Global| Feb 13 2009

Global| Feb 13 2009Michigan Consumer Sentiment Sinksto Its Lowest Since 1980

by:Tom Moeller

|in:Economy in Brief

Summary

The University of Michigan reported that its mid-February reading of consumer sentiment fell sharply. The 8.2% month-to-month decline to a level of 56.2 nearly reversed all of the gains of the prior two months and returned the index [...]

The University of Michigan reported that its mid-February

reading of consumer sentiment fell sharply. The 8.2% month-to-month

decline to a level of 56.2 nearly reversed all of the gains of the

prior two months and returned the index to its lowest level since 1980.

The latest figure was down 21% from last February and the reading fell

short of Consensus expectations for an unchanged level of 61.0.

The University of Michigan reported that its mid-February

reading of consumer sentiment fell sharply. The 8.2% month-to-month

decline to a level of 56.2 nearly reversed all of the gains of the

prior two months and returned the index to its lowest level since 1980.

The latest figure was down 21% from last February and the reading fell

short of Consensus expectations for an unchanged level of 61.0.

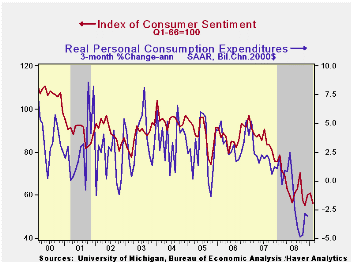

During the last ten years there has been a 62% correlation between the level of sentiment and the three-month change in real personal consumption expenditures.

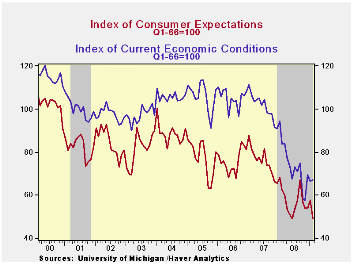

The expectations component of consumer sentiment led the decline in the overall February index. The 15.1% month-to-month drop reversed all of the increases during the prior several months and the series landed at its lowest level since 1980.

Expectations for business conditions during the next

year plunged 42.6% m/m to a new low for the series which dates back to

1947.  Expectations for conditions during the next five years

also fell. The expected change in personal finances also fell back to

the lowest level since last June with a sharp 9.6% decline.

Expectations for conditions during the next five years

also fell. The expected change in personal finances also fell back to

the lowest level since last June with a sharp 9.6% decline.

The current economic conditions index ticked up 0.9% after the sharp 4.3% January decline. Buying conditions for large household goods were viewed as having improved very slightly but the index remained down 17.1% from a year earlier. The view of current personal finances also added very slightly to the large January gain but the index remained down by roughly one-quarter from last February.

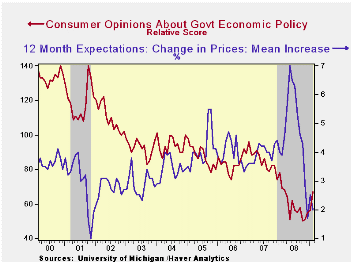

The opinion of government policy, which apparently influences economic expectations, improved to the highest level since last April . Ten percent of respondents thought that a good job was being done by government while a reduced forty-three percent thought that a poor job was being done.

Inflation expectations for the the next year fell back to

2.0%. It was as high as 7.0% in May. The range of expectations is from

slight price deflation to a 5.0% increase in prices, though that latter

figure is half the year-ago expectation. The expected inflation rate

during the next five years also fell to 3.0%.

Inflation expectations for the the next year fell back to

2.0%. It was as high as 7.0% in May. The range of expectations is from

slight price deflation to a 5.0% increase in prices, though that latter

figure is half the year-ago expectation. The expected inflation rate

during the next five years also fell to 3.0%.

The University of Michigan survey is not seasonally adjusted.The reading is based on telephone interviews with about 500 households at month-end; the mid-month results are based on about 300 interviews. The summary indexes are in Haver's USECON database with details in the proprietary UMSCA database.

Stabilizing the Housing Market: Next Steps is the recent speech by Federal Reserve Board Governor Elizabeth A. Duke and it can be found here.

Making Sense of the Subprime Crisis from the Federal Reserve Bank of Boston is available here.

| University of Michigan | Mid-February | January | December | February y/y | 2008 | 2007 | 2006 |

|---|---|---|---|---|---|---|---|

| Consumer Sentiment | 56.2 | 61.2 | 60.1 | -20.6% | 63.8 | 85.6 | 87.3 |

| Current Conditions | 67.1 | 66.5 | 69.5 | -19.9 | 73.7 | 101.2 | 105.1 |

| Expectations | 49.1 | 57.8 | 54.0 | -21.3 | 57.3 | 75.6 | 75.9 |

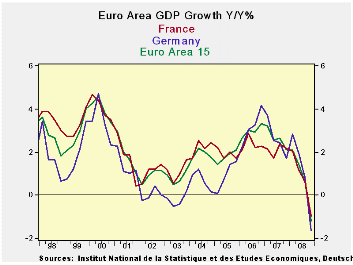

GDP In EMU Falls Hard In 2008-Q4

by Robert Brusca February 13, 2009

GDP is declining in the e-Zone at a very rapid rate. The

fourth quarter GDP declines in the zone have been larger than had been

expected. Declines in Europe are now generally worse than the declines

in the US. Germany has just adopted a second stimulus package worth 50

billion euros over two years to buffer its sagging economy. Budgets in

EMU are beginning to strain or to shatter the EMU guidelines know as

the Maastricht Criteria. Italy and France have been warned by the

Chairman of e-Zone finance ministers, George Junker, about

protectionist policies. "The European Commission needs to examine very

intensively the details of the Italian and French stimulus programs,"

Juncker was quoted as saying in a pre-release of an interview with a

German newspaper. These are the sorts of things that happen in

recession. Survival is the first order of business and sometimes the

rules get trampled or slightly skirted along the road to survival.

As the G-7 finance ministers meet in Italy there is concern

about protectionism. The US too has been warned by Japan. The Japanese

are worried about the ‘buy American’ provisions in the US stimulus

package. No one wants a trade war. But everyone seems to being skating

close to the edge.

Economies are weak and the manufacturing and export-based

economies have been hit the hardest. Note that among this growth of

counties the US Q4 result is second best; Germany and Italy have been

hit hardest. . The US, of course, has a large service sector and it is

a net importing nation. The short fall in US demand has activated one

of the automatic stabilizers in GDP, imports. Imports are weakened so

US GDP has been buffered in its decline, since imports subtract from

GDP growth. Weaker imports mean stronger GDP. But that has transmitted

more weakness overseas to the countries that export to the US. Still

the domestic weakness in the US is severe and it is so severe that

Japan’s Toyota is planning layoffs in its US operations.

This decline in GDP puts everyone on notice for how bad things

are. GDP is one measure all can see and relate to, at least to some

extent. In the US, the labor market has been hit harder than in Europe

with the its broader social safety net and business practices that are

different and a little less quick on the lay-off trigger. There is

concern about how bad the second round effects will be in the US with

such severe labor market displacement. Mitigating that is the task of

the stimulus package. So far US GDP has not been hammered to the extent

expected. But if the US has a more severe second round you can expect

that it will get Europe’s attention too.

| E-Zone and main G-10 country GDP Results | |||||||

|---|---|---|---|---|---|---|---|

| Quarter over quarter-Saar | Year/Year | ||||||

| GDP | Q4-08 | Q3-08 | Q2-08 | Q4-08 | Q3-08 | Q2-08 | Q1-08 |

| EMU-15 | -6.1% | -0.7% | -0.7% | -1.2% | 0.6% | 1.4% | 2.1% |

| France | -4.6% | 0.4% | -1.2% | -1.0% | 0.6% | 1.2% | 2.1% |

| Germany | -8.2% | -2.1% | -2.0% | -1.7% | 0.8% | 2.0% | 2.8% |

| Italy | -7.1% | -2.2% | -2.5% | -2.6% | -1.1% | -0.4% | 0.3% |

| The Netherlands | -3.4% | -1.2% | -0.3% | -0.7% | 1.7% | 3.3% | 4.0% |

| UK | -5.9% | -2.5% | 0.0% | -1.8% | 0.3% | 1.7% | 2.6% |

| US | -3.8% | -0.5% | 2.8% | -0.2% | 0.7% | 2.1% | 2.5% |

Tom Moeller

AuthorMore in Author Profile »Prior to joining Haver Analytics in 2000, Mr. Moeller worked as the Economist at Chancellor Capital Management from 1985 to 1999. There, he developed comprehensive economic forecasts and interpreted economic data for equity and fixed income portfolio managers. Also at Chancellor, Mr. Moeller worked as an equity analyst and was responsible for researching and rating companies in the economically sensitive automobile and housing industries for investment in Chancellor’s equity portfolio. Prior to joining Chancellor, Mr. Moeller was an Economist at Citibank from 1979 to 1984. He also analyzed pricing behavior in the metals industry for the Council on Wage and Price Stability in Washington, D.C. In 1999, Mr. Moeller received the award for most accurate forecast from the Forecasters' Club of New York. From 1990 to 1992 he was President of the New York Association for Business Economists. Mr. Moeller earned an M.B.A. in Finance from Fordham University, where he graduated in 1987. He holds a Bachelor of Arts in Economics from George Washington University.

More Economy in Brief