Global| Jan 29 2014

Global| Jan 29 2014Mixed Patterns for Money Growth

Summary

Money growth rates around the world have become somewhat mixed. Year-over-year growth rates in the United States and the European Monetary Union have slowed slightly while growth rates in the UK and Japan have been accelerating. The [...]

Money growth rates around the world have become somewhat mixed. Year-over-year growth rates in the United States and the European Monetary Union have slowed slightly while growth rates in the UK and Japan have been accelerating. The US still has the strongest growth rate of this group.

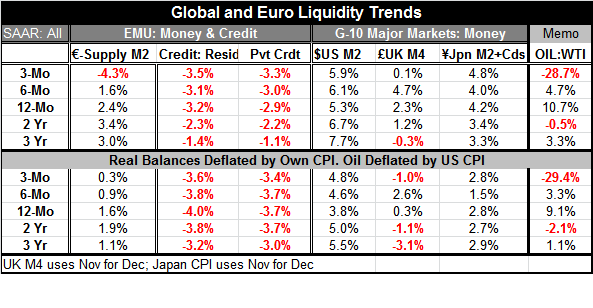

Over shorter horizons developments in the European Monetary Union's money supply show a sharp reduction, especially over the most recent three months. Money supply in the EMU that had grown at a 2.4% annual rate over 12 months and slipped to 1.6% over six months is now declining at a 4.3% annual rate over three months. This is not a welcome development. Meanwhile, credit to residents continues to contract. The pace of contraction has stepped up only slightly, falling at a 3.5% annual rate over three months compared to 3.2% over 12 months. Similarly, private credit is down 2.9% over 12 months and is down at a 3.3% annual rate over three months.

For the US, the growth of the money aggregate M2 has been fairly stable. Its 5.3% twelve-month growth rate picked up to 6.1% over six months and is back down to 5.9% over three months. These growth rates are below the 6.7% pace and 7.7% pace over two years and three years, respectively. In the UK twelve-month money growth was 2.3%. That accelerated to 4.7% over six months, but, over three months, is only 0.1%. However, since we simply plugged in the November money number as a surrogate for the missing December figure, it is likely that UK money growth is doing better than this when the December figures are in. For Japan, money growth is 4.2% over 12 months and that is better than it had been in the previous 2-3 years over six months it slipped slightly at 4%, but over three months it is up to a 4.8% annual rate. While this is modest progress in money growth, it appears that Abe-nomics is moving things in the right direction as far as money growth is concerned.

If we look at real balances or inflation-adjusted figures for money and credit we find that in the case of the monetary union real balance growth has decelerated but is still showing positive growth. M2 money supply for the monetary union is up by 1.6% over 12 months; it is up at a 0.9% annual rate over six months and edging up ever so slightly by 0.3% at an annual rate over three months. That does not look like figures from a union with improving growth. Credit to residents is still contracting when inflation-adjusted; the pace is slightly reduced in real terms. For example, there is a 4% contraction over 12 months, and a 3.6% rate of contraction over three months. Similarly private credit is down 3.7% over 12 months but is down only at a 3.4% annual rate over three months. The real numbers are better than their nominal counterparts, but the trends for money and credit are still not very encouraging in the monetary union.

Real balances for the US show some acceleration in growth. The recent growth rates are still lower than growth rates over 2-3 years, but the three-month growth rate of 4.8% is higher than the 12-month rise of 3.8%.

For the UK, there are positive growth rates over three months and 12 months, setting them apart from the previous two and three years. However, the three-month growth rate which again uses a November surrogate figure for December shows a 1% drop at an annual rate. It is likely again that the real number for December will produce better growth in real balances for the UK.

For Japan, real balance growth is steady. The two to three-year growth rate for real balances is in the 2.8% range and real balances have grown by 2.8% over the last year, and they are growing at 2.8% of the most recent three months. So for Japan, we would call real balance growth steady. In this sense, we do not see much influence from Abe-nomics on real balances.

EMU Money and Credit Growth

The chart above shows growth rates of money and credit to the private sector in the European Monetary Union. We can see that money growth has been turning lower now for a number of months. After a period of divergence with credit growth, both money and credit growth are slowing although credit growth while slowing is actually contracting. Credit growth began this process of slowing and contracting long before money growth turned around. While there is some optimism about Europe growing better, it is true that recent economic statistics on Europe have been uneven with Germany continuing to post some pretty strong numbers, having the largest current account surplus in the world, but not showing much revival in its consumer sector to help growth in other EMU members. In the union, but outside of Germany, conditions continue to be somewhat uneven although optimism on European recovery is still intact.

Developing Economies and Markets

It is unclear where we should lay the blame for the current problems we have seen in developing economies. While some of these have cropped up together, I can see, for example, that the problems in Argentina and Turkey are responsible for the market conditions that we have seen in those countries. Some want to link these back to the US policy of starting to taper away from its quantitative easing program. But the US has decided to step away from this program at least in part because officials do not see it is that effective anymore.

Whenever there are several countries experiencing problems at the same time, it is common to have people talk about contagion. But with problems in countries from South America, to Asia, to the tip of Africa, to the bridge between the Middle East and Asia, it is hard to find the right common denominator. Nor can we look at these countries and say that their common problem is in the currency market because when developing economies have problems their currency is the first thing that takes a hit. It is just how things work.

What I regard is particularly odd is to name names, Brazil, for example, that complained that they were hurt when the United States launched its program of QE and more recently Brazil is claiming it is hurt as the US is launching its program to taper QE. Some of these complaints simply are self-serving. For those who want to blame tapering for weaker demand conditions in a feedback loop to developing economies, we have to remember than in real time the US economy has actually posted stronger growth in the second half of the year since it has announced that the tapering program would be put in place. One can certainly argue that it is expectations at work, but that seems a strange argument given in reality growth has been stronger and the program that is being cut is being cut because it is thought to be ineffective.

But looking to the period ahead, there are some real challenges. The Federal Reserve is going to be tapering away from quantitative easing. Even if US growth picks up, the cession of this program is likely to lead to higher interest rates and that will impact developing economies. Nor is it certain that the growth pick up at the end of the year will be sustained since much of it has come from inventory building. While there is optimism that the EMU has turned the corner and is improving, it is unclear how fast growth will be or how widespread improvement will be in the monetary union. China already has seen handwriting on the wall and has shifted from its export-led growth plan to one that emphasizes the development of domestic demand. Other developing economies probably need to do the same thing.

It is important for the countries of the world to stand on their own two feet. It is important that developing economies do not depend too much on the kindness of strangers or the demand growth in developed economies. The developed economies are trying to mend themselves after the financial crisis and the realization that they piled on too much debt. This has implications for global growth. There is no point complaining about it. The point is to realign growth to account for it. This may be part of the growing pains that were seeing in some of the developing economies. However, it strikes me that it is too soon for these fallout affects to have hit. Only China is making major changes in its economy's structure to try to reorient sources of growth. What this means is that China will cease to be a bellwether for global growth since China is shifting gears to depend more on itself.

The broad global money supply numbers from the various money center economies suggest that there is still plenty of liquidity in the world economy. Nominal and real balances are still largely growing with the exception of the European Monetary Union. Interest rates are still low. The dollar area is still seeing more rapid money supply growth than in the other countries in the table. We do not think liquidity is the problem. But we do think that countries need to pay attention to what is driving their growth and to make sure that they are prepared for years ahead with plans to become more self-reliant.

Robert Brusca

AuthorMore in Author Profile »Robert A. Brusca is Chief Economist of Fact and Opinion Economics, a consulting firm he founded in Manhattan. He has been an economist on Wall Street for over 25 years. He has visited central banking and large institutional clients in over 30 countries in his career as an economist. Mr. Brusca was a Divisional Research Chief at the Federal Reserve Bank of NY (Chief of the International Financial markets Division), a Fed Watcher at Irving Trust and Chief Economist at Nikko Securities International. He is widely quoted and appears in various media. Mr. Brusca holds an MA and Ph.D. in economics from Michigan State University and a BA in Economics from the University of Michigan. His research pursues his strong interests in non aligned policy economics as well as international economics. FAO Economics’ research targets investors to assist them in making better investment decisions in stocks, bonds and in a variety of international assets. The company does not manage money and has no conflicts in giving economic advice.