Global| Sep 12 2016

Global| Sep 12 2016Mixed Signals from Japan's Corporate Sector

Summary

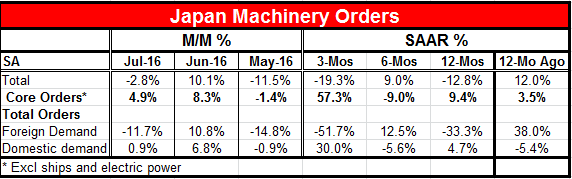

Foreign Demand Sinks as Domestic Demand Revives But Core Orders Stage Turnaround Nailing down Japan's economic trends can be harder than nailing Jell-O to the wall. Japan's orders report has enough convoluted trends to keep us [...]

Foreign Demand Sinks as Domestic Demand Revives

But Core Orders Stage Turnaround

Nailing down Japan's economic trends can be harder than nailing Jell-O to the wall. Japan's orders report has enough convoluted trends to keep us confused for at least for another month. Core orders are supposed to be the more reliable series but it is very volatile even as this month does put strong back to back gains in place. These gains look out of place given the other Japanese data we have seen including for industrial output and the PMI reports. The overall orders data that include "lumpy" projects are weaker on-trend than the "core-orders" as well as being weaker over the near-term with foreign demand weakness dominating what domestic strength there is.

Nailing down Japan's economic trends can be harder than nailing Jell-O to the wall. Japan's orders report has enough convoluted trends to keep us confused for at least for another month. Core orders are supposed to be the more reliable series but it is very volatile even as this month does put strong back to back gains in place. These gains look out of place given the other Japanese data we have seen including for industrial output and the PMI reports. The overall orders data that include "lumpy" projects are weaker on-trend than the "core-orders" as well as being weaker over the near-term with foreign demand weakness dominating what domestic strength there is.

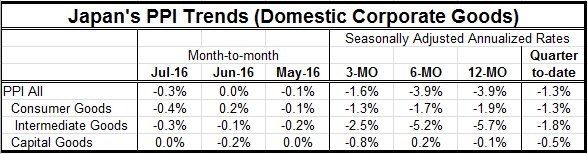

Corporate Goods Price Trends in Japan Undermine Outlook

On the price front, the corporate goods price index shows declines in prices in July with prices falling in all sectors except capital goods. Over three months, however, prices are falling in all PPI categories. In the chart we can see that corporate goods prices often move ahead of consumer prices and they are more volatile as well (note the TWO-SCALE chart).

On the price front, the corporate goods price index shows declines in prices in July with prices falling in all sectors except capital goods. Over three months, however, prices are falling in all PPI categories. In the chart we can see that corporate goods prices often move ahead of consumer prices and they are more volatile as well (note the TWO-SCALE chart).

On trend, while Japan's prices are still falling- which is not really a good sign for domestic activity- price declines generally are not accelerating. That is some source of relief. But overall prices are falling on all horizons from 12-Mo to 6-Mo to 3-Mo and in just about all categories as well on those same horizons. The annualized pace of decline is not getting worse...except oddly for capital goods. Of course, capital goods would be the sector most removed from temporary or cyclical oil and other commodity price weakness. So a stepped up pace of price weakness there is really not a good sign at all for economic activity. And that takes us back to the weakness we see on the machinery orders report.

Therefore, it is not possible to give Japan's economy a positive bill of health in July on these data and trends. The economy appears to be still-struggling. The new global markets weakness on the heels of the view that the Fed is getting ready to hike rates again is another adverse development for Japan to have to overcome.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.

More Economy in Brief