklyn, New York, and had a weekend home on Long Island.

More Economy in Brief